AT&T Continues Generating Solid Cash Flow Despite the Pandemic and Remains Committed to the Dividend

AT&T reported earnings on July 23, providing a more complete look at how its expansive business is performing during this economic downturn.

For the most part, there were no big surprises.

Revenue declined by about 9% and EBITDA dipped 6%, driven by a steep pandemic-related slump at WarnerMedia.

Content production and theaters were shut down, and the lack of sports hurt advertising sales.

Pay-TV subscriber losses also remained elevated, amplified by some hotels and restaurants canceling their services.

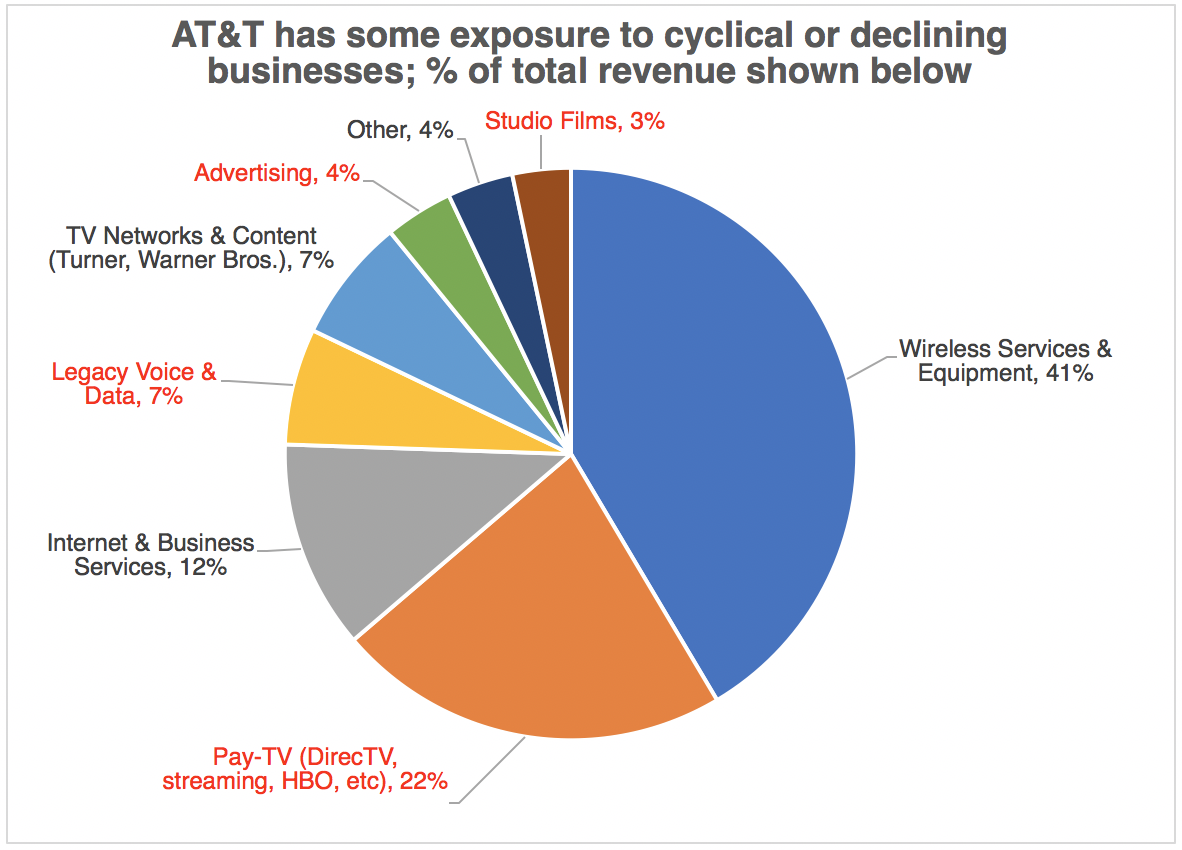

However, as we've discussed before, AT&T also has a number of less cyclical businesses.

For example, wireless services and equipment account for over 40% of the firm's revenue and have remained fairly steady.Source: Simply Safe Dividends, AT&T Data Overall, AT&T managed to generate $7.6 billion of free cash flow (down from $8.8 billion a year ago) despite the tough backdrop in some of its markets.

The firm's free cash flow payout ratio was 49% in the second quarter, and management reaffirmed guidance to deliver a full-year payout ratio near 60%.

Capital spending guidance was unchanged, so this forecast reflects management's ongoing confidence in AT&T's operating cash flow.

"We remain committed to our dividend, which we've increased for 36 consecutive years. We finished the quarter with a dividend payout ratio of about 50%. We expect to end the year with our payout ratio in the 60s, likely at the low end of that range."

– CEO John Stankey

AT&T's payout ratio guidance implies full-year free cash flow of about $23 billion to $25 billion, unchanged from management's updated view last quarter.

Prior to the pandemic, AT&T expected to generate $28 billion of free cash flow in 2020 (ramping to between $30 billion and $32 billion in 2022).

With AT&T's dividend costing about $15 billion, the cyclical headwinds facing the business continue to look manageable without jeopardizing the payout.

The main setback is that AT&T cannot pay down debt as quickly since the firm is retaining less cash flow after paying dividends than it had anticipated prior to the pandemic.

This year AT&T will likely retain around $8 billion of free cash flow that it can use to chip away at its $152 billion net debt load (including a $2.3 billion reduction this quarter).

Even if cash flow takes longer to improve than management expected due to COVID-19's lingering impact, this rate of cash flow generation is enough to cover AT&T's debt maturities in each of the next three years after management recently refinanced some debt.Source: AT&T Earnings Presentation With healthy liquidity (including $17 billion of cash on hand), various non-core assets it could sell, and continued access to capital markets on favorable terms, AT&T appears well positioned to continue riding out this downturn.

Ratings firm Standard & Poor's appears to have a similar view. On July 27, S&P reaffirmed AT&T's BBB investment-grade credit rating and stable outlook despite its expectation for EBITDA to decline by 7% to 9% this year.

That said, AT&T needs to stabilize and improve the performance of some of its businesses to ensure it can maintain a healthy pace of debt reduction, which is key to supporting the firm's Safe Dividend Safety Score.

While wireless services and high-speed internet remain low-growth cash cows and generate over half of firm-wide profits, AT&T's pay-TV business (around 20% of revenue) continues shrinking.

In the second quarter, video revenue declined 13%, driven by a loss of nearly 900,000 U.S. DirecTV subscribers as customers continued cutting the cord.

The company's satellite TV service now has 18.4 million accounts compared to over 25 million just two years ago.

AT&T is betting that HBO Max, its expanded online streaming service designed to compete with rivals such as Netflix, will help stabilize this segment over time.

HBO Max launched on May 27 but only signed up 4 million customers even as the pandemic kept people at home searching for more entertainment.

For context, rival streaming service Disney+ launched on November 12, 2019, and ended its first quarter in business with 26.5 million paid subscribers.

In fairness to AT&T, the firm has yet to ink distribution deals to make HBO Max available on popular streaming platforms Roku and Amazon Fire TV, which represent 70% of the streaming devices in the U.S.

Regardless, HBO Max represents an important bet for the company, and success won't come easy in an increasingly saturated market for streaming services.

We will continue monitoring the results of AT&T's pay-TV business and WarnerMedia division, which together represent around 30% of EBITDA.

Should the secular decline in pay-TV accelerate to unmanageable levels or WarnerMedia fail to fully rebound from the pandemic, then AT&T's reduced cash flow could make it harder to balance deleveraging, investing in its future, and returning capital to investors.

For now, AT&T's higher-margin subscription businesses and initiatives seem likely to keep generating enough cash flow to support necessary investments (nationwide 5G coverage, streaming content, etc.), dividends, and debt reduction.

We plan to maintain AT&T's Safe Dividend Safety Score and will continue holding our shares of AT&T in our Conservative Retirees portfolio.

.png)