Welltower Sees Senior Housing Occupancy Rise for First Time Since 2019

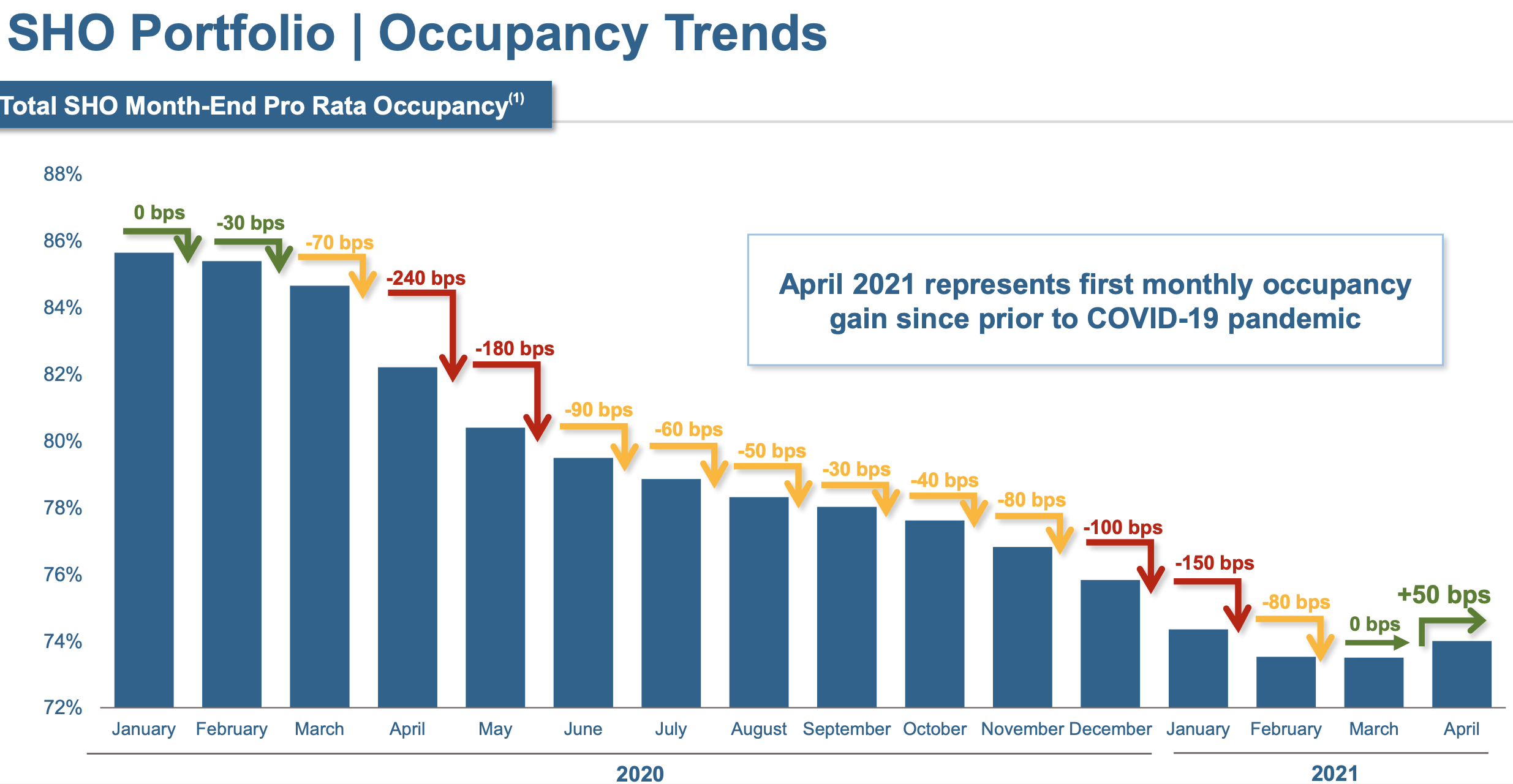

April 2021 marked the first monthly occupancy gain in Welltower's senior housing operating (SHO) portfolio since prior to the pandemic.

With the vaccine rollout enabling many senior living communities to drop comprehensive move-in restrictions that were implemented last year to reduce the risk of COVID-19 transmission, Welltower is hopeful that the industry has finally bottomed out.

Source: Welltower Investor Presentation

Prior to the pandemic, the senior housing industry had never seen occupancy dip below 80%. But within just 15 months, Welltower's occupancy fell from nearly 86% to less than 74%.

Welltower generates approximately 60% of its net operating income (NOI) from senior housing. Most of its tenants have continued honoring their lease terms, with rent collection rates across all properties exceeding 95% each quarter over the past year.

However, around two-thirds of Welltower's senior housing exposure is from properties it runs directly by partnering with an operator rather than leasing the space to a tenant. This exposed the REIT directly to the industry's declining cash flow.

Welltower's senior housing operating portfolio (39% of NOI) reported a 44% decline in same-store net operating income last quarter, reflecting lower occupancy and higher expenses driven by elevated staffing needs and personal protective equipment.

A recovery in this business is key to restoring Welltower's earning power and returning the dividend to growth. Management believes the SHO portfolio's NOI, excluding government aid, would nearly double if the business returned to its pre-COVID occupancy level.

We estimate a full occupancy recovery, plus contributions from development projects, would boost Welltower's firm-wide NOI by around 30%. This would help the REIT lower its projected payout ratio of 89%, its highest level since 2017 despite Welltower's 30% dividend cut last year.

Source: Simply Safe Dividends

We would like to see Welltower improve its dividend coverage before considering upgrading the firm's Borderline Safe Dividend Safety Score.

It's unclear how long the senior housing industry will take to recover and if it will ever return to pre-COVID occupancy levels.

Meanwhile, on the triple-net side of the business, leases representing around 15% of net operating income have rent coverage ratios (i.e. pre-rent cash flow, or EBITDAR, to rent expense) below 1.05x.

In other words, for every $1 of rent owed, these tenants generate $1.05 or less of pre-rent cash flow. Some of these operators could struggle to cover rent later this year and need to modify their lease terms, reducing Welltower's cash flow.

But based on what we know today, we don't expect the REIT's elevated payout ratio to threaten the dividend. A recovery in senior housing occupancy is the most important lever behind Welltower's cash flow, and it's encouraging to see that move-in activity in April already returned to pre-pandemic levels.

An occupancy-driven earnings recovery would also help reduce Welltower's leverage ratio. S&P has a negative outlook on the company's BBB+ credit rating, citing the REIT's deteriorating operating performance and elevated debt metrics.

Source: Simply Safe Dividends

We don't expect Welltower to need to take any actions to defend its credit profile. The REIT's dividend cut last year ensured its cash flow would be more than sufficient to cover its essential spending needs without needing to stretch its balance sheet.

This helped Welltower avoid needing to divest assets at fire-sale prices or bet its future on a quick recovery. The REIT now has nearly $5 billion of near-term liquidity, an amount we estimate is sufficient to cover debt maturities, development spending, and opportunistic property acquisitions for at least the next couple years.

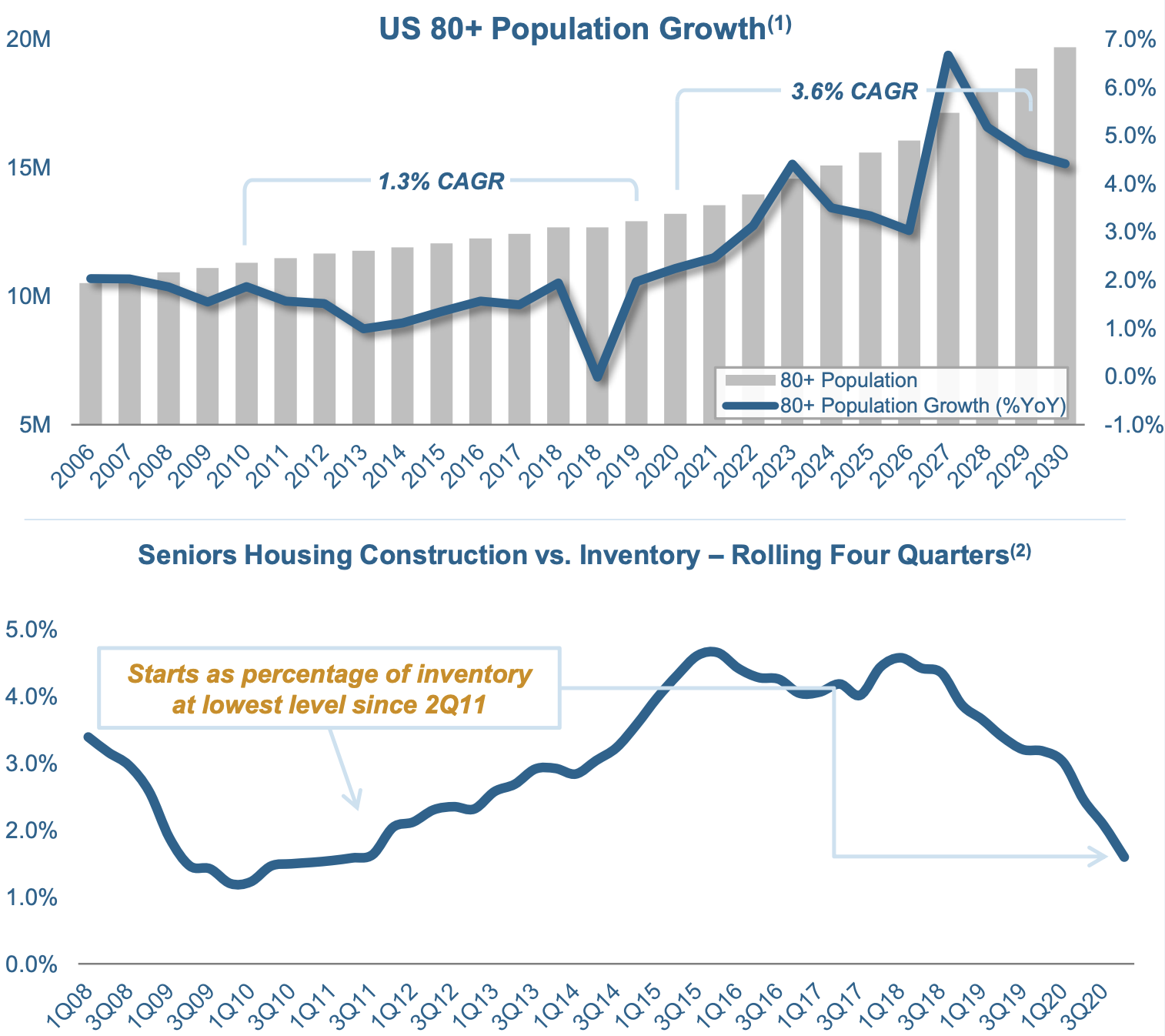

Looking further out, Welltower is optimistic that the next decade will be better than the last for the senior housing industry.

The number of Americans who are at least 80 years old is expected to rise by nearly 50% from 2020 to 2030 as this population segment's annual growth rate more than doubles compared to the previous decade.

Meanwhile, senior housing construction starts are down more than 70% from their 2017 peak to reach their lowest level in about a decade. More demand and less supply could bode well for long-term rent growth and occupancy rates.

Source: Welltower Investor Presentation

Overall, the worst appears to be behind Welltower. However, income investors shouldn't expect dividend growth to resume until the REIT's cash flow has seen a meaningful rebound, which could take at least several quarters.

We will continue monitoring the recovery in senior housing fundamentals and provide updates as necessary.