Owens & Minor stunned many investors in October 2018 when it announced a 71% dividend cut.

Shares fell more than 40% on the news as the medical supplies distributor broke its streak of paying uninterrupted dividends since 1977.

The company's core customers (hospitals) were putting increased price pressure on the firm in an effort to cut costs, and several large customers chose not to renew their distribution contracts.

As growth in its legacy business struggled, management attempted to stabilize earnings by making two large acquisitions in faster-growing segments, straining Owens & Minor's balance sheet and liquidity.

Cutting the dividend gave Owens & Minor more breathing room to service its significant debt load while continuing to adapt its business model for the future.

To further prioritize debt reduction, in February 2019 management slashed the dividend by another 97%, sending shares falling as much as 20%.

Owens & Minor had a Very Unsafe Dividend Safety Score prior to its dividend cuts. We even published a note two weeks before the October 2018 cut explaining why the firm's dividend looked speculative.

Since then, management has reduced the firm's cost structure, divested a non-core business, and issued equity to direct as much cash flow as possible towards debt reduction.

But Owens & Minor's fortunes didn't really turn around until mid-2020 when it became clearer that the company would benefit from the pandemic.

Owens & Minor has run its manufacturing operations at a record pace and added capacity to crank out N95 respirator masks and hospital gowns. The company has delivered nearly 11 billion units of personal protective equipment (PPE) since January, buoying its bottom line.

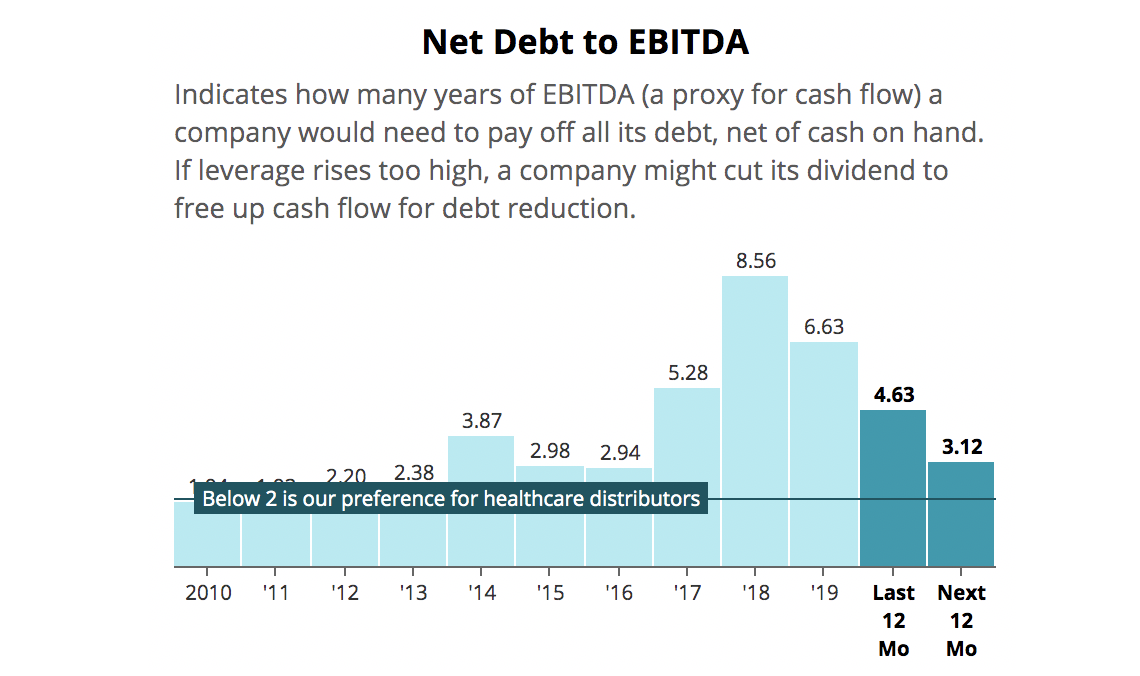

Management's previous deleveraging efforts, plus this surge in cash flow, has helped Owens & Minor reduce its debt by more than 20% over the last 6 quarters.

Owens & Minor still has a B+ junk credit rating from Standard & Poor's, but the firm has received ratings upgrades as it progresses on its deleveraging journey.

As you can see, Owens & Minor's net leverage ratio is expected to approach 3x in the year ahead, falling inside of managements 3x to 4x target range.

Source: Simply Safe Dividends

From a dividend coverage perspective, Owens & Minor's dividend costs less than $1 million per year. For context, Owens & Minor historically generated around $100 million of operating cash flow per year and is on pace to substantially exceed that figure in 2020.

Instead of suspending its dividend in 2019, Owens & Minor probably decided to keep a token payout for the sake of staying in index funds which only own stocks that pay dividends.

It's hard to say if or when Owens & Minor will pay a competitive dividend again. Management has not mentioned the dividend on a conference call since announcing the February 2019 cut.

Until the balance sheet is in better shape and management feels good about Owens & Minor's business mix, which could result in more acquisitions, the company may remain conservative with its dividend.

Regardless, Owens & Minor's strengthening balance sheet and cash flow are enough for us to raise the company's Dividend Safety Score to Borderline Safe.

Owens & Minor shares have appreciated significantly in recent months, driven by the surge in high-margin PPE sales.

With the stock trading at a more reasonable valuation and the PPE tailwind unlikely to last forever as vaccines roll out, conservative income investors may want to evaluate other companies that have less debt and stronger core businesses.