Philip Morris's Dividend Expected to Remain Safe Despite Disruptions in Russia and Ukraine

Shares of Philip Morris International have slumped 15% since Russia invaded Ukraine on February 24. Unlike most companies headquartered in America, Philip Morris has meaningful ties to Russia and Ukraine.

Russia accounted for 6% of the firm's 2021 net revenues, and Ukraine added another 2%. These countries also played a key role in Philip Morris's push into so-called reduced-risk products such as heated tobacco, which represented 29% of net revenues last year and are the firm's primary long-term growth driver.

Philip Morris's heated tobacco volumes grew 25% in 2021, and Russia accounted for 17% of all shipments. Ukraine has also been called out as an important contributor here, suggesting both countries could combine for over 20% of Philip Morris's heated tobacco volumes.

Further complicating the picture, Philip Morris's annual report states that the company owns 39 manufacturing facilities, with Russia cited as having at least one of the firm's largest factories. Of this group, 7 facilities also produce heated tobacco units, presumably including Philip Morris's operations in Russia.

Philip Morris on March 9 activated plans to scale down its manufacturing activities in Russia amid ongoing supply chain disruptions and the evolving regulatory environment. Planned investments in Russia have also been suspended.

Philip Morris previously temporarily suspended its operations in Ukraine, including at its sole factory in the country's second largest city, Kharkiv. The company will continue paying all 4,500 employees it has in Russia and Ukraine and pledged $10 million to support international humanitarian efforts.

Putting aside the tragic nature of the events unfolding in Ukraine, Philip Morris appears to have the financial strength to maintain its dividend and long-term investments in reduced-risk products despite these setbacks.

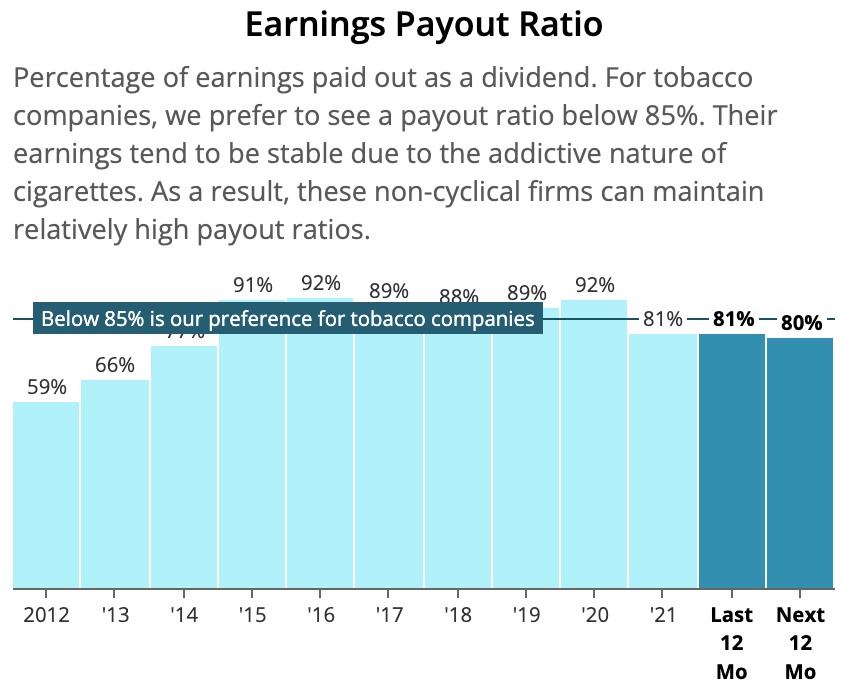

The cigarette maker's Eastern Europe segment includes Russia and Ukraine, in addition to Israel and parts of Southeast Europe and Central Asia. If this division's profits went to zero, we estimate Philip Morris's payout ratio would rise from about 80% to 89%, a level the business has operated at before.

Source: Simply Safe Dividends

With an A credit rating, Philip Morris also has flexibility to deal with one-time costs that could be required to shift or upgrade parts of its manufacturing footprint.

The biggest disappointment would be a temporary contraction in Philip Morris's heated tobacco business if operations never resume in Russia or Ukraine.

However, this would not negate the firm's leading technology investments in cigarette alternatives or ambitions for its heated tobacco device to reach 100 markets by 2025, eventually lessening the importance of any one country as the business scales.

We will continue monitoring Philip Morris's business as the war in Ukraine evolves. While this year could prove challenging, we ultimately expect the firm's dividend and long-term outlook to remain intact.