Despite Soaring Oil Prices Exxon Mobil Continues to Underperform

Oil prices have soared 60% over the past year, helping drive strong total returns between 20% and 40% for most integrated oil giants such as Royal Dutch Shell (RDS.B), British Petroleum (BP), and Chevron (CVX).

However, a notable exception has been Exxon Mobil (XOM), whose stock has returned just 5% during this period, significantly underperforming its major peers and the market as a whole.

Let’s take a look at why the market is so displeased with Exxon right now, and whether or not dividend investors have cause to be concerned.

Wall Street Isn’t Thrilled With Exxon’s Long-Term Growth Plan

After its first quarter earnings report, Wall Street punished Exxon’s share price when new CEO Darren Woods unveiled the company’s ambitious long-term strategy.

Investors had been hoping for a major buyback announcement, now that oil prices are soaring once more and Exxon’s free cash flow is booming. This is mostly the route other major oil companies have taken, because they remain very tight with their capital spending plans (memories of the oil crash continue to linger).

Instead, Mr. Woods announced that Exxon was embarking on a seven-year major growth program that would see it massively increase its capital spending (capex). In other words, Exxon would be sacrificing short-term growth in free cash flow for what’s expected to be much greater cash flow in 2025.

Here's what the company plans to spend on growth:

2016: $19 billion in capex

2017: $23 billion

2018: $24 billion

2019: $28 billion

2020 to 2025: average of $30 billion per year

As you can see, Exxon plans to increase its spending by almost 60% over oil crash levels (2016). Management believes that this will result in substantial production growth, including increasing its daily oil production from 4 million barrels per day (bpd) to 5 million (a 25% increase).

Overall, by 2025 Exxon thinks its $202 billion in spending between 2018 and 2025 will result in:

Increased production by 25% from 4 million bpd oil equivalent to 5 million bpd

Increase chemical production by 30%

Achieve 20%, 20%, and 15% return on invested capital on production, refining, and chemical operations, respectively

Double earnings from refining and chemical

Triple earnings from oil & gas production

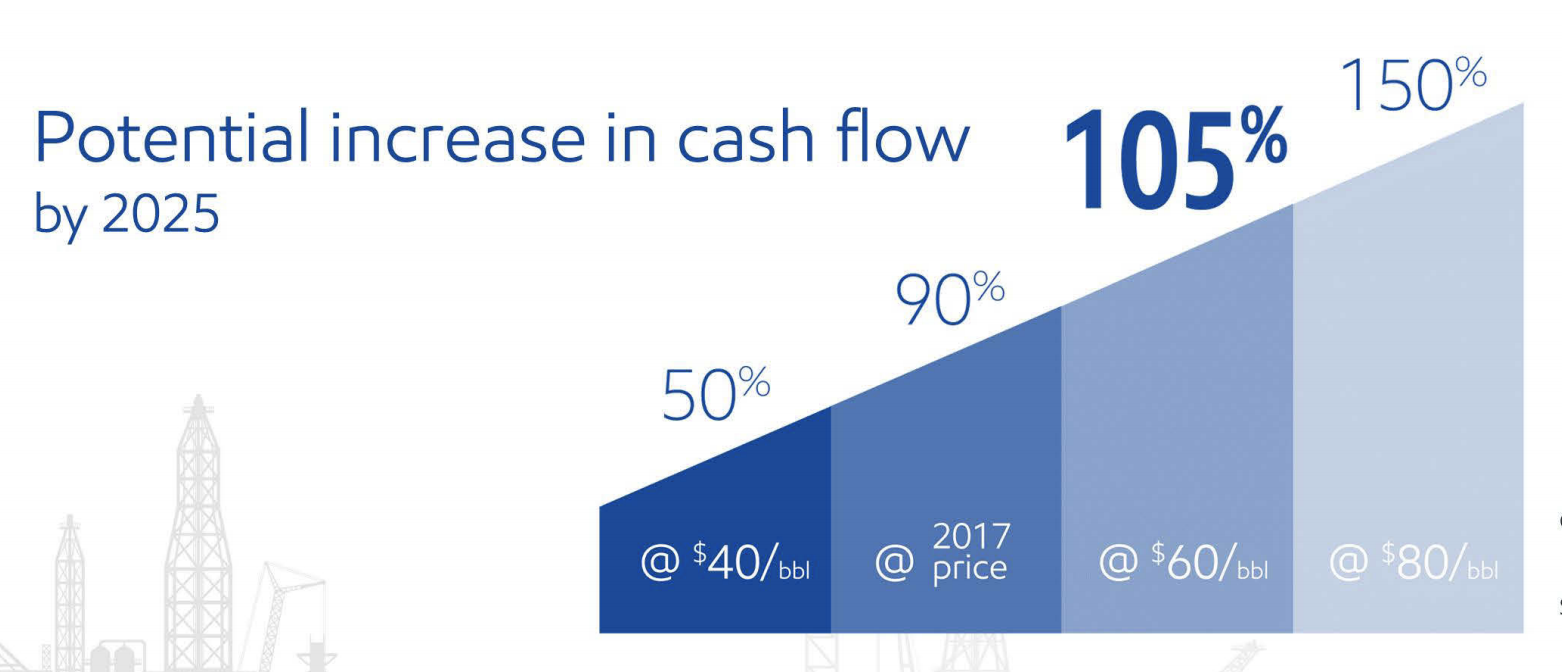

The most important benefit would be the expected strong growth in its operating cash flow, which is expected to soar by between 105% and 150% if oil prices average between $60 and $80 per barrel over that time.

Source: Exxon Mobil Investor Presentation

If those assumptions prove true, then Exxon’s free cash flow (what funds the dividend) might rise to $31.5 billion to $45 billion annually over the next seven years (up from about $13 billion in 2017).

And even if oil prices average much lower, $40 per barrel, Exxon expects to still see strong growth in free cash flow that would allow it to maintain its status as a dividend aristocrat (the firm just raised its dividend by 6.5%, marking its 35th straight year of increases).

However, as The Wall Street Journal noted earlier this summer, Exxon's reputation as an excellent capital allocator has lost some of its shine over the past decade.

The company pursued a number of big upstream projects in costlier, riskier areas (Canada's oil sands, the Russian Arctic, etc.) when the price of oil traded near an all-time high. Returns on many of these investments disappointed following the oil price crash.

Exxon also bought gas producer XTO Energy for around $40 billion in 2010. Unfortunately, natural gas prices stayed lower for longer than management anticipated, forcing the company to eventually take an uncharacteristic write-down on its natural gas assets.

Worse, despite all of these investments, Exxon's production output of 4 million barrels a day has remained largely the same since its merger with Mobil in 1999.

Combined with the impact that renewable energy could have on the long-term returns earned by Exxon's planned fossil fuel investments, and it's easier to understand some of the skepticism surrounding the stock.

But There are Reasons for Optimism

The oil crash was caused by OPEC launching a massive price war with U.S. shale producers. The theory was that a global glut of oil would crash the price and force many highly leveraged, high cost U.S. shale producers out of business. Thus, OPEC could regain market share it had been losing for years.

However, rather than go bankrupt en mass, U.S. oil companies responded by cutting costs to the bone and became more productive than anyone ever imagined.

For example, before the crash it was estimated that break even prices for U.S. shale production might be as high as $85 per barrel. Today, oil companies are able to generate up to 30% annual internal rates of return on $30 per barrel oil in some cases.

And thanks to ever-improving fracking technology, Exxon thinks that breakeven prices in key U.S. shale formations like the Permian (which holds an estimated 75 billion barrels of recoverable oil equivalents) might fall to just $20 per barrel by 2025. As a result, U.S. shale producers didn’t die, but are thriving.

While no one can predict where the price of oil will head, the world's oil glut is beginning to reverse course.

According to the International Energy Agency (IEA), full year global oil demand will average 99.2 million bpd in 2018, compared to production of just 98 million bpd. Even factoring in OPEC’s recent 1 million bpd production increase, the world is still running a daily oil deficit that is slowly draining global inventories and causing oil prices to rise.

Meanwhile, thanks to massive capital spending cuts by oil companies since the oil crash, there is a growing concern that underinvestment in production growth might cause a much larger oil shortage in the coming years.

As Saudi Arabia's energy minister Khalid A. Al-Falih recently told CNBC:

"I believe if the investment flows that we have seen the last two or three years continue in the next two or three years, we will have a shortage of oil supply by 2020...between increase in demand and natural decline, we need millions of barrels every year to be brought to the market, which requires massive investment."

A major reason for this concern (that we might soon see much higher oil prices) is because global oil production declines by about 5% annually as wells become depleted, according to analyst firm McKinsey. In order to just maintain global oil supply at today’s levels, oil companies need to increase production by about 5 million bpd each year.

Source: Exxon Mobil Investor Presentation

The bottom line is that the U.S. Energy Information Administration estimates that 80% of the total oil production growth through 2040 is going to be just to replace natural production declines. That’s even factoring in rapid growth in renewable energy and storage, and large-scale adoption of electric vehicles.

This is why Exxon estimates that the oil industry will need to invest about $400 billion annually (on average), or a total of $8.8 trillion between 2018 and 2040, to meet the world’s ongoing oil demand.

So far Exxon's peers are unwilling to increase their spending, but the company believes that it is ahead of the curve and its big spending hikes will ultimately give it a major advantage over its rivals in the future.

Major oil projects have long lead times (up to five years), and so by spending big earlier than other companies, Exxon could be poised to profit more from long-term secular trends in the global economy and its core energy markets. Only time will tell.

Closing Thoughts on Exxon's Performance

Exxon’s ambitious plans to ramp up its capex budget in the coming years are certainly risky. After all, while oil prices are rising now, history shows they can be extremely volatile and hard to forecast.

However, Exxon deserves the benefit of the doubt, especially in light of the energy market's long-term fundamentals and the steadily rising demand trend for oil for the foreseeable future. While demand for oil may be only growing at about 1.5% per year, a 5% decline rate in oil fields around the world means that the industry will need to step up investment if it is to meet the needs of a growing and richer world over the next decade and beyond.

So while it’s certainly possible that Exxon’s large investment plans might not work out (cost overruns, project delays, global recession causing another oil crash, a surge in renewable energy adoption), it seems more likely that Exxon will succeed in meaningfully growing its production and free cash flow over the coming seven years.

As a result, Exxon’s dividend is likely to remain among the safest in its industry, and its 35-year record of consecutive dividend increases should remain intact. With Exxon’s yield now at a nearly 20-year high, the stock could be interesting for high-yield investors who are interested in making a contrarian bet in their diversified income growth portfolios.