Deere & Company: Over 20 Years of Uninterrupted Dividends

Founded in 1837, Deere & Company (DE) manufactures and distributes agriculture and turf, and construction and forestry equipment worldwide.

Deere has three operating segments:

- Agriculture and Turf (68% of 2017 revenue): agriculture and turf equipment including large, medium, and utility tractors; tractor loaders; combines, cotton pickers, cotton strippers, and sugarcane harvesters. This segment also makes related harvesting front-end equipment such as: sugarcane loaders and pull-behind scrapers; tillage, seeding, and application equipment comprising sprayers, and nutrient management and soil preparation machinery.

- Construction and Forestry (19% of 2017 revenue): builds backhoe loaders; crawler dozers and loaders; four-wheel-drive loaders; excavators; motor graders; articulated dump trucks; landscape loaders; skid-steer loaders; and log skidders, loaders, forwarders, and timber harvesters.

- Financial Services (10% of 2017 revenue): finances the sales and leases of its equipment as well as offers extended warranties.

About two thirds of the company's sales are tied to its core agricultural markets. However, the company is investing aggressively into construction and forestry businesses to diversify its operations and increase the stability of its cash flow.

While Deere is a global company, 59% of the company's sales are generated in the U.S. and Canada.

Deere markets its products primarily through nearly 2,400 independent retail dealers, as well as retailers such as Home Depot (HD) and Lowe's (LOW).

Business Analysis

While the industrial sector is itself highly fragmented, companies usually focus on a few key niches where they perfect their designs and carve out competitive advantages.

For instance, Deere invests very heavily into making its products the most reliable and dependable offerings in the market, reducing customers' long-term operating costs. The company invested $1.4 billion in research and development in 2017, representing 5.3% of sales. That dedication to continuous product innovation is why in 2016 the U.S. patent board declared Deere to be the leading innovator in its industry.

For instance, Deere invests very heavily into making its products the most reliable and dependable offerings in the market, reducing customers' long-term operating costs. The company invested $1.4 billion in research and development in 2017, representing 5.3% of sales. That dedication to continuous product innovation is why in 2016 the U.S. patent board declared Deere to be the leading innovator in its industry.

Deere has also spent nearly 200 years building out the industry's largest distributor networks (2,400 distributors, including over 1,500 in the U.S. alone), which rivals don't have the time or money to recreate. And thanks to its strong brands and patent protection, Deere's tractors are some of the most trusted by farmers, who are usually loathe to take a risk on a cheaper but untested rival.

In fact, there are many farms in this country where only Deere machinery has been used for generations. This kind of brand loyalty (77% of Deere customers describe themselves as loyal to the company) allows for strong pricing power, even during industry downturns which can be long-lasting and severe. For instance, in 2016 industry wide sales plunged about 17%, yet Deere was able to raise its prices 2%, more than offsetting inflation.

In fact, there are many farms in this country where only Deere machinery has been used for generations. This kind of brand loyalty (77% of Deere customers describe themselves as loyal to the company) allows for strong pricing power, even during industry downturns which can be long-lasting and severe. For instance, in 2016 industry wide sales plunged about 17%, yet Deere was able to raise its prices 2%, more than offsetting inflation.

Deere's distributor network is also a key component to its aftermarket service part business which accounts for about 20% of its product sales and a far greater share of profits. Aftermarket parts used to maintain the firm's pricey machinery (tractors can cost well over $1 million for high end models) and minimize costly downtime represent relatively recurring and stable cash flow for the company; unlike cyclical new equipment sales, these are non-discretionary purchases.

Over the past few years aftermarket sales have been growing at about 3% annually, and since this part of the business earns much higher margins than original equipment sales, it contributes substantially to Deere's bottom line.

Over the past few years aftermarket sales have been growing at about 3% annually, and since this part of the business earns much higher margins than original equipment sales, it contributes substantially to Deere's bottom line.

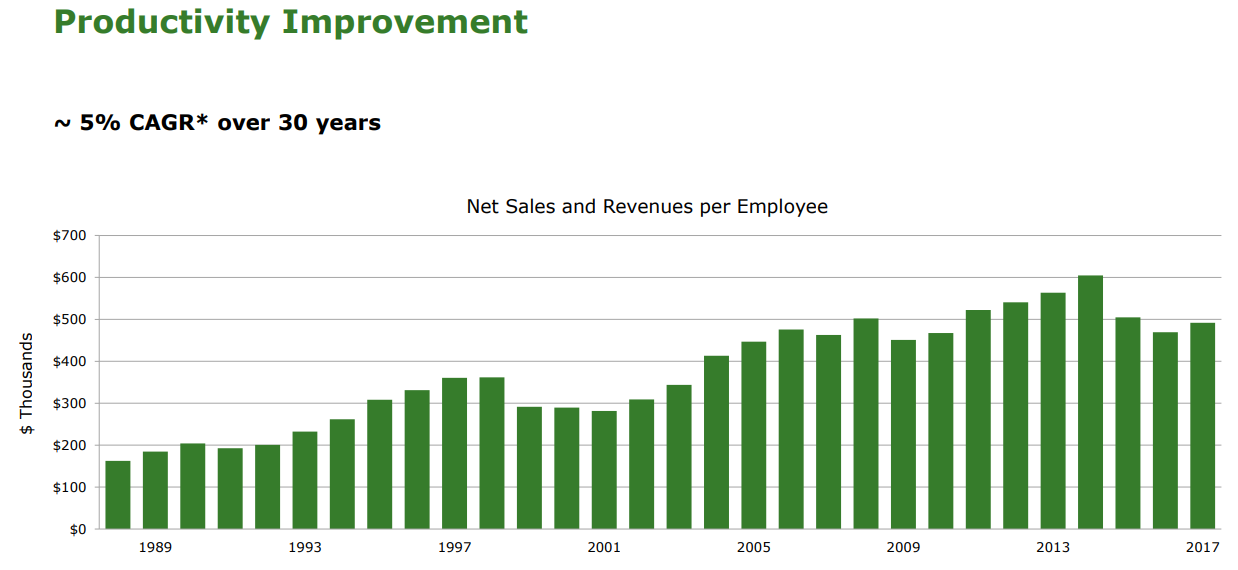

Another significant advantage Deere has is its economies of scale, which make it increasingly productive as the business expands over time. As you can see, the company is able to usually grow its long-term sales per employee at a good clip, including 5% annually over the past 30 years.

That, in turn, allows Deere to spread out its high fixed costs (such as dozens of factories all over the world) and achieve superior margins. Those margins are further boosted by being able to source the lowest possible inputs (bought in bulk) from all over the world thanks to its globe-spanning supply chain.

Thanks to its strong pricing power and good economies of scale Deere enjoys above average profitability with an operating margin around 15%, more than double the industry average.

Deere's disciplined and conservative management team is another competitive strength that has kept the company lean and highly profitable over the years. The team is led by CEO Sam Allen, who has been with the company more than 40 years, his entire working career.

Allen continues a trend of the company's in which executives have decades-long tenures at Deere, and are thus steeped in its corporate culture and maintain excellent industry operational expertise. In fact, the Roman Catholic Church has had more popes than Deere has had CEOs since its founding.

Allen continues a trend of the company's in which executives have decades-long tenures at Deere, and are thus steeped in its corporate culture and maintain excellent industry operational expertise. In fact, the Roman Catholic Church has had more popes than Deere has had CEOs since its founding.

Management's dividend policy is also conservative, targeting a payout of 25% to 33% of mid-cycle (smoothed out long-term) EPS. Excess cash flow is distributed through share buybacks (35% share count reduction since 2004). Deere's plan is meant to keep its dividend safe throughout the industry's unpredictable demand cycles.

On that note, Deere also maintains a very strong balance sheet. The company's debt levels look high at first glance due to the more than $30 billion in lease and product financing loans on the books at Deere Financing. However, that debt is all backed by Deere's equipment, making it less risky in nature.

At the corporate level, Deere's leverage metrics are very healthy, earning the company an "A" credit rating from Standard & Poor's. Thanks to the firm's low borrowing costs and solid financial flexibility, Deere can also grow its business through strategic acquisitions.

On that note, Deere also maintains a very strong balance sheet. The company's debt levels look high at first glance due to the more than $30 billion in lease and product financing loans on the books at Deere Financing. However, that debt is all backed by Deere's equipment, making it less risky in nature.

At the corporate level, Deere's leverage metrics are very healthy, earning the company an "A" credit rating from Standard & Poor's. Thanks to the firm's low borrowing costs and solid financial flexibility, Deere can also grow its business through strategic acquisitions.

In December 2017, Deere purchased privately-owned Wirtgen Group Holdings for $5.3 billion. Wirtgen is the largest road construction equipment manufacturer in the world. The company has 10 factories, employs 8,200 workers, and sells in over 100 countries, which means that buying it will provide Deere with greater economies of scale in its construction segment. This single acquisition is expected to boost Deere's 2018 sales by $3.1 billion, or about 12%.

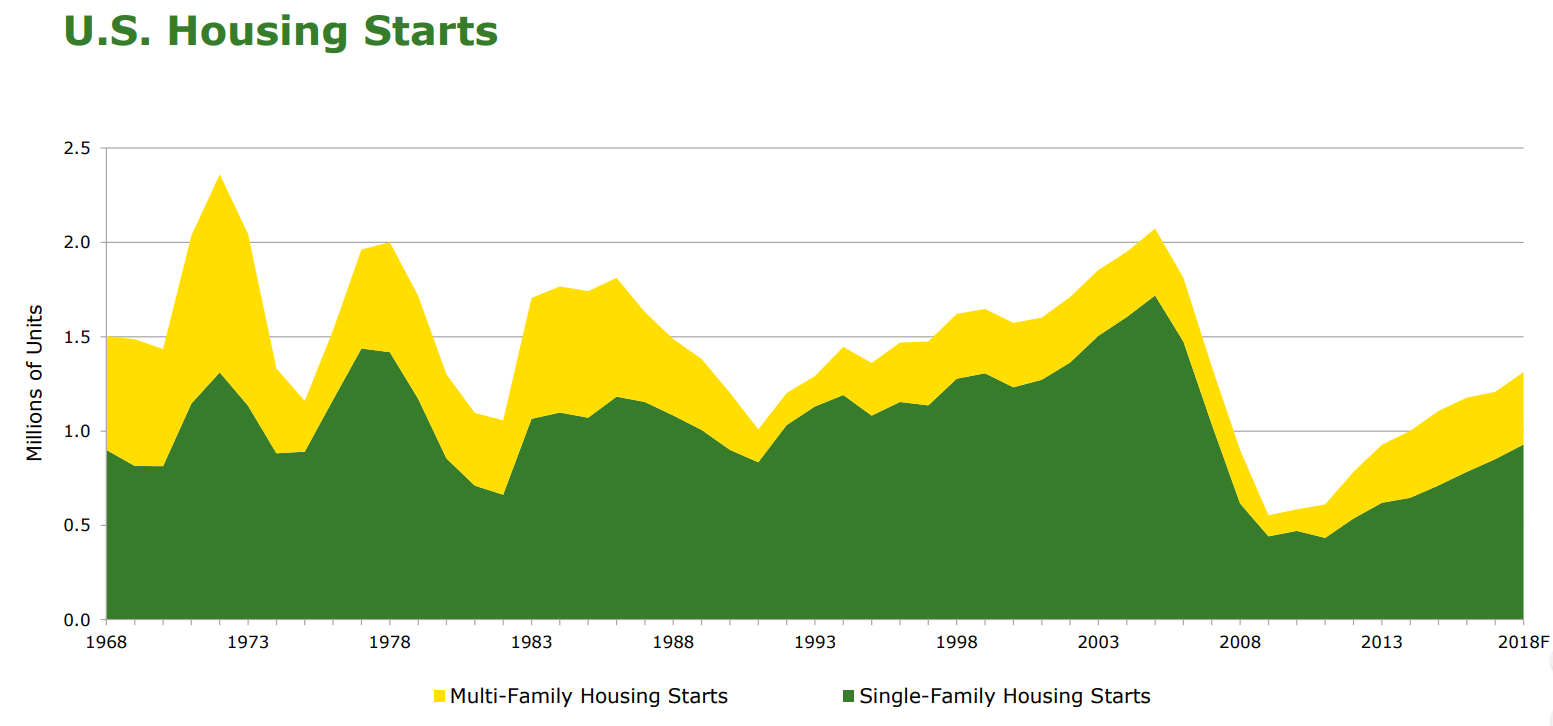

The reason that Deere is investing into non-farm-based businesses is to help diversify its cash flow from a heavy reliance on just one industry (U.S. agriculture). Management also wants to take advantage of an improving U.S. housing market.

However, Deere's core business remains tied to agriculture for the foreseeable future. Fortunately, there is a strong long-term growth driver that should push Deere's global tractor and farm product sales higher over time. Specifically, between today and 2050 it's expected that the world's population will rise from 7.6 billion to 9.8 billion people.

What's more, emerging market economies (where nearly all the population growth is coming from) are expected to grow strongly, fueling a rise in the middle classes of countries like China and India. That, in turn, is expected to result in more Western-style (heavier meat consumption) diets. As a result, total agricultural output will need to roughly double over the next 30 years to feed a hungrier world.

Deere has been seeing success in building its position in emerging countries like Brazil, where its current market share is 20%, up from just 8% a decade ago. For context, in the U.S. Deere has about 36% market share, making it the No. 1 agricultural machinery provider. In Europe and most emerging markets (like Latin America), Deere is the No. 2 provider.

Meanwhile, construction spending is expected to remain robust as the percentage of people living in cities continues to rise. This large-scale urbanization will require substantial investments into new housing (homes and apartments), as well as infrastructure, which should drive good demand growth for companies like Deere.

That being said, due to its large size and servicing of highly cyclical industries, Deere seems unlikely to grow its earnings per share by more than a low to mid-single-digit pace. Combined with its track record of highly variable dividend growth rates (more on this in a moment), Deere might not be the best long-term income growth stock for many investors.

In fact, there are several major risk factors that investors need to consider before investing in this company.

Key Risks

Deere operates in highly cyclical industries whose sales are driven by the health of the economy, as well as volatile commodity prices.

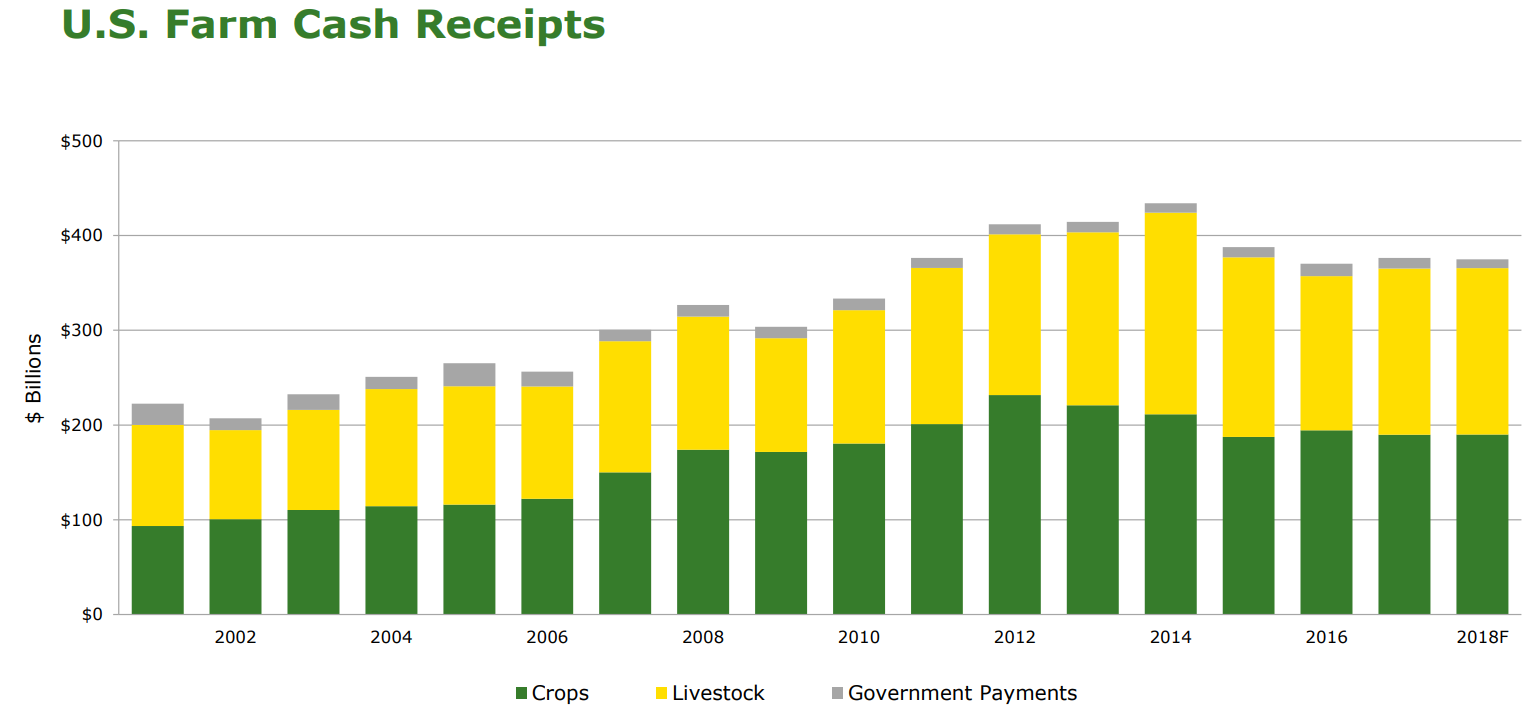

For example, between 2008 and 2009 the Great Recession caused overall North American tractor sales to decline by 22%. Then, due to years of low agricultural prices, it was not until 2015 that tractor sales finally recovered to their previous highs.

The industry's most recent recession happened because low agricultural prices caused U.S. farm revenues to peak in 2014. Such industry conditions can lead to extreme swings in operating margins, due to Deere's relatively high fixed costs. For example, between 2013 and 2016 the company's operating margin fell from 14.5% to 8%.

The industry's most recent recession happened because low agricultural prices caused U.S. farm revenues to peak in 2014. Such industry conditions can lead to extreme swings in operating margins, due to Deere's relatively high fixed costs. For example, between 2013 and 2016 the company's operating margin fell from 14.5% to 8%.

Crop revenues have yet to recover, which means that Deere's growth in demand is largely a result of farmers having to replace worn out equipment. This potentially limits the company's future growth opportunities in the U.S., making its foray into international markets that much more important.

However, increased focus on overseas sales will expose it to growing currency risk. Already over 40% of revenue comes from international markets, and Deere's largest growth potential is in emerging markets such as China, India, and Brazil.

When the U.S. dollar appreciates against local currencies in these countries, this can result in positive local sales growth translating to negative sales and earnings growth when earnings are reported. The good news is that most of the time currency fluctuations are not nearly that severe, but they can nonetheless represent significant short- to medium-term growth headwinds.

When the U.S. dollar appreciates against local currencies in these countries, this can result in positive local sales growth translating to negative sales and earnings growth when earnings are reported. The good news is that most of the time currency fluctuations are not nearly that severe, but they can nonetheless represent significant short- to medium-term growth headwinds.

Another potential risk is rising input costs such as in raw materials like: steel, plastics, and electronics. U.S. steel tariffs have caused the price of US hot roll steel to spike, which will pressure the company's margins.

On a related note, the multi-front trade battles the U.S. is currently engaged in are another potential threat to Deere's short-term results. Most of Deere's business is tied to U.S. agriculture, and foreign retaliatory tariffs (especially from China) have been extremely aggressively focused against U.S. farm exports like soybeans.

In fact, Chinese exports account for 25% of U.S. soybean production, which means that if the U.S. trade battles escalate and drag on for too long, Deere could see its projected sales growth slow or even turn negative. At the same time as rising input prices are causing its margins to fall.

On a related note, the multi-front trade battles the U.S. is currently engaged in are another potential threat to Deere's short-term results. Most of Deere's business is tied to U.S. agriculture, and foreign retaliatory tariffs (especially from China) have been extremely aggressively focused against U.S. farm exports like soybeans.

In fact, Chinese exports account for 25% of U.S. soybean production, which means that if the U.S. trade battles escalate and drag on for too long, Deere could see its projected sales growth slow or even turn negative. At the same time as rising input prices are causing its margins to fall.

Finally, its worth repeating that the company's long-term growth strategy includes strategic acquisitions, like Wirtgen Group. Acquisitions always bring execution risk, potential integration challenges, and the risk of overpaying.

And while the company's corporate leverage is low, Deere's overall large debt levels could still pose a threat to it. While its financing arm's loans are profitable and backed by income-producing assets, if its customers get into trouble and default (another downturn in farming), then Deere could be facing large losses due to its high effective financial leverage (like a bank's).

Today the company's loan loss reserves are 0.5% of its financing segment's book, indicating very little expected defaults. However, in another recession or agricultural downturn, those losses could mount quickly. This could lead to very disappointing dividend growth in the future, or even potentially a payout cut if conditions were bad enough.

For example, while Deere hasn't cut its dividend in over 20 years, there have been very long stretches of the dividend being frozen (such as 2014 through 2017).

And in the Farm crisis of the 1980's Deere did have to cut the dividend, severely. From 1981 to 1983, Deere's payout was reduced 62%. Then, after a brief recovery in 1984 and 1985, the dividend was cut 75% in 1986, again due to extremely challenging conditions in U.S. agriculture leading to huge credit losses.

While the dividend recovered to its 1981 levels by 1989, it then was frozen for five years. From 1997 to 2004, Deere froze its dividend yet again. This is why, despite occasionally boosting the payout by a large amount (15% in 2018), Deere's overall dividend growth rate is far less impressive (6% average over the past five years).

Today the company's loan loss reserves are 0.5% of its financing segment's book, indicating very little expected defaults. However, in another recession or agricultural downturn, those losses could mount quickly. This could lead to very disappointing dividend growth in the future, or even potentially a payout cut if conditions were bad enough.

For example, while Deere hasn't cut its dividend in over 20 years, there have been very long stretches of the dividend being frozen (such as 2014 through 2017).

And in the Farm crisis of the 1980's Deere did have to cut the dividend, severely. From 1981 to 1983, Deere's payout was reduced 62%. Then, after a brief recovery in 1984 and 1985, the dividend was cut 75% in 1986, again due to extremely challenging conditions in U.S. agriculture leading to huge credit losses.

While the dividend recovered to its 1981 levels by 1989, it then was frozen for five years. From 1997 to 2004, Deere froze its dividend yet again. This is why, despite occasionally boosting the payout by a large amount (15% in 2018), Deere's overall dividend growth rate is far less impressive (6% average over the past five years).

Simply put, Deere's dividend is likely safe for the foreseeable future. However, the company's poor track record of infrequent but severe cuts, and long stretches with zero growth, mean that investors looking for exposure to U.S. agriculture may be better off looking elsewhere.

Closing Thoughts on Deere & Company

Deere's track record over the past nearly two centuries has been impressive. The firm has established itself as one of the most trusted and largest farm equipment makers in the world. And over the decades it's successfully diversified into construction and forestry equipment.

The company's long-term plans to continue diversifying into faster-growing emerging markets and relatively more stable industries (construction and forestry) should help decrease future cash flow variability (though not eliminate it entirely).

That being said, Deere has several challenges ahead of it including high exposure to potential credit losses (from its financing segment), and ongoing challenges with generating steady enough free cash flow to fund consistent dividend growth.

That being said, Deere has several challenges ahead of it including high exposure to potential credit losses (from its financing segment), and ongoing challenges with generating steady enough free cash flow to fund consistent dividend growth.

Ultimately there seem to be better names to own in both the agricultural industry, as well as the industrial sector. These include companies with: strong balance sheets, less cyclical end markets, and a more proven ability to grow their dividends each year in all manner of economic and industry conditions.