Con Edison's Dividend Continues to Look Safe Despite Pandemic Impact

Since bottoming on March 23, shares of Con Edison (ED) have returned less than 20% while the utilities sector (XLU) has rallied 40%.

As a result, Con Ed's dividend yield still hovers near 4%, above its longer-term average.

Like its peers, Con Ed faces a number of challenges stemming from the pandemic including reduced power consumption, higher bad debt expenses, and rockier credit markets.

But Con Ed's service territory footprint magnifies some of these issues.

The regulated utility generates the vast majority of its earnings from providing electricity and gas to the New York City area, one of the hardest hit parts of the country.

In early May, Con Ed reported that its commercial electric delivery volumes were down nearly 20% year-over-year from March 16 to April 30, excluding weather impacts. This drove a double-digit decline in commercial electric revenues.

Residential electric volume increased about 10% as more people worked from home. But this wasn't enough to offset weakness in commercial markets, which account for a little over half of Con Ed's overall electric delivery volumes.

Overall energy demand remained around 15% lower than normal in New York City during the last two weeks of May as many businesses were still closed, according to data cited by The Wall Street Journal.

Based on what we know today, we do not believe these headwinds threaten the safety of Con Ed's dividend.

Decoupling refers to regulatory policies designed to ensure revenue earned by utilities is in line with what they need to cover costs and earn a fair return, reducing their incentive to sell more power.

Under decoupling plans, rates change with consumption to meet predetermined revenue targets, according to ASE.

Approximately 87% of Con Ed's revenues are subject to regulatory recovery mechanisms such as revenue decoupling.

As a result, in May Con Ed reduced its full-year earnings guidance by just 3%, mostly reflecting the impact of warmer than normal winter weather on its steam business which doesn't have revenue decoupling.

Con Ed's rate plans also provide for more than $50 million of bad debt expense in 2020 (about 0.5% of revenue), further reducing earnings volatility.

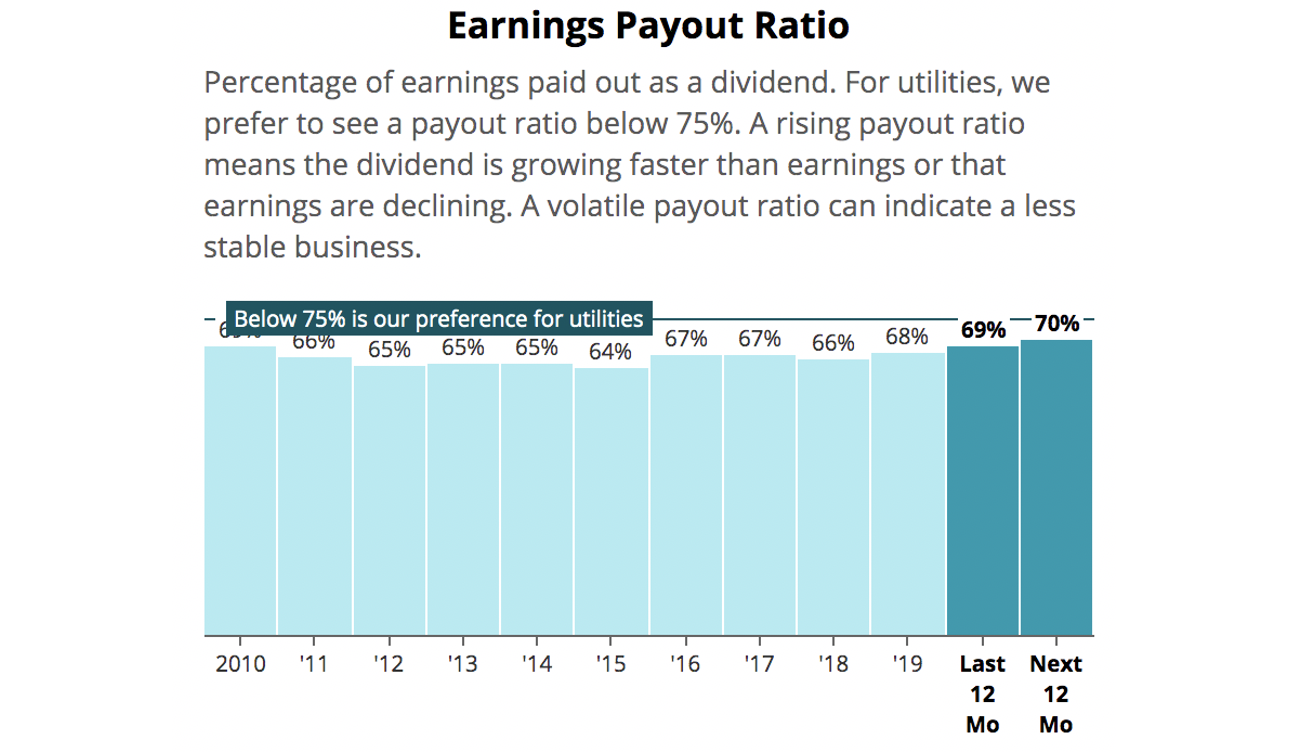

Based on Con Ed's latest forecast and updated analysts' estimates, the utility's payout ratio is expected to remain at a reasonable level near 70% this year.

Source: Simply Safe Dividends

Con Ed's balance sheet and liquidity remain supportive of its dividend as well.

The company's BBB+ credit rating has allowed it to continue accessing debt markets on favorable terms, including a new $750 million supplemental credit agreement entered into in April 2020.

At the end of March, Con Ed had about $1.4 billion of cash and $1 billion of borrowing capacity available under its primary credit facility.

That's plenty of firepower to cover its remaining 2020 debt maturities of $518 million in the unlikely event that refinancing temporarily became difficult.

If needed, Con Ed's liquidity appears sufficient to cover most of its financing plan for 2020, too. The company expected to issue between $1.5 billion and $2 billion of long-term debt and up to $600 million of equity.

That said, it's important for New York City's economic activity to resume without major setbacks. (New York City began phase one of its reopening plan on June 8.)

Regulators are not keen on transferring additional costs to ratepayers during this time of high unemployment, and decoupling wasn't designed for a sudden economic contraction triggered by a pandemic.

Should power demand remain unusually weak for an extended period, ratings-firm Fitch notes that decoupling mechanisms may not be fully protective of Con Ed's revenue stream or recovery time could be deferred (lost revenue is typically recovered 6-12 months later).

With more people staying at home this summer, Con Ed could face unusual stress on the grid as well. The firm is bracing for a heat season unlike any other due to an expected surge in use of residential air conditioning units.

Additional investments may be necessary to shore up its infrastructure, and social distancing measures have made it more challenging to complete work.

Overall, we believe the utility's decoupling mechanisms, liquidity, and investment-grade balance sheet position it to weather a temporary slump in commercial energy demand.

While the pace of growth will likely remain slow, Con Ed appears positioned to continue its 46-year streak of increasing dividends (the longest streak of any utility in the S&P 500).

The most important factors we will continue monitoring are the trajectory of New York City's economic recovery and regulators' willingness to continue supporting Con Ed's needs during this unusual period of stress.

For now, we don't expect these issues to threaten Con Ed's Dividend Safety Score.