Energy Transfer Cuts Distribution by 50% to Prioritize Deleveraging

Energy Transfer is the latest midstream MLP to slash its distribution, announcing yesterday evening that it will chop its payout in half.

Management will get to explain their rationale for the distribution cut when Energy Transfer reports earnings on November 4, but this action was necessary to address the firm's fragile balance sheet.

As we discussed in July, Energy Transfer faced mounting pressure to reduce debt to protect its BBB- credit rating, which sits one notch above junk status.

With oil and gas production declining, weak commodity prices hurting shale producers, and litigation threatening the Dakota Access Pipeline, Energy Transfer's credit metrics had potential to weaken.

Meanwhile, the firm remained committed to several in-progress growth projects which prevented its cash flow from covering distributions and capital spending, restraining its ability to pay down debt.

For these reasons, Energy Transfer had an Unsafe Dividend Safety Score.

From a financial perspective, Energy Transfer's annualized distributable cash flow in the second quarter was about $5.1 billion.

The firm's previous distribution cost $3.2 billion per year, and Energy Transfer's growth capital spending is expected to total $3.4 billion in 2020.

In other words, the firm's distributable cash flow would fall short of covering Energy Transfer's total spending needs by around $1.5 billion to $2 billion.

With capital markets shunning most energy companies, midstream firms have been increasingly forced to migrate to self-funded business models, which eliminate the need to raise debt or equity capital to fund their growth.

Cutting the distribution in half will save Energy Transfer $1.6 billion annually, enough to nearly cover its expected cash flow deficit this year.

As importantly, the partnership's growth spending is expected to fall from $3.4 billion this year to $1.3 billion in 2021 and just $500 to $700 million per year in 2022 and 2023.

Coupled with some of its growth projects coming online in the next year, this will allow Energy Transfer to finally begin generating excess cash flow.

Ratings firm Standard & Poor's believes Energy Transfer's discretionary cash flow after paying distributions and covering all capital spending could approach around $2 billion in 2021 and $3 billion in 2022.

This money will be used to chip away at Energy Transfer's debt load, which exceeds $50 billion.

Despite Energy Transfer's distribution cut and improved deleveraging potential, Standard & Poor's maintained its negative outlook on the firm's BBB- credit rating.

Given the various headwinds facing the industry, Standard & Poor's does not see Energy Transfer's debt to EBITDA leverage ratio improving to management's target range of 4.0x to 4.5x (from a projected 5.5x this year) until at least the end of 2022.

Needless to say, the partnership's distribution is likely to remain frozen during this period to direct as much cash flow as possible to debt reduction.

Current unitholders face a tough decision on how to proceed.

On one hand, Energy Transfer's valuation remains depressed with units trading at around 3x distributable cash flow. It wouldn't take much to justify a higher multiple for the stock.

Signs of a sustained recovery in energy prices and domestic production would ease some of today's concerns about excess midstream infrastructure capacity.

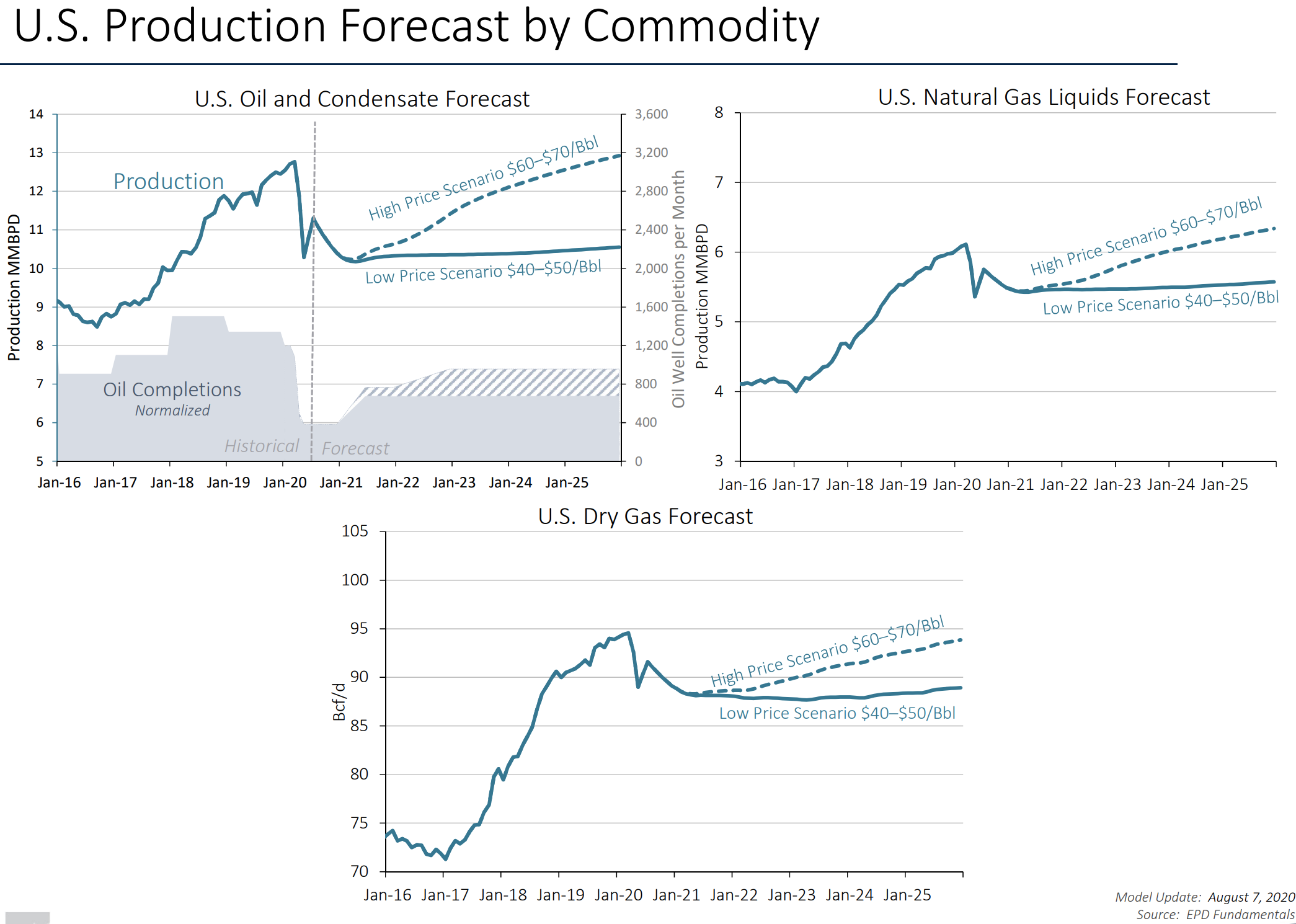

But if energy prices fail to improve much from their current level, midstream rival Enterprise Products Partners expects a minimal recovery in production.

Source: Enterprise Products Partners Investor Presentation

In a low price scenario, Energy Transfer's cash flow could decline further as pipeline throughput falls, contract rates decline, and credit risk rises (about 20% of customers already have junk credit ratings).

Energy Transfer doesn't exactly have the best reputation for executing well on its aggressive projects either, so its assets could experience greater weakness if the energy tide continues going out over the next few years.

Energy Transfer's co-founder and Executive Chairman Kelcy Warren has lost the trust of many investors as well. SL Advisors, an asset manager specializing in midstream energy infrastructure, provided a nice summary of management's past shenanigans.

Given their reputation, perhaps management would consider trying to take the firm private at a depressed valuation, locking in a loss for most retail investors.

Converting to a corporation is another option to try and improve Energy Transfer's investment appeal (and valuation), though it could trigger a taxable event.

Overall, Energy Transfer will likely remain one of the more volatile midstream stocks until its balance sheet has improved. While the stock looks cheap, there are no guarantees of a recovery.

Conservative income investors who wish to maintain exposure to the midstream space may want to consider Enterprise Products Partners, which runs its business more conservatively, has a stronger balance sheet, would also benefit from an energy recovery, and sports a similar yield near 10%.