Exxon Expects to Maintain Dividend as Breakeven Oil Price Falls

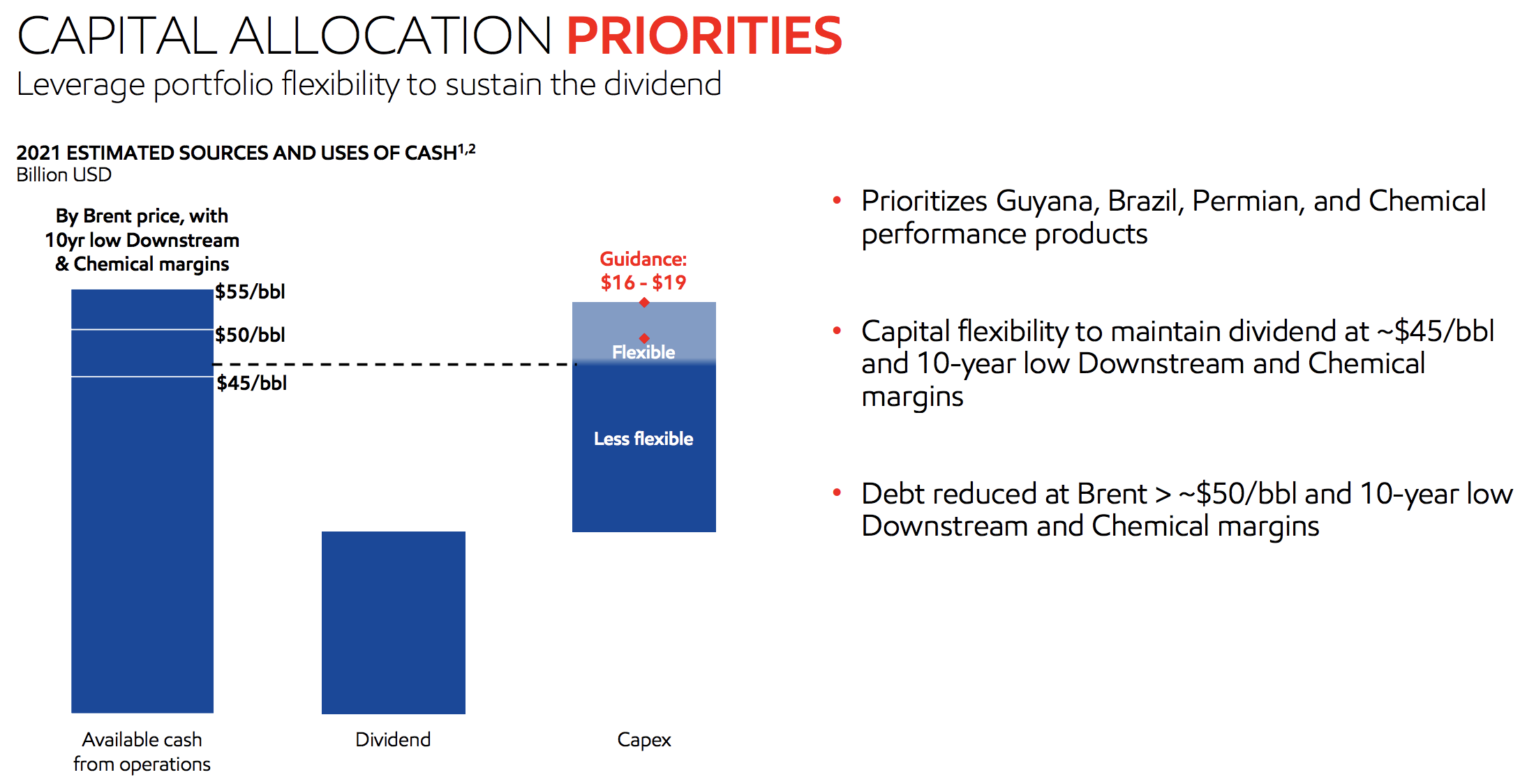

Exxon believes its cash flow will cover capital expenditures and the dividend this year even if Brent oil prices average as low as $45 per barrel and its downstream and chemical businesses maintain their lowest margins in at least a decade.

As part of the firm's earnings presentation on Tuesday, management laid out capital allocation priorities through 2025. Exxon's base plan this year expects Brent prices of $50 per barrel, but the firm highlighted its ability to flex its spending on short-cycle shale projects if market conditions change.

Management believes this will enable dividend coverage and maintenance of balance sheet strength at Brent prices of $45 per barrel (versus $58 today) while allowing the firm to continue working on its largest and most important projects.

Source: Exxon Earnings Presentation

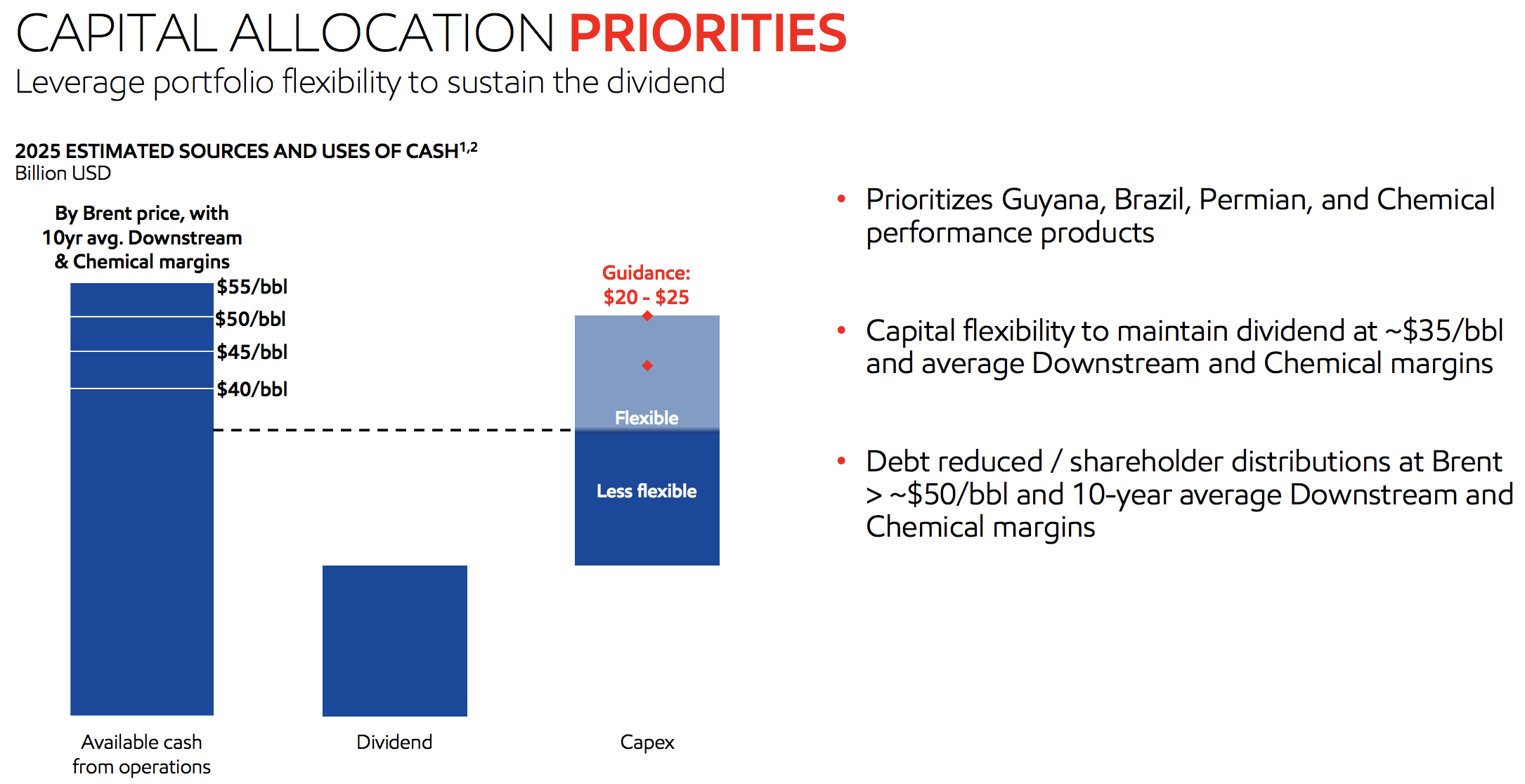

If Exxon's downstream and chemicals businesses, which historically accounted for about 50% of the firm's profits, saw their margins return to their 10-year averages, the firm's breakeven prices would be roughly $5 a barrel lower.

This would allow Exxon this year to not only fund its investments and pay the dividend, but also reduce debt at Brent prices slightly above $45 a barrel.

Less than a year ago, analysts estimated that Exxon needed oil prices to be $60 per barrel to cover its capital spending and dividend. The firm's cost reductions and capital flexibility have put Exxon in a better spot to defend its payout.

Looking further out, Exxon needs to increase its capital spending to a more sustainable level. The firm's planned capital expenditures of $16 billion to $19 billion in 2021 will be the lowest level of spending that Exxon has had in any year since Exxon and Mobil merged in 1999.

Management targets $20 billion to $25 billion of annual capital expenditures from 2022 through 2025. Roughly 90% of Exxon's upstream spending over this period has a cost-of-supply of $35 Brent per barrel or lower.

As these projects come online, they are expected to represent 40% of Exxon's operating cash flows in 2025. Coupled with ongoing cost-cutting actions, this will further reduce the firm's breakeven oil price.

Assuming downstream and chemical margins return to their 10-year averages during this period, Exxon by 2025 expects to be able to maintain its dividend and fund this higher level of investments while preserving its balance sheet at Brent prices between $45 and $50 per barrel.

The company believes it will even be able to cover the dividend and essential capital investments at Brent prices as low as $35 thanks to its ability to flex some of its capital spending.

Source: Exxon Earnings Presentation

Exxon's plans instill more confidence in the firm's dividend, but we need to see the company rebuild the strength of its balance sheet before considering upgrading its Borderline Safe Dividend Safety Score.

With Brent prices approaching $60 per barrel today, Exxon should be in a position to generate excess cash it can use for deleveraging.

However, it's hard to say if oil prices will hold at their current level as U.S. shale producers mull whether to increase their production growth. For now, there's some hope that spending reductions will support firmer prices.

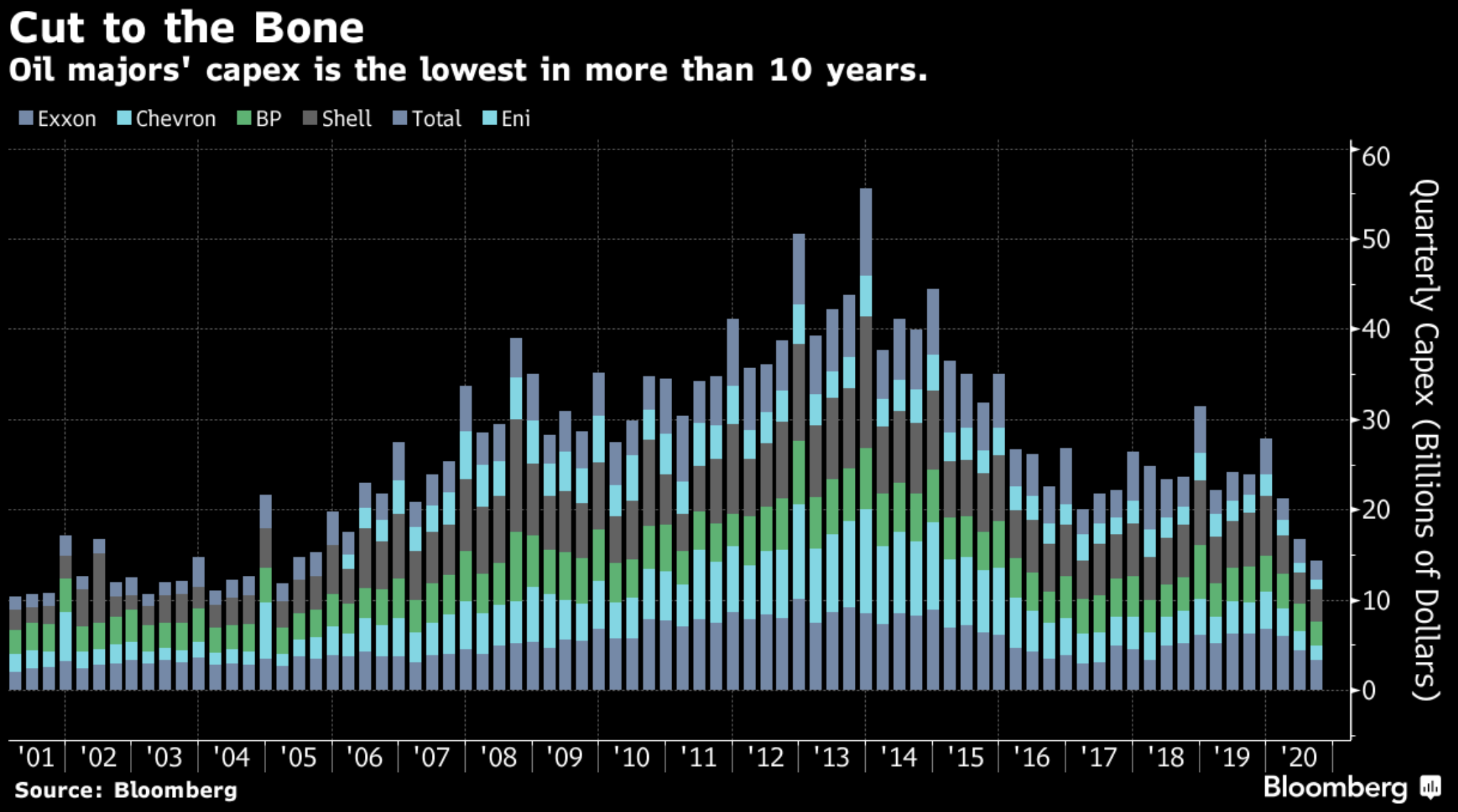

The six oil supermajors saw their combined capital expenditures fall by about 50% in the third quarter of 2020. This marked the lowest level since 2005, according to data compiled by Bloomberg.

Source: Bloomberg

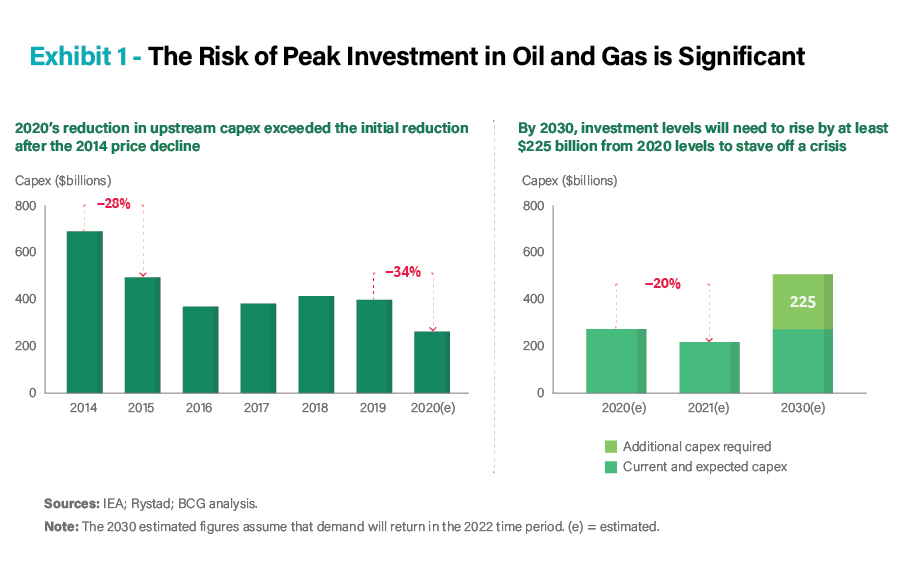

Even if energy demand remains flat, this could create supply problems since oil production declines over the life of a well as the deposit it taps is depleted. New investment is continuously required just to maintain production rates.

The International Energy Forum, in partnership with the Boston Consulting Group, believes that industry investment needs to rise over the next three years by at least 25% yearly from 2020 levels to stave off a supply crisis and keep the market balanced.

Yet investment levels are expected to fall another 20% in 2021 based on the range of company announcements made at the time the report was published in December.

Source: International Energy Forum Report

The industry's massive reduction in capital spending could persist as investors push drillers to earn higher returns on their investments, deleverage their balance sheets, and take actions to advance a lower carbon future.

The largest, lowest-cost producers seem best positioned to navigate this uncertain environment and capitalize on the industry's potential underinvestment in oil production.

With a shared interest in cutting costs, improving operational efficiencies, and staying focused on fossil fuels, Exxon and Chevron even discussed merging last year after the pandemic set in, according to sources cited by The Wall Street Journal.

Talks were "described as preliminary and aren't ongoing but could come back in the future." However, any deal would face significant regulatory and antitrust challenges, especially under the Biden administration.

Regardless, Exxon's latest plans hopefully position the company for a stronger future. But activist investors remain dissatisfied with Exxon's plans. While their desires include maintaining the dividend, they argue that the firm is not doing enough to adapt as markets move toward cleaner forms of energy.

Exxon plans to invest more than $3 billion through 2025 in technologies to reduce carbon emissions, but this will represent only around 3% of total capital expenditures as the firm remains focused on its core oil and gas businesses.

We believe that fossil fuels will remain a core component of the world's energy mix, but almost any long-term prediction admittedly comes with heightened uncertainty.

Based on what we know today, we plan to keep holding our Exxon shares to see how the future unfolds. The stock could appeal to contrarian income investors who believe in oil's staying power, and we will continue providing updates as necessary.