AT&T Can Sustain Dividend But Delayed Deleveraging Reduces Margin for Error

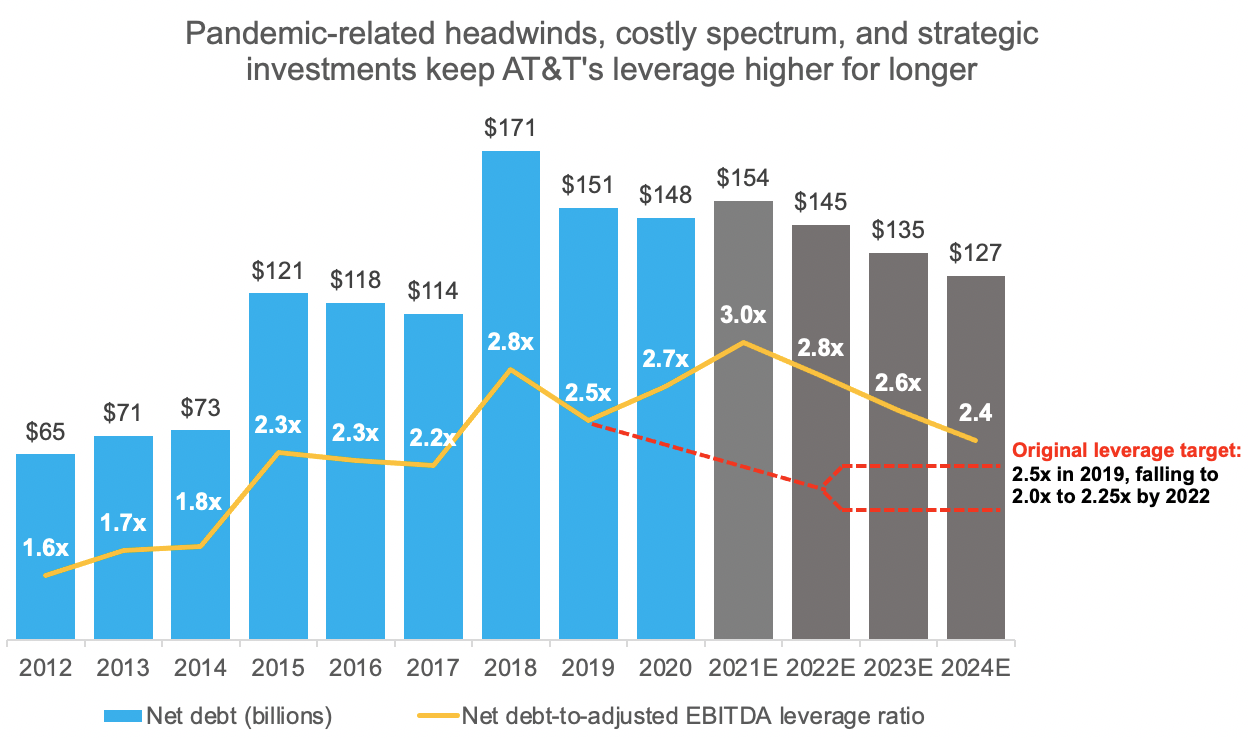

AT&T purchased $27.4 billion of spectrum at the Federal Communications Commission's recent record-setting auction and plans to reduce its leverage ratio to 2.5x in 2024, according to the firm's March 12 business update.

Both of these figures missed our expectations. In the analysis we shared in February, we assumed AT&T would spend $20 billion at the spectrum auction and see its leverage ratio fall below 2.3x in 2023 (and even lower in 2024).

We said we would consider downgrading AT&T's Dividend Safety Score if its spectrum costs were greater than we anticipated and management showed a willingness to run the business with higher leverage in the short term.

With both of those factors materializing and reducing the company's margin for error, we are lowering AT&T's Dividend Safety Score from Safe to Borderline Safe.

We plan to continue holding our AT&T shares, which account for about 1.4% of our Conservative Retirees portfolio.

Assuming everything goes according to management's plan, we still expect AT&T to maintain its dividend at its current level. Valuation expectations also continue to look modest for the stock.

But AT&T's higher leverage needs to be watched closely in the coming years.

To provide more context around AT&T's balance sheet, we updated our leverage analysis below to incorporate the firm's latest guidance and DirecTV divestiture.

Management in 2019 had expected leverage to fall from 2.5x to below 2.25x by 2022. But AT&T's leverage ratio is now projected to rise to 3.0x in 2021, matching its mid-2018 level when the firm completed the acquisition of Time Warner.

Leverage is then expected to decline only moderately over the next few years, driven by a mix of earnings growth and debt reduction using free cash flow available after paying dividends.

Source: Simply Safe Dividends, Company Filings

AT&T's debt-funded spectrum costs have slowed its deleveraging progress, but the firm's free cash flow is also tracking around 15% to 20% below where management thought it would be just 18 months ago.

The pandemic is partly to blame for the shortfall as WarnerMedia's (17% of EBITDA) theatrical releases faced delays and its cable networks' ad revenue declined.

But AT&T has also felt pressure to invest more in its internal infrastructure and across its strategic business areas of 5G wireless, fiber internet, and streaming.

While the dividend remains well covered by free cash flow with a payout ratio near 60%, the concern is that AT&T may need to put even more money towards these capital-intensive areas to protect its long-term outlook.

For example, AT&T in 2020 invested $2.1 billion in its streaming service HBO Max. The company expects to ramp spending on this product in the years ahead, with ambitions to roughly double its number of HBO and HBO Max subscribers by 2025.

Depending on how much spending is ultimately needed, this could eat into the $11 billion of free cash flow currently retained by the company after paying dividends, and HBO Max is not expected to break even until 2025.

S&P earlier this month revised its outlook on AT&T's BBB credit rating to negative from stable, citing concerns that leverage could remain above their base-case forecast as management juggles these competing capital allocation priorities.

"AT&T's business strategy is focused on acquiring spectrum, deploying fiber, and investing in its streaming product HBO Max. However, balancing shareholder returns, including its sizable dividend, with business investment and debt reduction will be challenging, in our view."

– S&P Global Ratings

Favorable debt market conditions have taken some of the pressure off of AT&T's balance sheet by reducing refinancing risk and keeping borrowing costs low.

However, until AT&T demonstrates that its current slate of investments is sufficient to return the business to profitable growth and support material deleveraging progress, we are unlikely to upgrade the company's Dividend Safety Score.

Overall, we think management's commitment "to sustaining the dividend at the current levels" has enough fundamental support for now. AT&T's higher leverage just raises the stakes in case the firm hits any unexpected road bumps along the way.

As we stated in February, management has a long ways to go to regain credibility with investors following the firm's ill-timed and costly expansions into pay-TV and media.

This year will be a big step as the firm positions itself for a return to growth in 2022 and tries to demonstrate that it can effectively manage its sprawling operations.

Should there be any significant setbacks to management's long-term plan, there's a chance that the firm would revisit its capital allocation priorities in light of AT&T's debt load and weak valuation.

As always, we will continue monitoring AT&T's progress and provide updates as needed.