BP's Debt Reduction Strengthens Dividend Profile as Business Transition Begins

Faced with low oil prices, a stretched balance sheet, and growing pressure to invest more in low-carbon energy, BP in August 2020 slashed its dividend by 50% and unveiled a business transformation plan.

Following the dividend cut, we maintained BP's Unsafe Dividend Safety Score in recognition of the international oil major's still-elevated leverage and the challenging commodity price environment.

Since then, crude oil has nearly doubled to $75 per barrel – well above the $45 level BP needs to cover its capital spending and dividend. This helped BP hit its debt reduction target recently, providing more support for its A- credit rating from S&P.

In recognition of BP's improving financial health, we are upgrading the firm's Dividend Safety Score to Borderline Safe. However, investors should be aware that BP expects its business mix to shift dramatically in the decade ahead.

Oil companies have long argued that fossil fuels will remain a core component of the world's energy mix – a position we agree with.

But there is concern that these firms, which are among the largest producers of greenhouse gas emissions, are not prepared for downside demand scenarios.

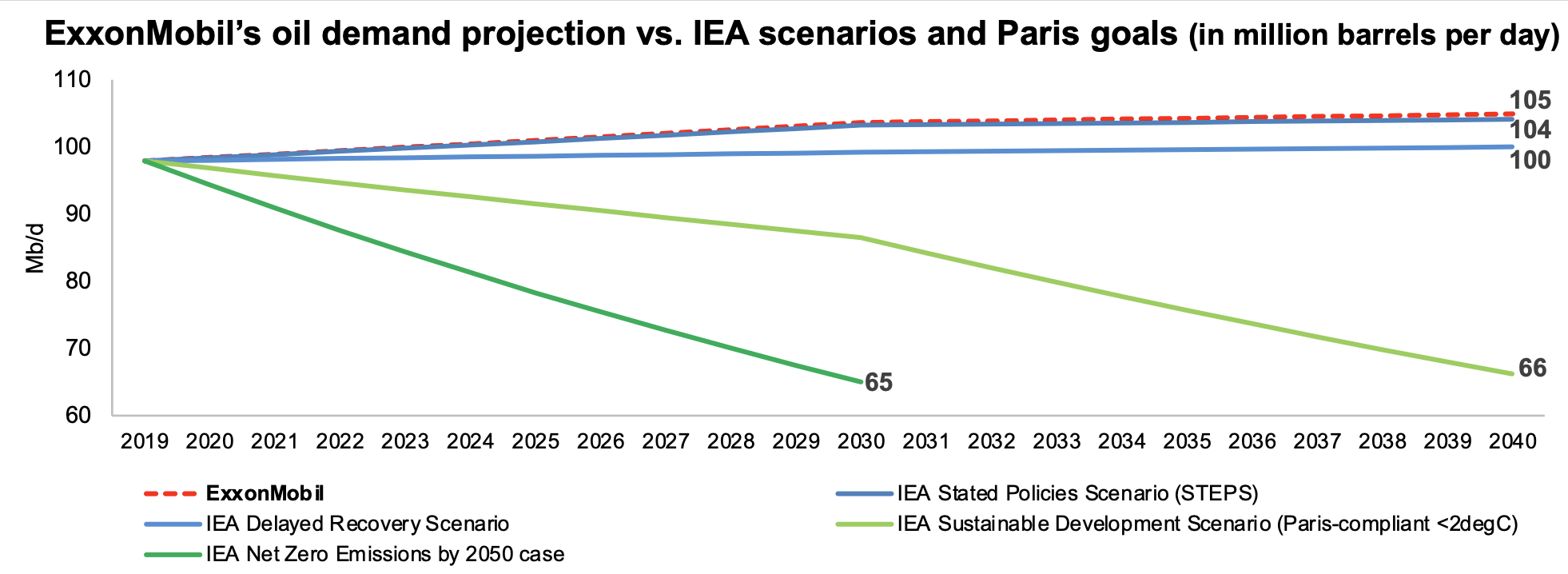

The world's push for cleaner power could see oil consumption fall around 30% within a decade, according to one scenario modeled by the International Energy Agency (IEA) that accounts for many countries reaching their goal of net zero emissions by 2050.

Source: Engine No. 1 Presentation on Exxon Mobil

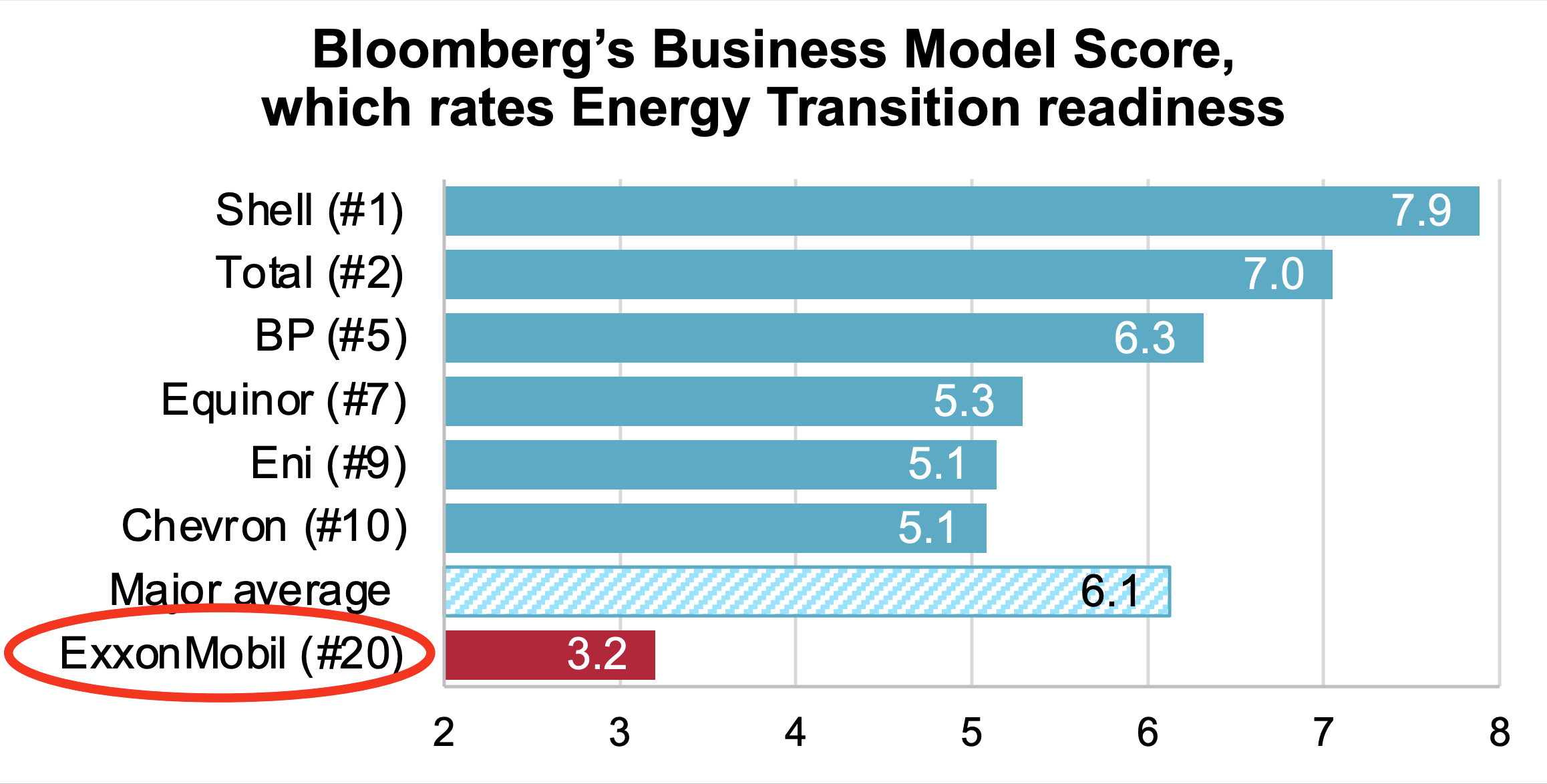

Unlike American rivals Exxon and Chevron, Europe's oil giants have more eagerly embraced the movement to combat climate change as the world seeks to cut carbon emissions.

Shell, Total, and BP rank well ahead of the U.S. oil majors in terms of energy transition readiness with scores between 6 and 8 out of 10, according to a 2021 study conducted by Bloomberg.

Source: Engine No. 1 Presentation on Exxon Mobil

In large part, the rankings above reflect the ideological differences between American and European oil majors, which Bloomberg summarized:

"On one side of the Atlantic, BP, Shell and Total are trying to make themselves going concerns for a low-carbon age, diluting their fossil-fuel businesses with plans to build significant revenues from renewable energy. Exxon and Chevron -- insulated from the pressure applied by European investors and politicians -- are charting a different course: keep pumping as profitably as possible and hand the cash back to investors. Like Big Tobacco, they’re increasingly courting shareholders willing to put returns above the harm their product causes."

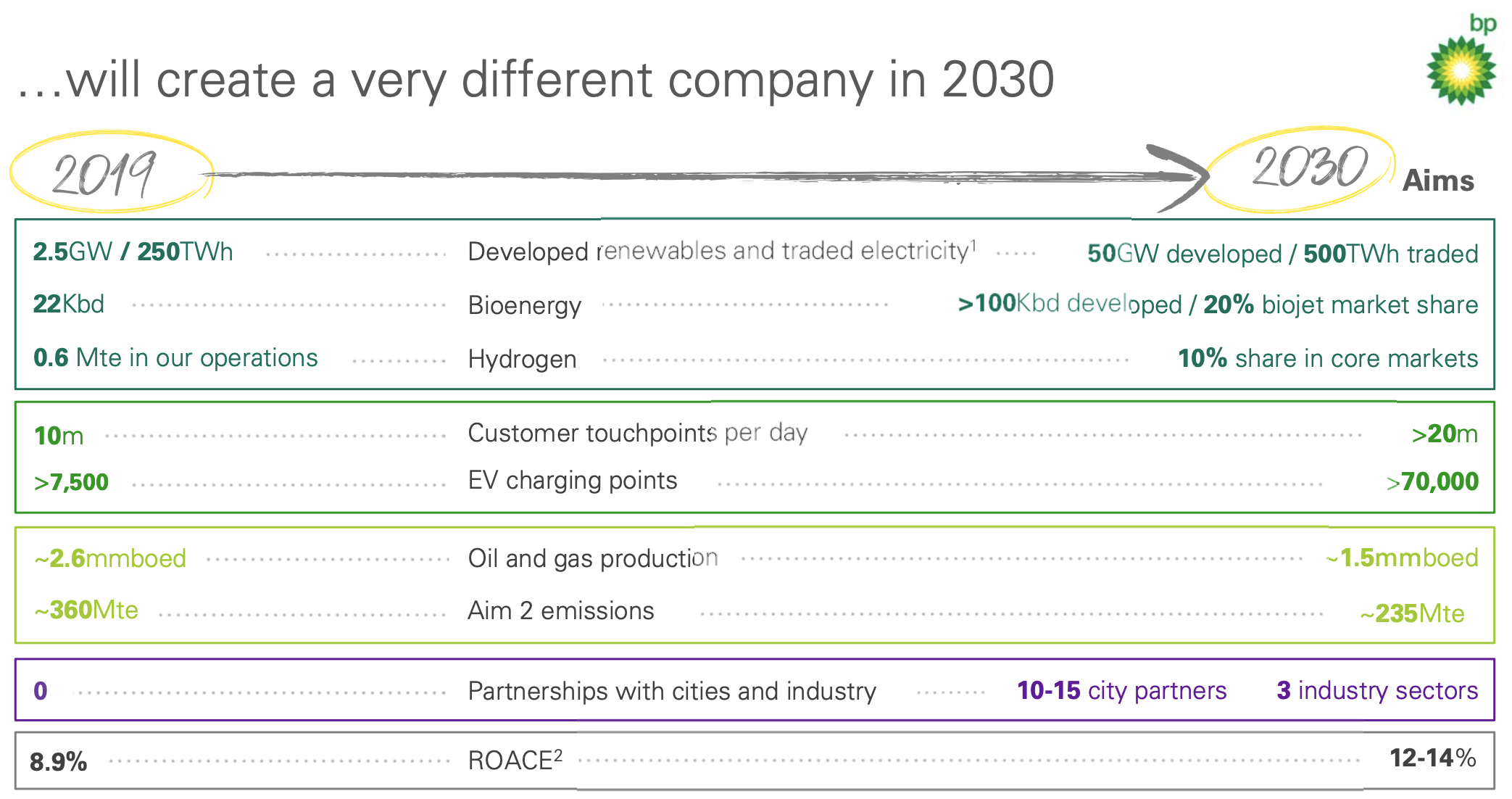

As part of this push, BP expects to reduce its oil and gas production by 40% over the next decade, with most of the decline ramping up after 2025. Investments in low-carbon assets and electric vehicle charging points are expected to see a ten-fold increase, and renewable energy generating capacity will rise by twenty-fold.

Management expects to be directing at least 40% of BP's investment into these areas by 2030, representing $5 billion of annual spending on low carbon compared to $750 million last year. This marks a massive shift in capital allocation priorities.

Source: BP Investor Presentation

Expanding into wind and solar power to supply cleaner electricity may lessen BP's dependence on commodity cycles, but investors are skeptical that these areas can provide attractive returns compared to the oil and gas business.

BP targets returns of "at least 8% to 10%" from its investments in renewables, indicating these projects will not be as profitable as its core fossil fuels, which management expects will earn returns around 13% over the next five years.

Despite the lower-return profile of low-carbon energy, BP believes the market will value this business more because of the relative stability it offers. Compared to hydrocarbons, which experience boom-and-bust cycles, renewables can offer more predictable returns through long-term contracts with their customers.

Ultimately, it will take years to gauge whether BP can profitably scale its renewables business. Ratings agency Fitch expects BP's business mix transition to happen gradually, with low-carbon assets contributing only minimally to the firm's operating cash flow up to 2025.

During this transition period, income investors should expect minimal, if any, dividend growth. Management has emphasized the importance of having a "resilient" dividend, noting that increases could make it harder to cover the payout during downturns. Share buybacks will instead serve as the primary way to return surplus cash flow.

Overall, BP has embraced an ambitious plan to mitigate long-term risks poised by the green energy transition and the potential use of carbon taxes. But the actions BP plans to take over the next decade carry their own risks, and the firm's track record does not instill much confidence in management's ability to execute.

BP has historically earned lower returns on capital employed compared to its peers, and the firm's worker safety record is among the worst of any large U.S. industrial company, underscoring BP's questionable project management skills.

It's also worth noting that BP several decades ago attempted a similar push into low-carbon energy, investing billions of dollars only to later abandon its plans in the face of unsatisfactory returns and a desire to cut costs.

Pivoting successfully into new businesses is hard. Contrarian income investors who believe in oil's staying power may want to consider sticking with energy companies such as Chevron which plan to primarily continue doing what they know how to do well.

We will continue monitoring BP's plans and provide updates as needed. Until BP reduces its leverage further and demonstrates it can maintain its earnings power with less reliance on fossil fuels, we are unlikely to upgrade the firm's Dividend Safety Score again.