STORE Capital's Dividend Safety Improves as Rent Collection Returns to Pre-Pandemic Levels

In May last year when pandemic uncertainties were at their peak, STORE Capital's rent collection rate fell to just 64% as restaurants (14% of pre-pandemic rent), gyms (5%), movie theaters (5%), and other "non-essential" tenants braced for a long downturn.

At this level of rent collections, cash flow no longer covered the dividend. And management had made it clear they were opposed to borrowing money to fund the dividend, putting the payout in peril if cash flow did not rebound quickly.

Fortunately, over the year since conditions have recovered quicker than many had expected as the economy reopened. STORE was able to collect 95% of rent payments last month, and occupancy has remained strong with 99.6% of its properties actively rented.

Cash flow visibility looks solid going forward as well. Only 4% of STORE's leases mature over the next five years, and the retail REIT continues to boast a lengthy weighted average lease term of 14 years.

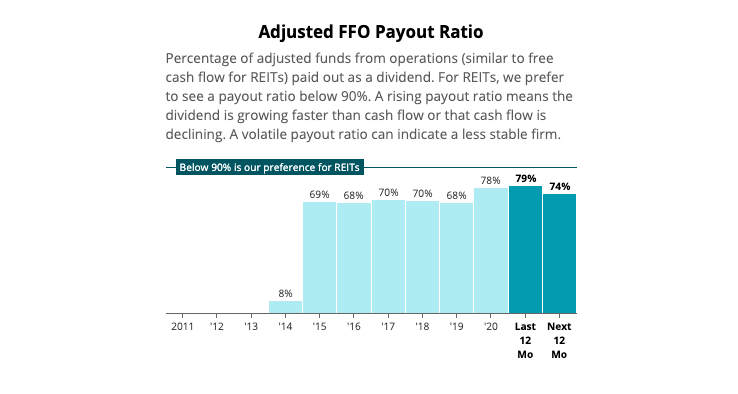

With STORE's portfolio looking resilient, management expects adjusted funds from operations (AFFO, a measure similar to free cash flow for REITs) to fall in the range of $1.90 to $1.96 per share this year.

That is comparable to STORE's pre-pandemic cash flow and enough to comfortably cover the $1.44 per share dividend. Should this forecast be realized, STORE's payout ratio would return towards historical levels.

Source: Simply Safe Dividends

Compared to other retail REITs such as Realty Income and Spirit Realty, which maintain payout ratios around 80%, STORE has historically targeted stronger dividend coverage. This helped protect the dividend in 2020 and even led to a modest increase last fall.

Looking forward, it's possible some of the REIT's tenants might struggle should the economic recovery continue in fits and starts, but the overall outlook is positive.

STORE's portfolio diversification helps reduce risk too, with more than 2,500 single-tenant properties dispersed throughout the country. These properties are used in over 100 different industries and are filled with a diverse mix of tenants, of which none account for greater than 3% of total rent.

Coupled with the firm's BBB investment-grade credit rating and healthy liquidity, STORE appears well-positioned to navigate future economic downturns.

Overall, we feel comfortable returning STORE Capital's Dividend Safety Score to a Safe rating and believe it's likely the company will continue to extend its 6-year dividend growth streak.