With Government Aid Diminishing, Omega's Tenants Face Uncertain Future

Omega Healthcare continues collecting virtually all rent due despite the crushing blow dealt by the pandemic to many of its skilled nursing tenants (over 80% of revenue).

Years of falling occupancy (oversupply), rising labor costs, and changes to Medicare reimbursement rates have contributed to the industry's long decline in profitability.

Covid exacerbated these challenges. Occupancy across Omega's portfolio steadily eroded from 84% in January 2020 to just 73% in April 2021.

Fewer residents have moved in due to lower elective surgery volumes at hospitals and a growing preference for home health services, which can provide more lifestyle flexibility and peace of mind in the midst of a pandemic.

Meanwhile, operating expenses have rocketed higher. Finding qualified labor has become even more challenging and costly, and nursing homes have had to invest heavily in personal protective equipment and Covid testing to keep residents safe.

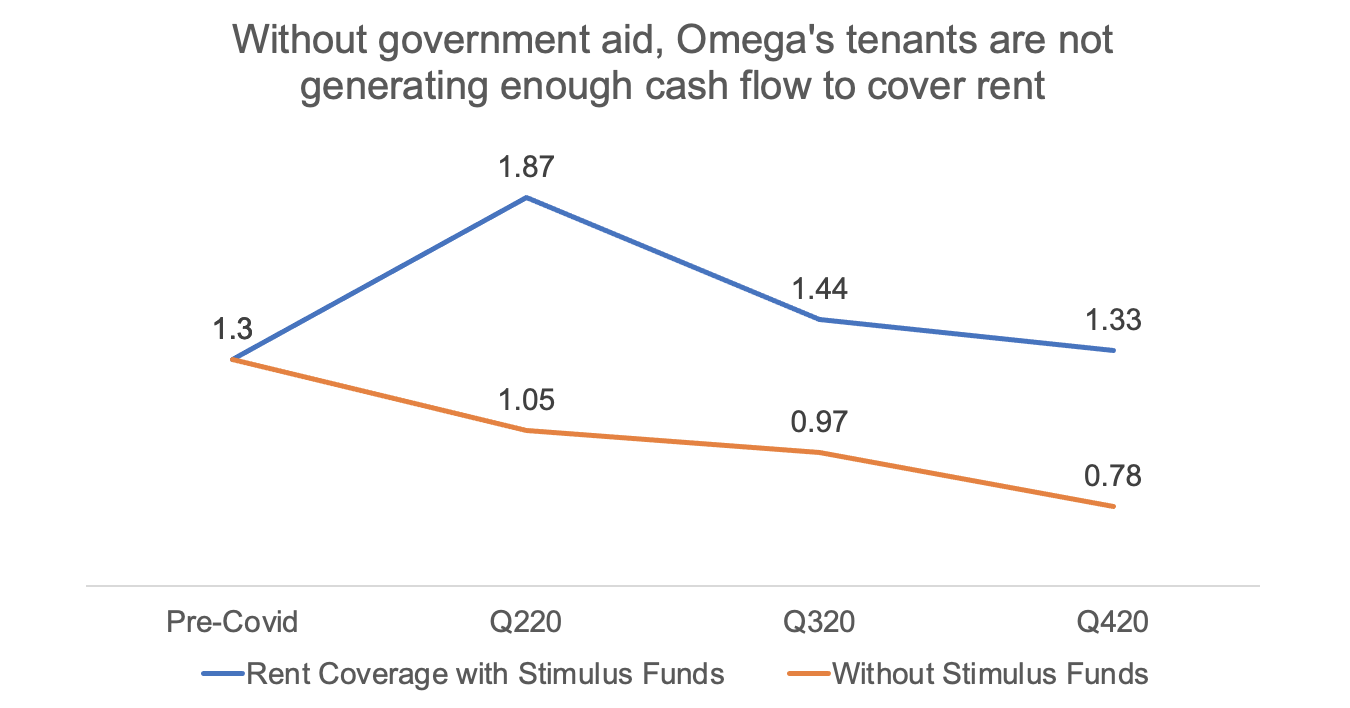

Prior to the pandemic, Omega's tenants had a rent coverage ratio (i.e. pre-rent cash flow, or EBITDAR, to rent expense) of 1.3x.

In other words, for every $1 of rent owed, tenants were generating about $1.30 of pre-rent cash flow. All else equal, their cash flow could fall around 20% before rent would no longer be covered.

With occupancy plunging and expenses spiking last year, rent coverage fell to just 0.78x in the fourth quarter of 2020. Nursing home operators, in aggregate, were no longer positioned to meet the payment terms of their leases with Omega.

But government aid bailed them out, at least temporarily. The CARES Act passed in March 2020 provided stimulus for the nursing home industry, which primarily receives revenue through reimbursements from government programs like Medicaid and Medicare.

Thanks to these relief funds, Omega's tenants in the second quarter of 2020 saw their rent coverage ratio (including stimulus funds) jump to its highest level in at least a decade.

Source: Simply Safe Dividends, Omega Healthcare Filings

But rent coverage has continued sliding since last summer with occupancy remaining weak, and government aid won't last forever.

On Omega's first-quarter earnings call in early May, management cautioned that the second half of the year could be a period of stress for nursing home operators if federal and state governments do not supply more funding:

"Although we have seen occupancy stabilize and increase slightly as vaccines have rolled out, it is not clear that the pace of occupancy recovery will be sufficient to avoid industry-level cash flow issues.

"With an estimated $24.5 billion remaining in the Provider Relief Fund, and the likelihood of provider funding requests well in excess of this amount, we expect certain providers in the industry may have shortfalls...

"As we look at our operators, obviously, they paid through April. They're still in pretty good shape from a liquidity perspective, but with no more funding, I think you see that stress start to hit operators in the back half of the year."

– CEO Taylor Pickett

Hopefully occupancy strengthens significantly as the year rolls on to improve operators' cash flow. But it seems likely that some tenants will need to negotiate rent deferrals or make permanent changes to their lease terms since rent is one of operators' largest costs.

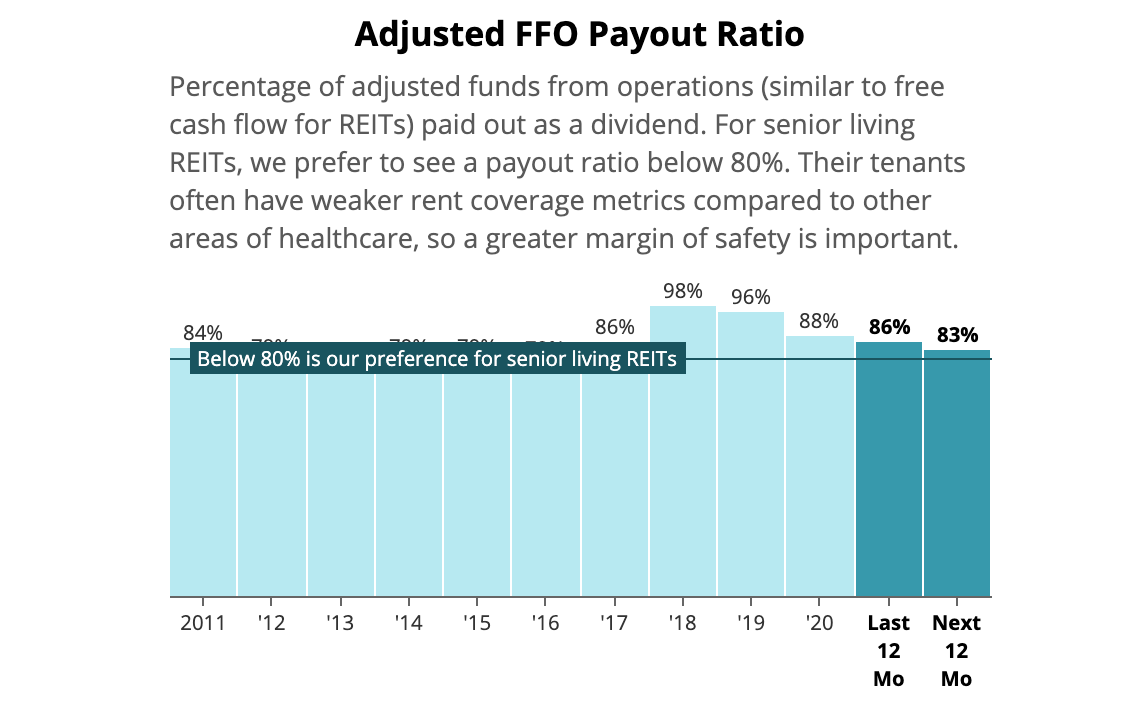

Bracing for these potential challenges, Omega has held its dividend flat since late 2019 to help work down its payout ratio to a projected 83% this year. We estimate Omega's rental revenue could fall by around 15% without pushing its payout ratio above 100%.

Source: Simply Safe Dividends

It's hard to say if that margin of safety will be sufficient with many operators not yet being able to cover rent without government aid.

In September, ratings agency Fitch estimated that Omega will face permanent rent reductions equal to 10% of rental revenues starting in 2021.

Fitch warned that permanent rent cuts above that amount could cause Omega's leverage ratio to exceed 5.5x (up from 5.1x currently), a level that could cause the REIT to lose its investment-grade credit rating.

If such a scenario unfolded, we believe Omega would consider reducing its dividend, which Fitch also noted is one of Omega's "additional levers to stabilize leverage if rent reliefs meaningfully impact leverage metrics."

Based on what we know today, we are maintaining Omega's Borderline Safe Dividend Safety Score. The company's dividend continues to hinge on the industry's occupancy rate recovering to pre-pandemic levels before stimulus funds are exhausted.

Occupancy has stabilized and slightly increased as vaccines have rolled out, but operators still have a long way to go to return to normal and cover rent on their own.

We will continue monitoring trends in Omega's business and provide updates as needed.