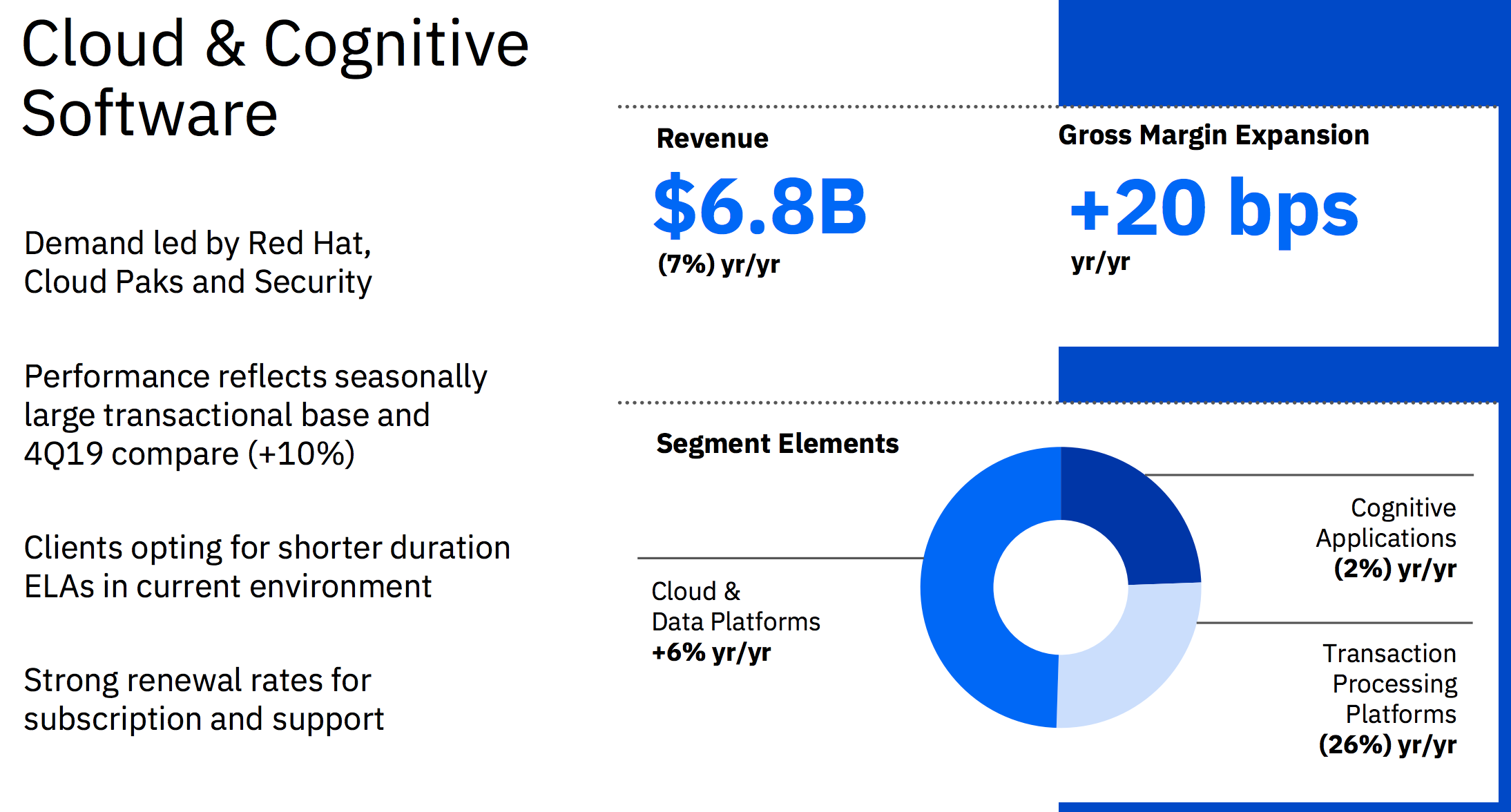

IBM's organic sales fell 8%, marking the fourth straight quarterly decline, but investors were most concerned by a 7% drop in the Cloud & Cognitive Software segment.

This high-margin division accounts for roughly 50% of IBM's gross profit and will become an even larger driver once the firm spins off its infrastructure services segment (25% of revenue) in late 2021.

Cloud & Cognitive Software holds the foundational pieces of IBM's hybrid cloud and artificial intelligence (AI) strategy, which new CEO Arvind Krishna has bet the company's future on.

Cloud & Cognitive Software's disappointing results could signal that Mr. Krishna's turnaround plans are not delivering quickly enough for post-spin IBM to hit its goal of mid single-digit revenue growth in 2022.

Management attributed most of the weakness to factors outside of the company's control.

Specifically, IBM's Transaction Processing Platforms subsegment (about 25% of the Cloud & Cognitive Software segment) recorded a 26% revenue decline.

This business sells transaction processing and storage software to clients in industries such as banking, airlines, and retail. These software deals are usually large in size and tend to cluster in the fourth quarter.

Many of these clients continue to deal with the effects of the pandemic and have taken a more cautious approach with their spending. This put downward pressure on large software transactions, according to management.

IBM also pointed out that software growth in the fourth quarter of 2019 was unusually strong with many large deals renewing. That product cycle dynamic made 2020's results look worse on a year-over-year basis.

There's probably some truth to those claims. But IBM's poor credibility and disappointing revenue performance has more investors wondering if the company's cloud software offerings may just not be as competitive as management believes.

Yet IBM's Cloud and Data Platforms subsegment (about half of the Cloud & Cognitive Software segment) registered just 6% growth last quarter. And the firm's Cognitive Applications platform, which includes software infused with AI, fell by 2%.

Red Hat's performance at least remained strong with 17% organic sales growth, but we estimate this business will only account for around 10% of post-spin IBM's revenue.

Source: IBM Earnings Presentation

It feels a little harsh to place judgement on Mr. Krishna's turnaround results this early in his tenure (he took the top job in April 2020 at the onset of a pandemic), but IBM hasn't exactly earned the benefit of the doubt either.

Despite the disappointing finish to 2020, management still hopes to deliver revenue growth this year as client demand improves in the second half of 2021.

From a financial perspective, IBM remains in good shape for now and expects to continue supporting a "secure and modestly growing dividend policy."

The company generated $6.1 billion in free cash flow last quarter. This was plenty to cover IBM's $1.5 billion of dividend payments (a 25% payout ratio) while also providing some cash for debt reduction.

Cash flow is expected to remain supportive of the dividend and continued deleveraging. Management provided guidance for adjusted free cash flow to rise from $10.8 billion in 2020 to $11 billion to $12 billion this year and $12 billion to $13 billion in 2022.

Even after accounting for IBM's $2.5 billion of expected restructuring charges related to its spin-off, the $6 billion dividend should remain comfortably covered if those results are realized.

However, income investors should remember that IBM's spin-off transaction taking place in late 2021 will result in IBM's dividend being split between the two companies. See our note here for more information.

Overall, IBM's latest set of results didn't do much to change our opinion of the company.

IBM hasn't shown investors many reasons why it can be a serious cloud competitor, but it may take a few years to assess the success of Mr. Arvind's hybrid cloud strategy.

For now, IBM continues to have the financial health to pay a reliable dividend and work on its turnaround plan. But the company cannot sustain revenue losses forever.

The stock's expectations look low (as usual), but there are no guarantees IBM will successfully adapt its business in the long term, especially if rivals move even further ahead of IBM as cloud demand accelerates.

We will continue monitoring IBM's traction over the coming quarters and provide updates as needed. Given IBM's track record, the stock will probably remain a "show me" story until revenue trends improve.