NetApp's Dividend Safety Score Downgraded to "Safe" Due to Growth Challenges

NetApp (NTAP) sells hardware and software to enterprises implementing data storage solutions at on-premise data centers and within cloud environments.

Modern companies produce huge amounts of data that can be rapidly analyzed, securely accessed, and easily monitored with NetApp's storage solutions.

Competition is stiff. Not only does NetApp contend with hardware providers like Dell, IBM, and numerous startups, but cloud providers (Amazon, Google, etc) have disrupted the traditional model of companies purchasing their own equipment.

Still, many enterprises (for regulatory reasons or otherwise) demand on-premise or colocated storage, which is where NetApp excels.

Meanwhile, NetApp is adapting to the emergence of the cloud and offers "hybrid cloud" integrations that fuse companies' cloud and non-cloud storage.

Only 40% of NetApp's fiscal 2020 revenue was recurring in nature, making the majority of sales dependent on somewhat discretionary IT spending, much of which was put on pause in March due to the pandemic.

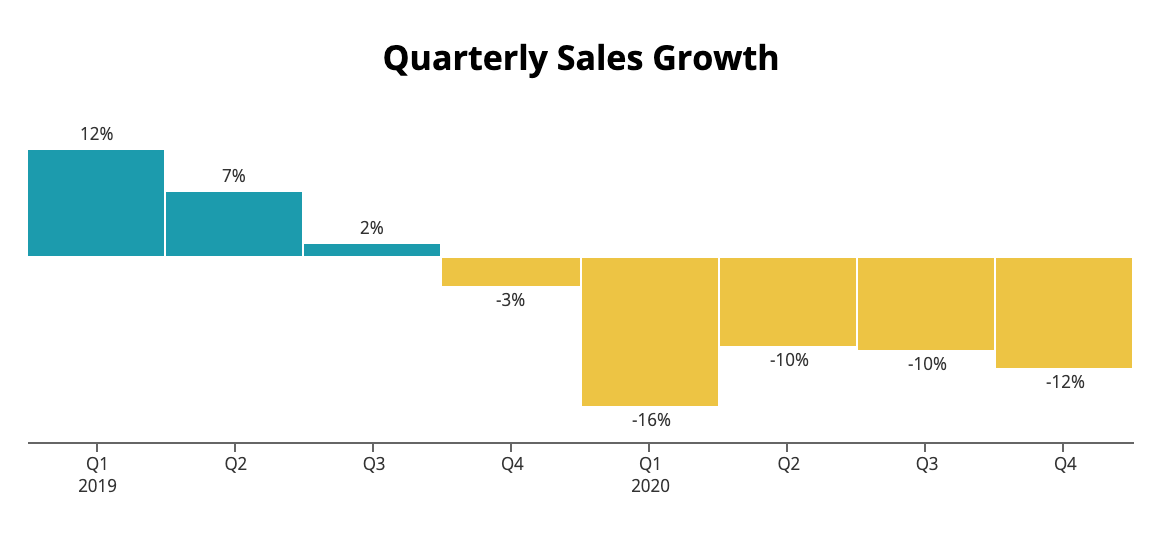

NetApp reported earnings on May 27. In the quarter ended April 24, sales were down 12% year-over-year. The pandemic's impact is expected to be steeper in the current quarter, with management guiding for EPS to decline 32% to 44%.

While visibility is limited beyond the summer, analysts forecast NetApp's EPS to be down 19% over the next year, pushing up NetApp's payout ratio to 58%.

Source: Simply Safe Dividends

58% isn't an alarmingly high payout ratio, especially if business rebounds. Indeed, NetApp's CEO said the dividend will be maintained unless "we see some structural impairment to our free cash flow, which we don't see at the moment."

The concern, then, is that business doesn't return to previous levels, which would constitute a "structural impairment to free cash flow".

Technology trends are difficult to predict. Nonetheless, NetApp's products may lose relevance as more companies ditch costly on-premise data centers in favor of cloud services, where NetApp plays a smaller role.

It's also possible the coronavirus pandemic will hasten the adoption of cloud technology, especially if work-from-home becomes more commonplace.

Moreover, competition is intensifying as more startups enter the storage device market and cloud providers like Amazon encroach on NetApp's territory, seeking ever-larger slices of massive enterprise IT budgets.

In fact, these cloud trends are already playing out. NetApp's sales peaked at $6.3 billion in 2014 and have declined by 10% or more in each of the last four quarters, highlighting the company's struggle to sustain positive growth.

Source: Simply Safe Dividends

The good news is that a large installed base, which yields recurring maintenance revenue, and sizable distribution network (sales offices in 43 countries and strong relationships with resellers) help NetApp consistently generate free cash flow.

But the longer growth struggles persist, the more pressure NetApp will feel to pursue acquisitions or invest in new products to spur growth.

While an outside risk at this point, reducing the dividend could eventually become a consideration to retain more cash for investing in growth projects.

Fortunately, NetApp carries more cash ($2.8 billion) than debt ($1.7 billion), and leverage (gross debt to EBITDA) is expected to be 1.4x this year, well below the 3x threshold stipulated in the company's credit agreement with lenders.

Combined with a BBB+ credit rating from Standard & Poor's, NetApp's net cash position and healthy debt levels provide some flexibility to maintain the dividend while the company adapts to trends in the data storage industry.

But in recognition of NetApp's growth challenges and the risks they pose to the dividend, we are downgrading the firm's Dividend Safety Score to Safe.

For now, NetApp's dividend looks secure, but a further downgrade could be considered if sales weaken further or appear unlikely to rebound.