Dominion Announces Major Divestiture Which Will Result in a Q4 Dividend Cut

On Sunday, Dominion announced plans to sell its natural gas transmission and storage business to Berkshire Hathaway in a $9.7 billion deal. This division generated nearly 25% of Dominion's operating earnings.

Driven primarily by the loss of ongoing cash flow once the sale closes later this year, Dominion expects to "rebase" (i.e. cut) its dividend by about 33% from 94 cents per quarter to 63 cents beginning with the fourth-quarter payment in December.

We had a Safe Dividend Safety Score on Dominion and own shares in our Top 20 and Conservative Retirees portfolios. Needless to say, we were surprised by this news and had not anticipated a major divestiture taking place when issuing our rating.

Given the discretionary nature of this strategic decision, I'm not sure there was much we could've done to get ahead of this cut.

Dominion's earnings were projected to increase about 5% this year per management's guidance in early May, the dividend remained covered by earnings, liquidity was solid, its investment-grade credit rating was stable, and the pandemic's impact appears limited.

Dominion's gas transmission and storage businesses also had a stable outlook compared to other midstream service providers which are under pressure from weak oil and gas prices and declining energy production.

The company's midstream operations store and transport natural gas for demand-driven counterparties such as utilities and power stations (rather than energy producers).

This business operates under long-term, take-or-pay contracts with firm reservation or capacity charges, which are largely independent of utilization. Counterparty credit quality is high, given the regulated utility skew of the customer base.

Simply put, this wasn't a problematic business, though its growth profile was on the slower side.

Dominion didn't appear to face any financing challenges for its capital spending plans either.

Demonstrating its flexibility, the firm plans to use $3 billion of the deal's proceeds to buy back its own shares. For context, the new dividend payment is about $1 billion lower than the previous payout.

Perhaps the only potential issue was that Dominion's payout ratio was a little on the high side (around 85%).

However, the payout ratio was expected to continue improving as earnings growth outpaced 2.5% annual dividend growth, a policy which management had reaffirmed in May.

Ultimately, an income investor would have had to anticipate that Dominion wanted to more immediately adjust its long-term business mix and would be comfortable losing its decades-long streak of uninterrupted dividends in the process for the right deal.

Management will speak more about their strategic rationale on a 9:00AM EDT call today, but it appears that Dominion wanted to transition its business to be more of a pure-play state-regulated utility and found a deal it couldn't pass up.

Once this transaction closes, Dominion will generate up to 90% of its operating earnings from state-regulated gas and electric utilities, up from about 70% previously.

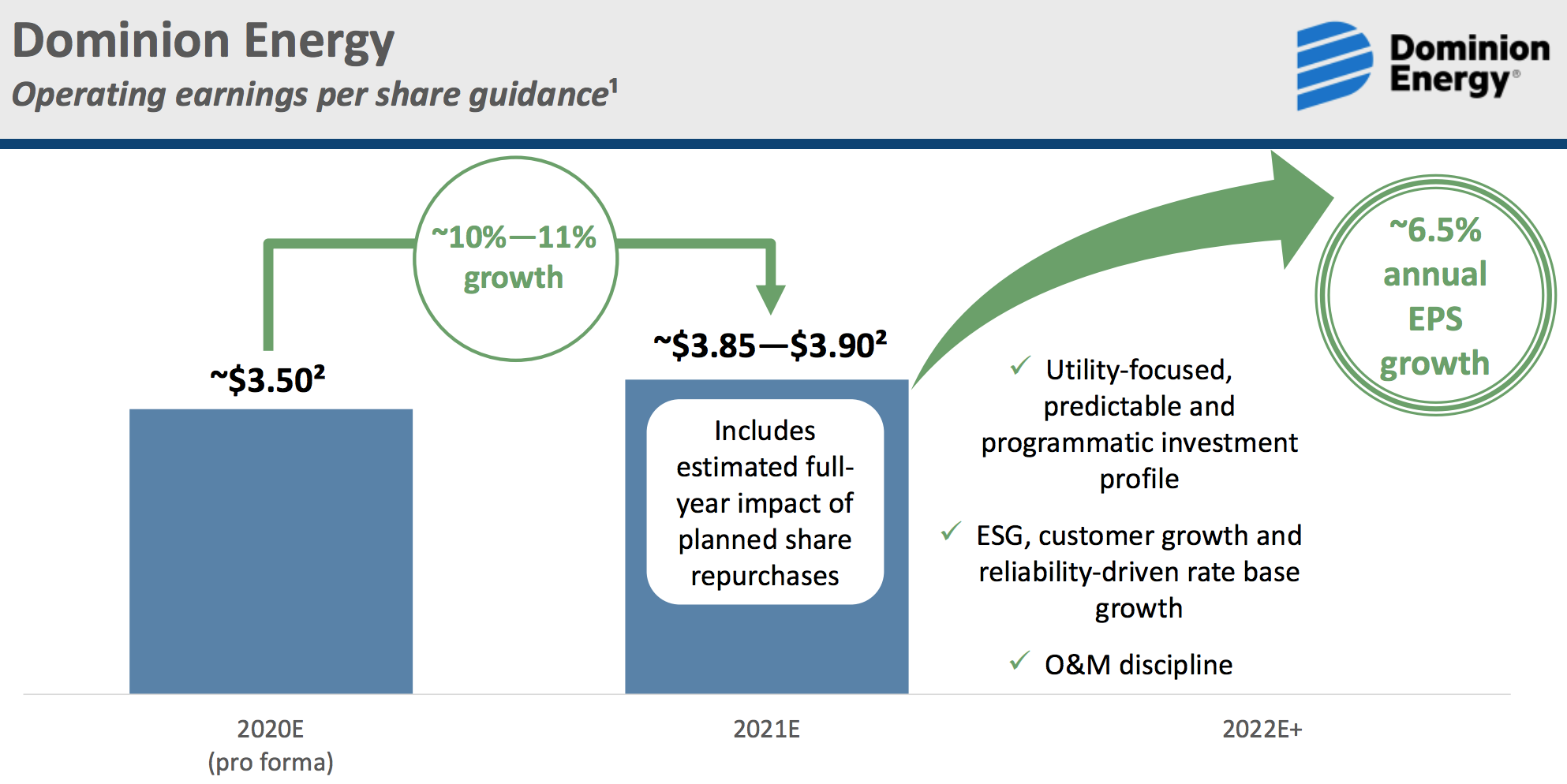

By shedding its lower-growth gas transmission and storage business, Dominion believes it can achieve 6.5% annual EPS growth beginning in 2022, up from its prior long-term growth guidance of 5%.Source: Dominion Investor Presentation

Similarly, Dominion believes its new dividend can grow approximately 6% annually, much faster than its current 2.5% annual growth guidance (albeit off a lower base).

This growth profile is relatively strong compared to other pure-play regulated utilities, potentially helping Dominion achieve a stronger valuation (midstream assets have fallen out of favor in recent years).

Perhaps further supporting its valuation as ESG investing gains in popularity, Dominion believes shedding some natural gas exposure will help it achieve net zero carbon and methane emissions by 2050.

This divestiture is expected to give Dominion an "industry-leading clean energy profile" as its utilities continue investing in wind, solar, and battery storage technologies. These issues may become increasingly important to regulators and customers in the decades ahead.

It's also worth mentioning that Dominion pulled the plug on its majority-owned (53%), $8 billion Atlantic Coast Pipeline project, which had experienced substantial delays and cost overruns.

This action keeps the utility's natural gas pipeline footprint minimized and is not expected to have a material change on the firm's credit metrics.

Looking ahead, Dominion's business mix should remain very strong and continue generating predictable earnings.

While today we are downgrading Dominion's Dividend Safety Score to Unsafe to reflect the upcoming dividend reduction in the fourth quarter, we expect the new, lower dividend to earn a Safe rating once it's in place.

Dominion's new payout ratio will be around 65%, backed by a stable regulated earnings profile. The balance sheet will remain strong as well (Berkshire is taking on some of Dominion's debt in the deal).

The downside for income investors is that Dominion's new dividend amounts to only a 3% yield based on the stock's July 2 closing price. Dividend growth prospects are much better, but the investment's appeal for generating current income has been reduced.

As a result of this news, we wouldn't be surprised if Dominion's stock traded off today.

Retail investors who own the stock for current income will be disappointed by the unexpected dividend change, and it's hard to imagine management walking away with a lucrative deal with Warren Buffett on the other side of the table.

For now, we plan to continue holding our shares of Dominion. The utility expects to maintain its regular 94 cents per share dividend in the third quarter (next ex-dividend date expected in early September) before aligning its payout with its lower earnings base.

At that time, we will consider rotating into alternative ideas that can generate stronger current income (a key objective of our Conservative Retirees' portfolio).

We don't expect the value of Dominion's regulated utilities to materially change over that time period, reducing the downside risk of continuing to hold.

Management also has a solid long-term track record of creating value for shareholders, so it's possible that investors will warm up to this deal as it's better digested.

We will tune in to Dominion's call this morning and provide additional updates as necessary.