Enterprise's Distribution Continues to Look Safe But Midstream Headwinds are Worth Monitoring

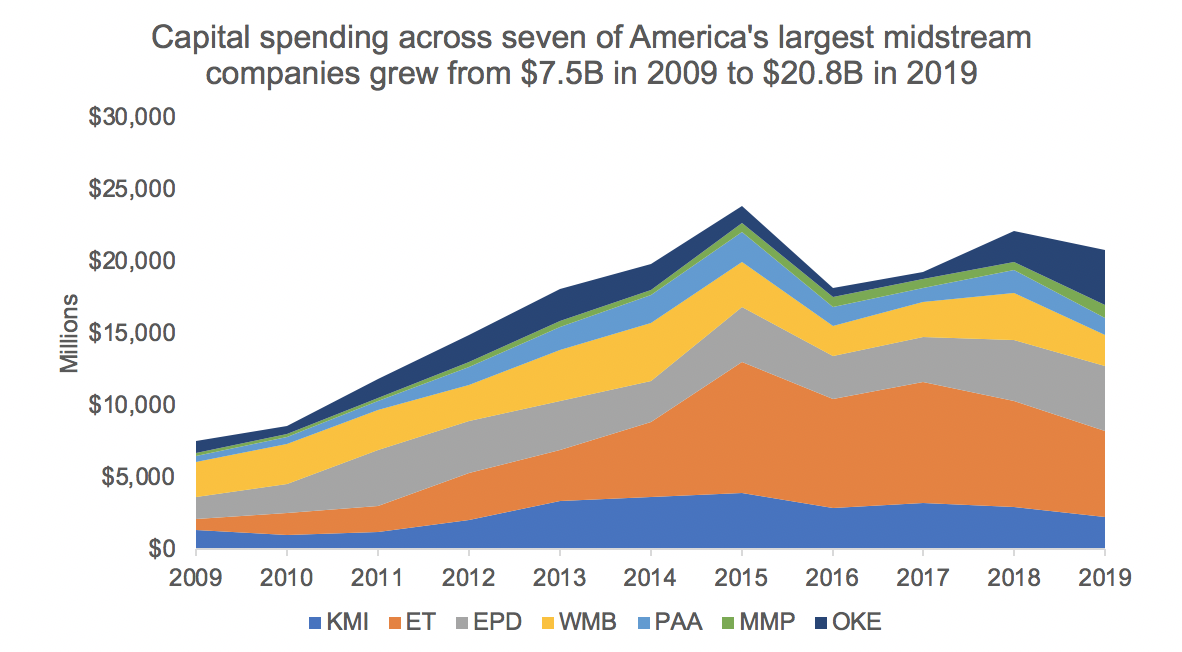

Build it and they will come. That was the midstream industry's mantra for much of the last decade as some of the largest firms combined to nearly triple their annual spending on pipelines, storage facilities, and other assets.

Source: Simply Safe Dividends, Company Filings

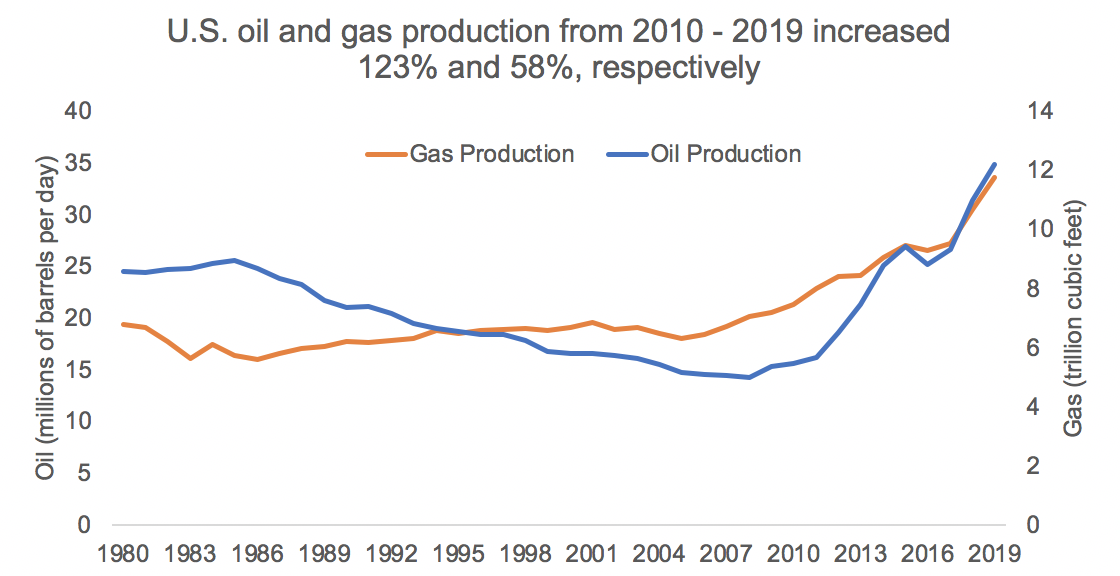

This rapid buildout of America's energy infrastructure was in response to the boom in U.S. energy production ushered in by advancements in fracking. After decades of stagnation or decline, domestic oil and gas production surged.

Source: U.S. Energy Information Administration, Simply Safe Dividends

Midstream infrastructure generally takes many years to earn a return and was put in the ground under the assumption that domestic energy production would remain strong.

But the coronavirus has upended that thesis, at least in the short term.

Government-mandated shutdowns and restrictions on travel have resulted in the largest shock to energy demand in 70 years, with a decline seven times greater than the 2009 financial crisis, per the International Energy Agency.

Energy producers have responded to today's low-price environment by slashing upstream oil and gas investment to its lowest level since 2005.

Enterprise's latest forecast shows U.S. oil production falling by around 20% from its peak, with natural gas and natural gas liquids production declining closer to 10%.

Under a high oil price scenario, a return to 2019 production levels is not expected for at least several years, while minimal recovery is projected if prices fail to improve much from their current levels.

Source: Enterprise Products Partners Investor Presentation

In the Permian Basin, which accounts for around 30% to 40% of America's oil production, pipeline utilization next year is on pace to sit near 50% as more capacity hits the market at an inopportune time.

In response to falling throughput challenges and elevated counterparty risk, pipeline operators have made headlines recently for offering customers steep discounts and providing volume incentive programs.

Some firms, including Enterprise, have also shelved certain pipeline expansion projects given the lack of demand today.

"I don't think in any way says that we are less bullish on the Permian. It's says that in the medium term, we don't need it, and [our customers] don't need it. And in the long term, who the hell knows."

– Enterprise Co-CEO Jim Teague, 9/9/20 Investor Conference

The ultimate impact from these headwinds will take time to emerge as more contracts come up for renewal, credit risk mounts across weaker energy producers, and oil demand continues its bumpy road to recovery.

Evaluating midstream companies is difficult in this environment. Differences in production basin exposures, contract terms, customer quality, backlog, and commodity and asset mixes will result in varying levels of cash flow impact across firms.

We will keep watching how these factors play out, but based on what we know today, Enterprise still looks deserving of its Safe Dividend Safety Score.

As we discussed in May, Enterprise's diversification provides some protection.

The business is connected to nearly every major U.S. shale basin, serves hundreds of mostly investment-grade customers, and touches many different commodities.

While oil production impacts production across all of Enterprise's businesses, the firm's direct exposure to crude only accounts for 25% of profits. Natural gas liquids (NGLs) make up 50% of the business, with the remainder split between dry gas and petrochemicals.

Nearly 90% of the firm's earnings are also fee-based. Only about 25% of these profits come from businesses with volumetric risk, such as gas gathering & processing and petrochemicals, which are most susceptible to swings in the market.

For now, business trends have remained stable since last quarter and should continue providing solid cash flow coverage for the distribution.

Speaking at an investor conference in early September, Enterprise said it has seen NGLs volumes continue at a similar level or a little higher compared to July. Its crude oil pipes are still running at about 80% to 85% of where they were back in March, too.

In this environment, Enterprise in the second quarter generated $1.8 billion in operating cash flow excluding changes in working capital (down 10% compared to the prior year).

On an annualized basis, Enterprise's operating cash flow would be around $7.2 billion.

Enterprise's distribution costs $3.9 billion per year, leaving about $3.3 billion available for capital spending.

Being able to cover capital expenditures (capex) without issuing equity or debt has become increasingly important across the industry with the cost of capital rising.

Fortunately, Enterprise appears well positioned to make this happen, especially after cancelling several major expansion projects last month.

Enterprise's maintenance capex totals $300 million per year, and growth capex is projected to fall from $2.8 billion in 2020 to $1.6 billion in 2021 and $0.9 billion in 2022.

In other words, as long as Enterprise's operating cash flow does not fall off a cliff compared to its second-quarter levels (analysts project distributable cash flow to decline just 6% in the year ahead), the firm has a path to soon generate over $1 billion in annual free cash flow after paying distributions.

Management said they will consider using some of this money on unit buybacks given EPD's high cash flow yield and will also evaluate distribution growth quarterly.

The firm's low leverage continues to earn Enterprise a BBB+ credit rating with a stable outlook. Leverage last quarter was 3.4x per the company's calculation, just below management's 3.5x target area.

While leverage will likely edge higher over the next year given the headwinds facing the midstream industry, we don't anticipate it reaching a dangerous level that would jeopardize Enterprise's credit rating or capital allocation plans.

However, the market continues shunning nearly all energy MLPs, including Enterprise.

Some investors worry that the world's energy transition will accelerate, causing demand for fossil fuels to fade much faster than expected.

In such a scenario, the midstream industry's remaining useful life could be a lot shorter than management teams anticipated when making their long-term investments and loading their balance sheets with debt.

If we had to guess, the world's energy mix will remain diverse for the foreseeable future, with fossil fuels remaining a core component. Please see our recent note on Exxon Mobil for more information.

Aside from the future of energy, some investors wonder what actions management might take if MLPs become an abandoned asset class, keeping valuations depressed.

The most obvious options are to take the company private or convert to a corporation, which Enterprise has previously mulled over given the potential for tax consequences and distribution reductions.

As of late July, Enterprise said it was "pretty content" with its current MLP structure. With income tax rates potentially heading higher to help with America's deficit, management said they had not spent any time looking at an MLP versus corporation analysis.

Regardless, unitholders need to be comfortable with this unique risk facing the MLP industry, as well as the long-term trajectory of demand for oil and gas.

We will keep monitoring these factors, but Enterprise's distribution should continue flowing for the foreseeable future. In fact, Enterprise on October 7 declared its next quarterly distribution, holding its payout flat.

.png)