Exxon's Dividend Hinges on Oil Rebound and Management's Tolerance of Higher Leverage

None of the oil majors can cover their capital spending and dividends at today's oil price, even after slashing their investment plans.

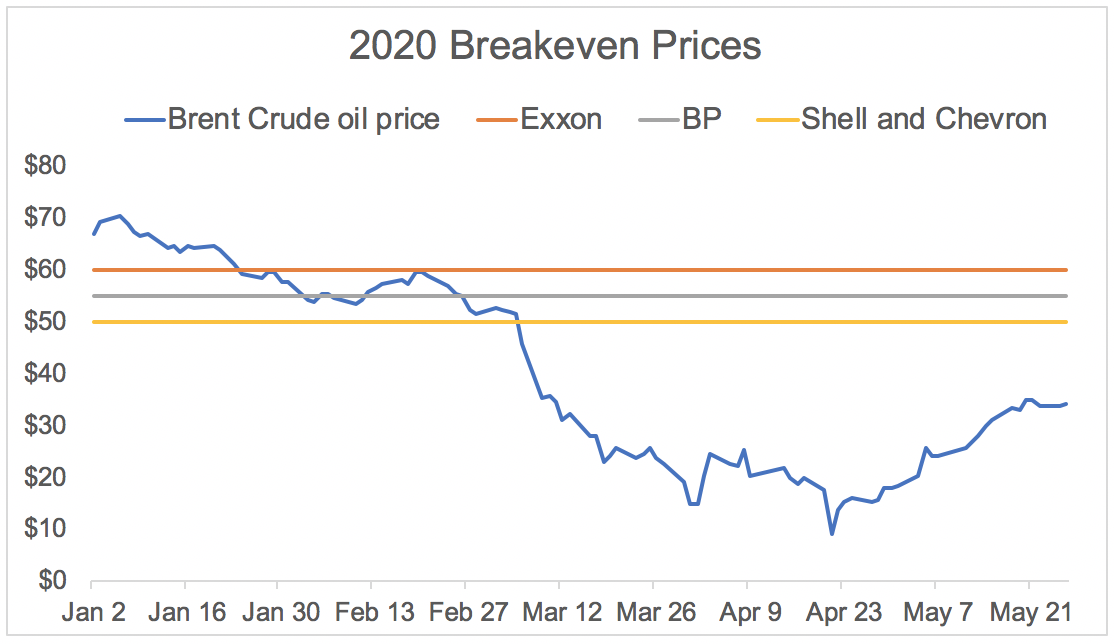

Oil needs to be closer to $50 to $60 per barrel for these companies to breakeven on their obligations, according to data from Bloomberg.

Source: Bloomberg, U.S. Energy Information Administration, Simply Safe Dividends

The price of oil has started to rebound off its April lows with lockdowns being lifted and supply falling. But at today's level near $35 per barrel, the oil majors will continue burning through cash.

With an estimated breakeven price of $60 per barrel, Exxon is no exception.

Facing these realities, Shell on April 30 announced its first dividend cut since World War II. Investors are worried other oil majors may soon follow suit.

So is Exxon's dividend safe? That's the question investors had following Exxon's May 1 earnings release and its annual shareholders meeting on May 27.

For now, Exxon still plans to maintain its dividend. Although the firm historically increases its dividend in April, this year Exxon held its payout flat.

The dividend's future trajectory depends on how long the current environment persists, and how far Exxon is willing to stretch its balance sheet in the meantime.

Exxon has paid uninterrupted dividends since 1882 and understands that the dividend is central to its investment case. This has made the company more willing to continue borrowing to preserve its payout.

If you look at our shareholder base, about 70% of them are retail or long-term investors that look for our dividend and see that as an important source of stability in their income. And so we have a strong commitment to that.

– Chairman and CEO Darren Woods, Q120 Earnings Call

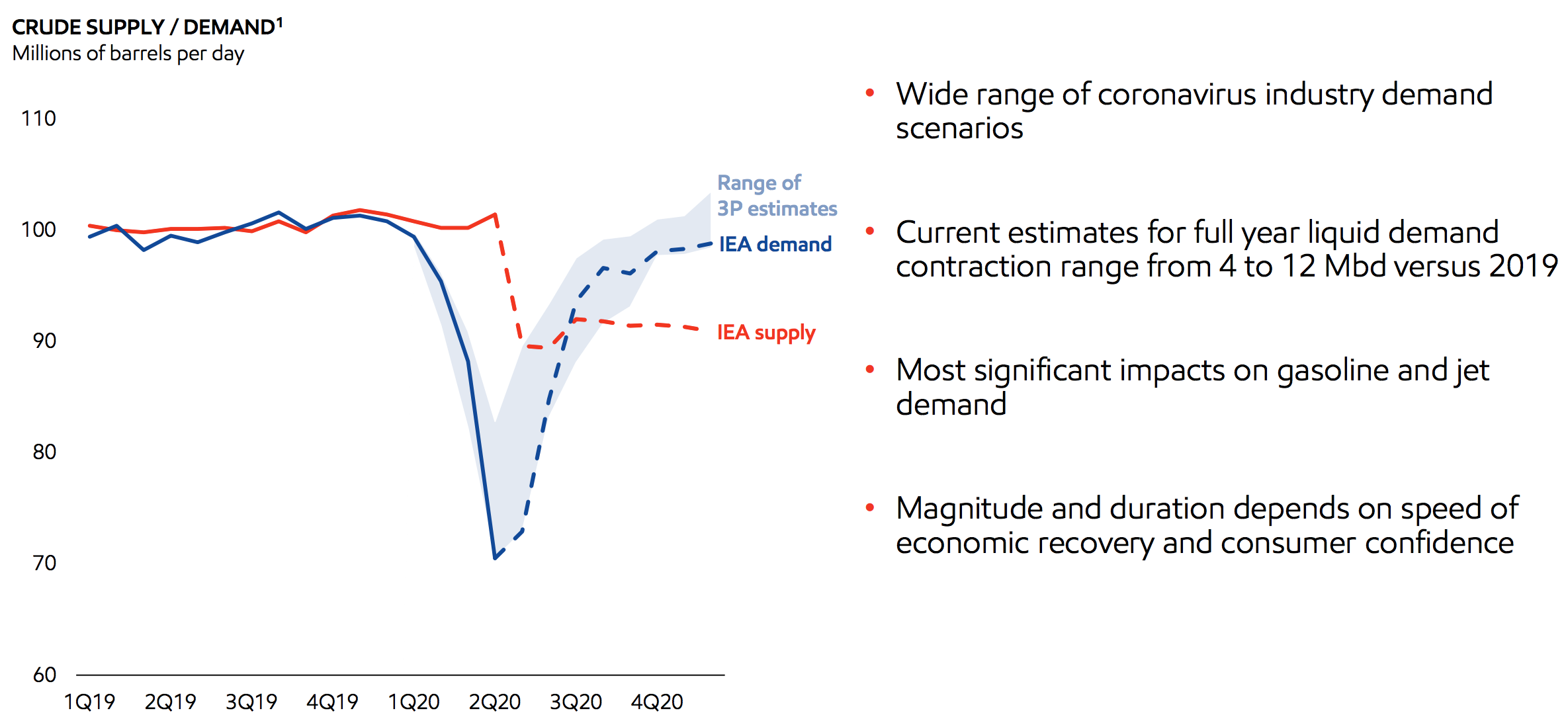

Based on third-party demand projections and announced OPEC+ supply reductions, management also sees potential for the oil market to come into balance and then go short sometime in the second half of 2020.

Source: Exxon Mobil Earnings Presentation

Exxon doesn't expect to see an improvement in prices until crude inventories are worked down, but a faster than expected recovery remains possible.

"Bottom line here, it's going to be a very challenging summer with a pretty sloppy market as we move into the back half of the year.

"We've adjusted our plans to a low price and margin environment through year-end. Our price projections tend to be at the low end of third-party estimates. Once again, I hope we're surprised with a quick recovery, which we have not ruled out, particularly given our ongoing experience in China."

– Chairman and CEO Darren Woods, Q120 Earnings Call

Barring a major setback in these projections, it would be surprising if management reduced the dividend in the short term given the potential for oil market fundamentals to begin improving by next quarter.

Until then, Exxon will continue borrowing to address its cash flow deficit.

Exxon's dividend costs $14.7 billion annually, and 2020 capital expenditures are now projected to total $23 billion after initial guidance was reduced by 30% in response to the crash in oil prices.

The company's operating cash flow is insufficient to cover these $37.7 billion of obligations in today's commodity price environment.

In the first quarter of 2020, when oil averaged $50 per barrel, Exxon generated $6.3 billion of operating cash flow (around $25 billion annualized).

If prices remain near $35 per barrel going forward, we estimate Exxon could burn through around $10 billion to $15 billion annually, depending in part on the success of its plan to lower cash operating expenses by 15%.

Asset sales could help reduce the cash flow deficit, but deal activity has slowed given the weakness in energy markets.

Instead, the balance sheet remains Exxon's primary lever to pull.

Liquidity is not a problem. In April, Exxon held about $18 billion of cash and had $15 billion of available borrowing capacity through its credit facilities. Less than $3 billion of long-term debt matures through 2021.

The company also maintains an AA credit rating from Standard & Poor's, helping it continue access debt markets on reasonable terms.

But no business can increase leverage forever, especially for the sake of maintaining a dividend.

At Exxon's investor day earlier this year, Exxon showed a slide suggesting that it would be comfortable taking its debt to capital ratio up from about 20% at the end of 2019 to 30%. Management said this would still be "within the range of peers."

On its earnings call earlier this month, Exxon disclosed that its debt to capital ratio was about 26% following its debt issuance in April.

Thanks to its scale, Exxon estimates that each 1% of incremental leverage equates to about $4 billion in additional debt.

In other words, Exxon could take on around $16 billion of incremental debt before hitting a 30% debt to capital ratio.

Coupled with the company's $18 billion of cash on hand, Exxon has over $30 billion of financial capacity at its disposal before it would hit its implied maximum leverage target.

Based on our estimate of the company's annual cash burn rate, Exxon could, in theory, maintain its current spending levels and dividend for around two years.

But this would be a risky strategy for several reasons. For one, Exxon's reduced capital spending level is already at an unsustainable level for a depletion business.

Exxon must continuously invest to replace the oil it pumps out in order to keep its long-term outlook stable. This year's spending cuts are expected to reduce 2021 production volumes by around 3%.

Maxing out leverage for the sake of paying dividends reduces Exxon's flexibility to be opportunistic as well.

As many as one in three shale players are expected to exit the market one way or another, per Bloomberg. This could allow the oil majors to acquire cheap assets and become even larger once we get to the other side of this crisis.

The bottom line is that Exxon may need to re-evaluate its capital allocation policy within the next year if the oil price environment has not shown meaningful signs of improvement.

Here's what Chairman and CEO Darren Woods said earlier this week at Exxon's shareholders meeting when asked if he would cut the dividend:

"First and foremost, we want to invest in advantaged projects. That's a priority because it maintains the foundation for a healthy and long-term business. We want to pay a reliable and growing dividend. It's our way of rewarding long-term shareholders and it shares our success over the years. And we need to maintain a strong balance sheet to ride to the ups and downs of the market...

"As you look at the short-term environment, we have given a priority to the dividends. And so we have not reduced that and instead have moved to cut our operating expenses and to reduce capital, while preserving the value of that capital over the long term.

"And we'll continue to assess that as we move forward, balancing across those three [capital allocation] priorities that we have. The Board looks at that every quarter and assesses it and continues to put a priority on those three priorities and in maintaining a dividend. So I think we'll have to see how the environment continues to go, but it is an important priority that the Board wants to maintain."

For comparison, Safe-rated Chevron has been much more vocal about the dividend's priority and its ability to support the payout through at least 2021 without taking excessive financial risk.

"We've got a long-standing financial framework that has the dividend as our #1 financial priority...

"On our first quarter earnings call about a month ago, we laid out a stress test, where we showed the financial state of the company and our balance sheet if we have 2 years of $30 Brent crude pricing, continue to invest in our business, sustain the dividend and it shows that we still exit 2021 with a very strong balance sheet and good financial health [including a net debt to capital ratio below 25%]. So that was an attempt to lay out for investors the the safety of our dividend and the actions we're taking to protect it."

– Chairman and CEO Mike Wirth, Chevron's Annual Shareholders Meeting

Overall, Exxon's Borderline Safe Dividend Safety Score reflects the uncomfortable situation the firm's payout is in if the current environment persists longer than expected.

The dividend's safety hinges on oil prices returning to their late 2019 levels within the next year or so, plus management's tolerance to continue borrowing for now.

Oil prices above $60 per barrel are needed by most major oil-producing nations to balance their budgets. But how long it takes for fundamentals to normalize is anyone's guess.

Supply side dynamics are extremely complex thanks to disruption caused by U.S. shale players, and demand recovery is still in the early days as the pandemic's impact lingers.

Exxon's valuation reflects many of these uncertainties, but current shareholders should evaluate how comfortable they are with these risks.

Exxon's Dividend Safety Score could be downgraded later this year if conditions in the oil market fail to improve meaningfully. We will continue monitoring the situation and provide updates as needed.