Simon's Outlook Stabilizes as Mall Retailers Enjoy Sales Revival

Simon's Empire Mall in South Dakota – the largest mall in the state – has seen its retailers' sales exceed their 2019 pre-pandemic level, according to comments made earlier this week by General Manager Dan Gies.

Empire Mall's observation supports Simon's expectation that its mall retailers would likely see their sales start topping 2019 levels beginning in April as vaccinated consumers strapped with record excess savings return to brick-and-mortar retailers.

Malls and in-person shopping are not dead, but parts of the industry continue facing an uncertain future as more consumers embrace online shopping and retailers shrink their store footprints.

Macy's, which represents Simon's largest anchor tenant at nearly 11% of square footage, is in the middle of a three-year plan to close 125 stores, or roughly 20% of its locations.

(It's worth noting that only three of Macy's 65-plus store closures announced for 2020 and 2021 are at Simon-owned properties, highlighting the REIT's more desirable malls.)

Meanwhile, J.C. Penney (4.8% of square footage) declared bankruptcy in May 2020 and was acquired by Simon and Brookfield Asset Management in an effort to stabilize its remaining stores.

These anchor tenants and others generate less than 3% of Simon's rent (despite representing around 30% of total square footage) but serve an important role in bringing shoppers to the rest of a mall's smaller tenants.

Unfortunately, many of Simon's non-anchor tenants are also focused on shrinking their footprints as they prioritize their most profitable locations.

Simon's largest tenant, The Gap (3.2% of rent), is in the process of permanently shuttering around a third of its fleet, abandoning traditional malls in favor of strip centers and outlets. About a third of The Gap's closures that have occurred since January 2020 were at Simon-owned properties, according to our analysis.

L Brands, which operates stores under the Victoria's Secret and Bath & Body Works, shut down over 20% of its stores in 2020 with plans to shutter another 4% to 6% of its fleet this year. L Brands is Simon's second-largest tenant, accounting for 2.2% of rent.

Other mall-based businesses are undertaking the same analysis and may shrink or eliminate underperforming locations as their leases come up for renewal.

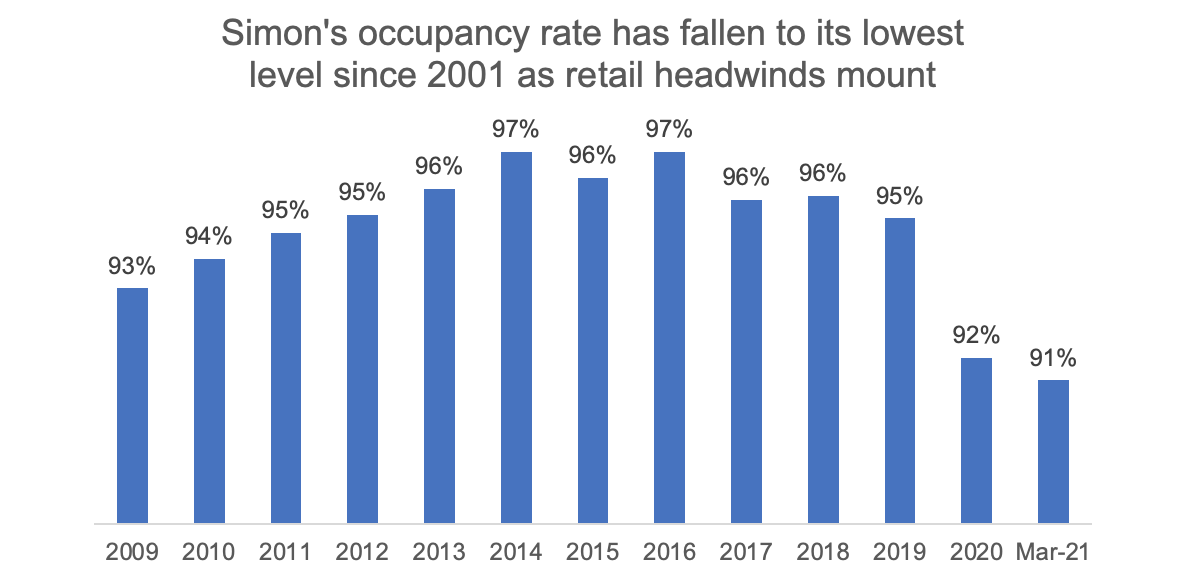

Coupled with some retailers going out of business due to last year's pandemic-induced lockdowns, Simon's occupancy rate has slumped to its lowest level in two decades.

Source: Simon Annual Reports, Simply Safe Dividends

Management hopes occupancy recovers to 2019 levels by 2022 or 2023, leading to a rebound in cash flow as vacant storefronts are filled. But the path could be bumpy since leases representing more than 30% of Simon's revenue expire over the next three years.

Retail has become a renters' market with mall vacancy rates at a record level, according to Moody's Analytics. Moody's expects "downward pressure on rents and vacancy rates through this year and into 2022" as retailers move or downsize as their leases expire.

Other real estate experts have an even bleaker outlook for the industry.

Nothing lasts forever, and many of the problems malls initially addressed are increasingly being solved in other ways. The weakest properties probably won't survive.

America's first enclosed mall was built in 1956, and the nation hasn't looked back. About 1,500 malls were built in the U.S. from 1956 through 2005, providing hubs for social gathering and shopping throughout America's booming suburbs.

By 1975, malls accounted for 50% of U.S. retail dollars spent, representing an impressive 13% of GDP. So much property was developed that by 2017 America had an estimated 26 square feet of retail for every person in the country, compared with less than 3 square feet per capita in Europe, according to Time.

But now, in the age of Amazon, the technology-driven shift in retail distribution and socialization preferences reduces malls' value proposition, threatening to leave a glut of capacity behind.

Given this backdrop, Simon is the best house in a bad neighborhood thanks to its focus on "Class A" malls, which are perceived to be of the highest quality given their higher sales per square foot and stronger traffic.

Coupled with Simon's well-located suburban real estate, the firm's properties have greater potential to remain a core part of brick-and-mortar shopping. And as consumer preferences evolve, the firm can gradually adapt its portfolio with redevelopment work.

Redevelopment projects enable Simon to bring in non-traditional mall tenants such as gyms, hotels, and entertainment centers to help preserve the network effects that are so crucial to a mall's health.

There is not necessarily a major urgency for Simon to transform its properties since many of its locations are on their way to recovery. But continuing to execute on these projects, especially at malls that are not faring as well, is important to protect Simon's long-term outlook.

From a financial perspective, Simon looks positioned to continue investing in its real estate projects while maintaining its dividend.

Before the pandemic struck, Simon had earmarked $1.4 billion of spending in 2020 to improve its mall properties. Management then postponed some projects to preserve capital, reducing the annual run-rate of redevelopment investments to a few hundred million dollars.

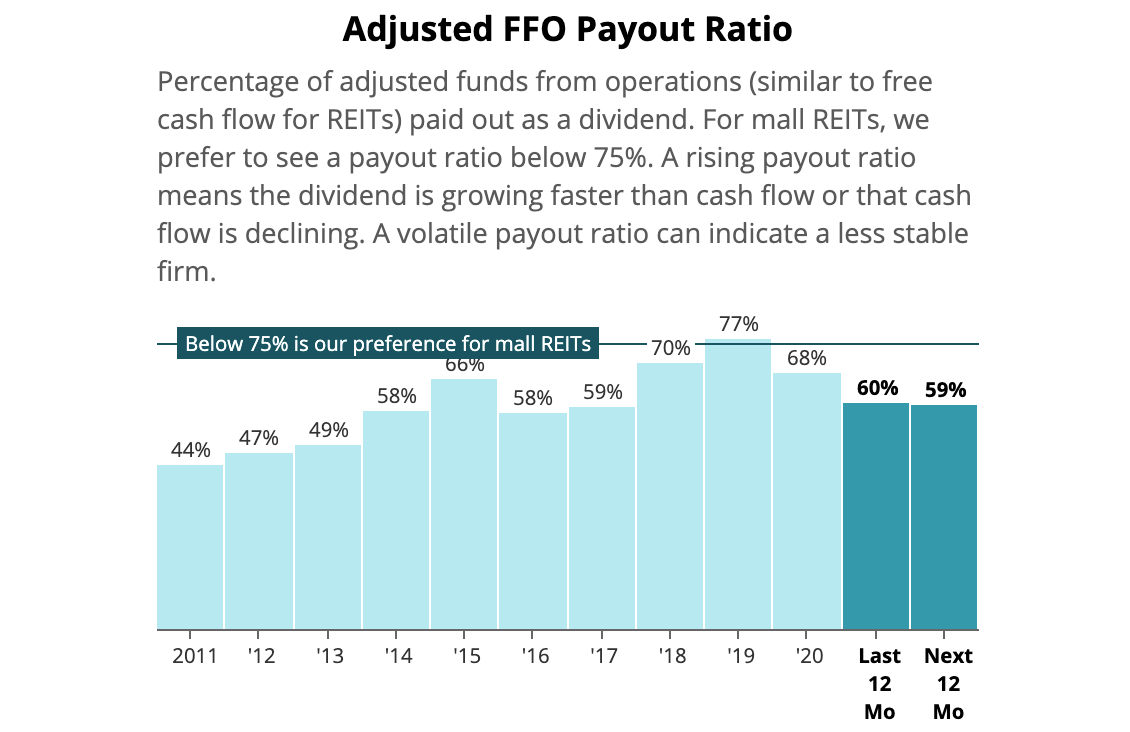

Following Simon's 38% dividend cut in July 2020, we estimate the firm will retain around $1 billion of cash flow annually after paying dividends. This should be sufficient to fund the majority of the firm's redevelopment projects, and Simon's A- credit rating provides additional flexibility to tap debt markets if needed.

As occupancy hopefully recovers, Simon's retained cash flow will further improve. Either way, the company's payout ratio near 60% provides a reasonable margin of safety. Especially with many mall retailers seeing a recent rebound in business.

Source: Simply Safe Dividends

Overall, Simon's short-term outlook appears to be stabilizing as its malls and outlets experience a recovery in traffic. However, the firm must continue navigating a tough retail environment as tenants shrink their footprints and fight for more favorable lease terms.

We would consider upgrading Simon's Dividend Safety Score if over the next year the firm makes progress improving its occupancy rate, holding its rent rates, and demonstrating that the bulk of its malls remain in stable condition.

As always, we will continue monitoring Simon's recovery and provide updates as needed.