Chevron's Breakeven Oil Price Now in the $40s, Providing More Support for the Dividend

Chevron on Friday reported fourth-quarter earnings and showed continued progress improving the sustainability of its dividend in a low oil price environment.

Driven by capital spending reductions and lower operating expenses, Chevron's breakeven oil price required to cover its capital program and dividend was under $50 per barrel for the second quarter in a row. That's down from $55 per barrel in 2019 and the $80s not long before that.

Chevron's breakeven price is especially impressive since it includes the poor performance of its downstream and chemicals businesses, which normally account for around 20% of firm-wide profits.

These cyclical divisions barely broke even last year since they are experiencing very low margins and weak volumes compared to their historical norms. Assuming they eventually recover to pre-pandemic profit levels, Chevron's breakeven price will fall even further.

Brent oil sits near $55 per barrel today, so Chevron's dividend is expected to be more than covered by free cash flow in this environment.

However, management opted to keep the dividend frozen for the first quarter of 2021 since they "expect only a gradual recovery in the global economy, which would support gradual recovery in commodity prices."

Chevron held its dividend flat for 10 consecutive quarters during the 2014-16 oil crash, so management's conservatism is nothing new when faced with an uncertain commodity price environment.

Based on management's comments during the earnings call, we believe Chevron will consider a low single-digit dividend increase by the end of this year if the price of oil holds near its current level.

The company's balance sheet remains supportive of the dividend as well. Thanks in part to its less ambitious growth plans, Chevron entered the latest downturn in oil prices with one of the lowest net debt to capital ratios in the industry.

This metric ticked up from 13% in 2019 to 23% last year, reflecting a moderate amount of borrowing to fund the dividend and the firm's opportunistic acquisition of Noble Energy.

Despite this increase, Chevron's leverage sits comfortably in the middle of management's 20% to 25% preferred range and remains on the low end compared to its peers.

Unlike many of its rivals, Chevron does not need to repair its balance sheet. The firm has flexibility to ride out this down cycle and invest capital opportunistically depending on how the industry landscape evolves this year.

For example, Chevron could look to restart production in the Permian Basin or pursue another acquisition. But even without any further actions, Chevron expects its 2021 production to be flat to up 3% despite additional reductions in spending levels.

Despite these strengths and a track record of paying uninterrupted dividends since 1912, Chevron hasn't received much love from investors.

The oil and gas industry has earned unsatisfactory returns over the past decade while racking up dangerous amounts of debt. And the long-term outlook for fossil fuels has become fuzzier with pressure mounting to transition the world to a cleaner energy mix.

The U.S. represents only about a third of Chevron's upstream production, with the Permian Basin accounting for more than half of the firm's domestic exposure. Fortunately, federal acreage represents less than 10% of Chevron's land in this important area.

Perhaps the bigger uncertainty is whether oil prices can hold at their current level above $50 per barrel as U.S. shale producers mull whether to increase their production growth.

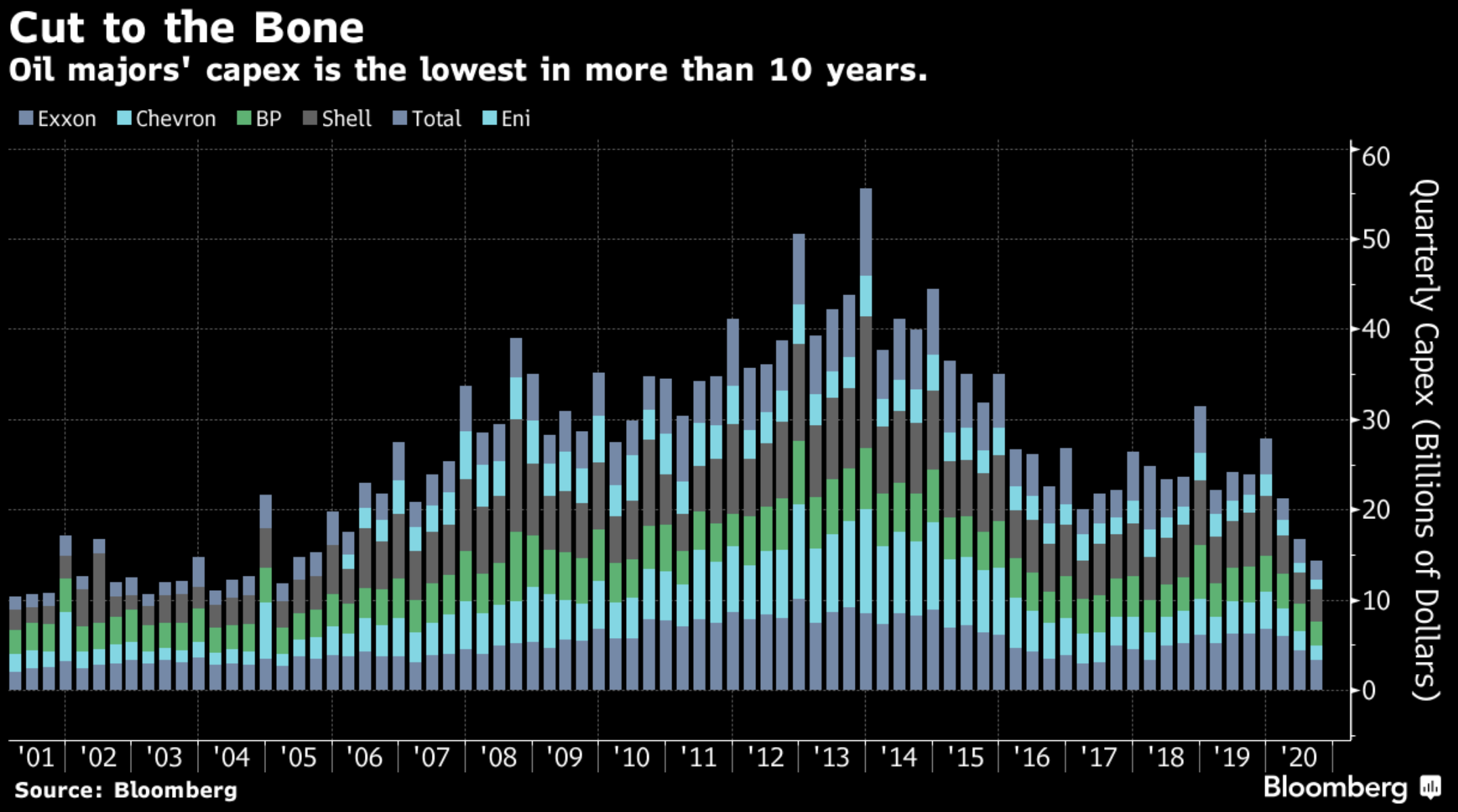

The six oil supermajors saw their combined capital expenditures fall by about 50% in the third quarter of 2020. This marked the lowest level since 2005, according to data compiled by Bloomberg.

Source: Bloomberg

Even if energy demand remains flat, this could create supply problems since oil production declines over the life of a well as the deposit it taps is depleted. New investment is continuously required just to maintain production rates.

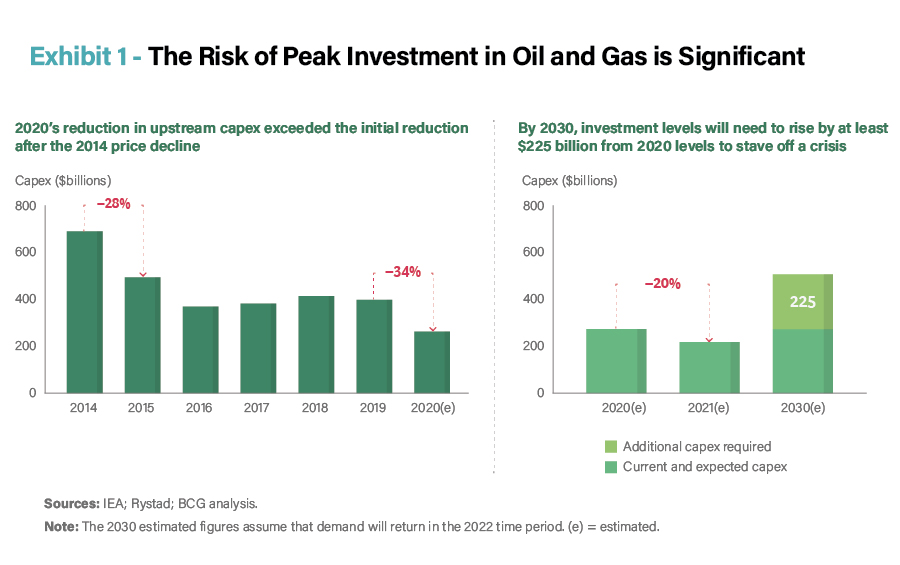

The International Energy Forum, in partnership with the Boston Consulting Group, believes that industry investment needs to rise over the next three years by at least 25% yearly from 2020 levels to stave off a supply crisis and keep the market balanced.

Yet investment levels are expected to fall another 20% in 2021 based on the range of company announcements made at the time the report was published in December.

Source: International Energy Forum Report

We believe that fossil fuels will remain a core component of the world's energy mix, and the industry's massive reduction in capital spending could persist as investors push drillers to earn higher returns on their investments, deleverage their balance sheets, and take actions to advance a lower carbon future.

The largest, lowest-cost producers seem best positioned to navigate this uncertain environment and capitalize on the industry's potential underinvestment in oil production.

With a shared interest in cutting costs, improving operational efficiencies, and staying focused on fossil fuels, Chevron and Exxon even discussed merging last year after the pandemic set in, according to sources cited by The Wall Street Journal.

Talks were "described as preliminary and aren't ongoing but could come back in the future." However, any deal would face significant regulatory and antitrust challenges, especially under the Biden administration.

Regardless, Chevron remains well positioned to navigate the years ahead on its own. The company has prioritized earning higher returns on capital, maintaining a conservative debt level, and lowering its dividend breakeven point.

It's hard to say what the world's long-term energy mix will look like, but Chevron's modest valuation and safe dividend could appeal to contrarian income investors who believe in oil's staying power.