International Paper's Rebased Dividend Supported by Strong Balance Sheet and Steady Cash Flow

International Paper completed the spin-off of its printing papers business on October 1 and, as expected, rebased its dividend on Tuesday to reflect the firm's lower cash flow.

The dividend was reduced by about 10% (better than management's original estimate of a 15% to 20% cut). With the spin-off complete and the rebased dividend in place, we are upgrading the firm's Dividend Safety Score to Safe.

While box manufacturing is a cyclical business, International Paper's solid dividend coverage, strengthened balance sheet, and improved business mix seem likely to protect the dividend over a full economic cycle.

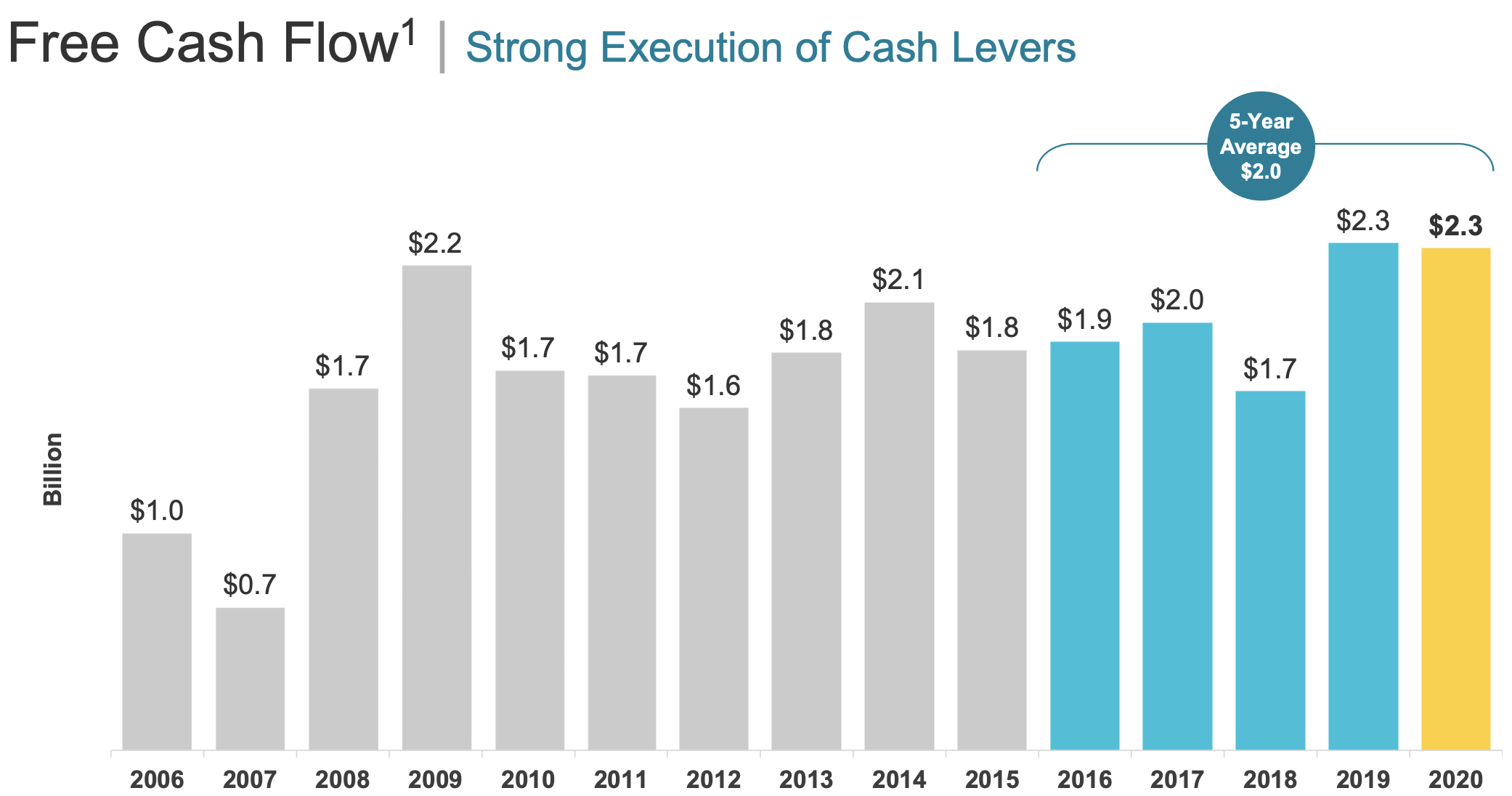

International Paper targets a free cash flow payout ratio of 40% to 50%. Based on the company's adjusted free cash flow metric, the packaging giant has reliably met its goal for more than a decade.

The current dividend costs about $725 million annually, and free cash flow has remained between $1.6 billion and $2.3 billion each year since 2008.

Source: International Paper Investor Presentation

But this consistent cash flow generation didn't stop International Paper from slashing its dividend by 90% in 2009, breaking its streak of paying dividends without interruption since 1946.

The steep dividend cut was necessitated by International Paper's heavily indebted balance sheet, which swelled in 2008 after completing a $6 billion deal to acquire Weyerhaeuser's packaging assets.

Management has prioritized deleveraging in recent years, reducing the firm's leverage metrics to their lowest levels in more than a decade and reinforcing International Paper's BBB investment-grade credit rating.

Source: Simply Safe Dividends

As Chairman and CEO Mark Sutton explained in June, this financial flexibility positions International Paper to not only defend its dividend during a downturn but also take proactive action to increase shareholder value, such as repurchasing stock at distressed prices:

I can't remember a time in...any kind of recent modern history that we have had the opportunity to have all options on the table for capital allocation through a cycle. Usually, because of the way we built the company, when there was a downturn, we were deleveraging from a prior acquisition that might have happened a couple of years before.

I want to see us in a position, and we're getting close to that, where we have the low end of our range on debt, the opportunity to continue to grow our dividend, continue to be more strategic in share repurchases, especially if there's a downturn, and we can buy more shares at a trough environment, which we haven't been able to do in the past because of the balance sheet.

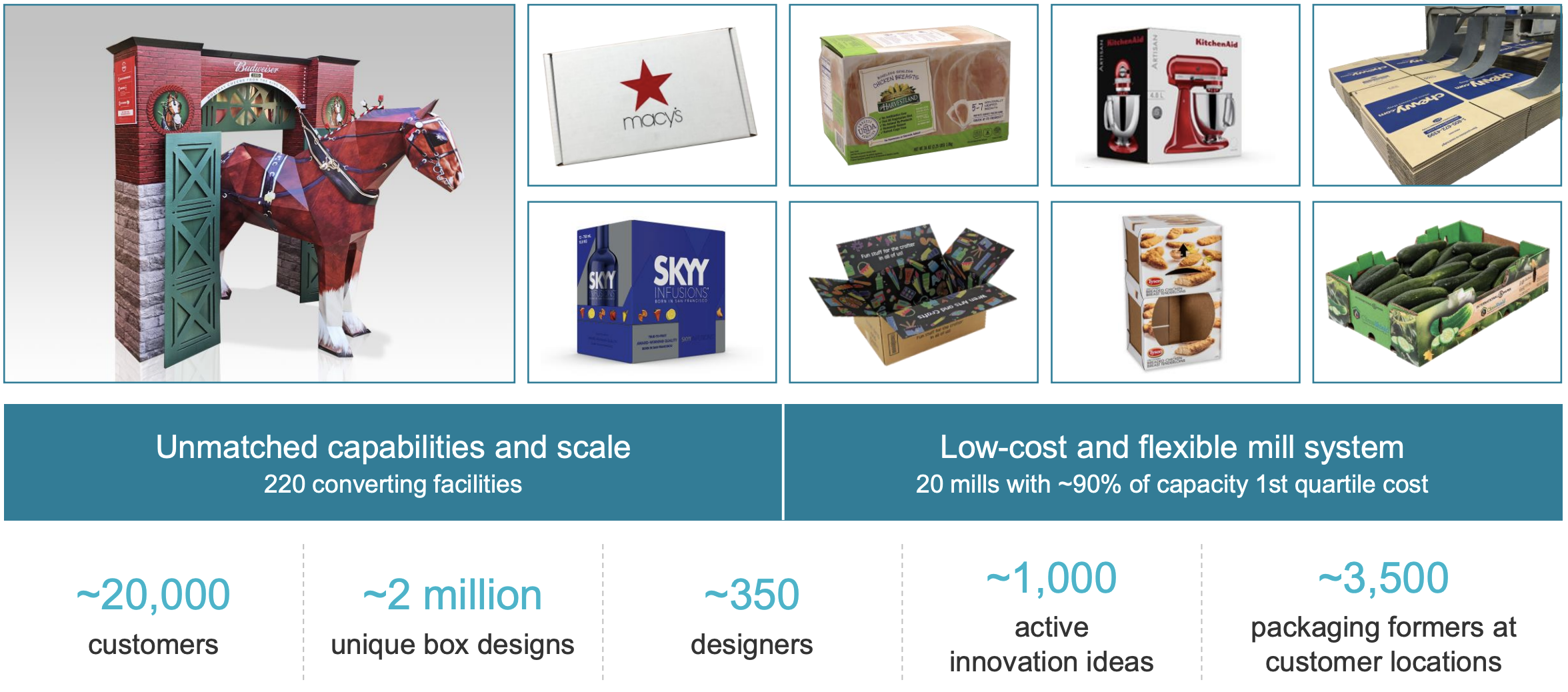

Looking ahead, we expect International Paper to remain a force for years to come. After shedding its lower-margin printing papers business, which was in secular decline and accounted for close to 20% of revenue, International Paper's industrial packaging division will drive nearly 90% of sales.

This vertically-integrated business makes linerboard and heavy-duty cardboard boxes used to move food and beverages (45% of sales), other non-durables such as chemicals and tissues (30%), and durable goods used in e-commerce and shipping (25%).

Source: International Paper Investor Presentation

The containerboard market has consolidated over time to be dominated by just a handful of companies, and International Paper is the largest player with over 30% share in North America.

As a result, nearly all of the company's production capacity is positioned in the first quartile on the global cost curve, and the shrinking number of competitors has helped the industry's operating rates and pricing discipline.

While boxes are a commodity product, demand is slowly but steadily growing thanks to stable shipment trends in core markets such as food manufacturing, as well as strong increases in online sales of goods that now need to be shipped.

Overall, International Paper may appeal to income investors seeking a dependable cash cow with modest growth prospects.

The company will remain sensitive to general economic conditions and shifts in industry capacity, but International Paper's improved balance sheet and business mix should help keep the dividend protected in good times and bad.