Extended Lockdowns Increase Risk Profile of Urstadt Biddle's Dividend

On April 8, we discussed the coronavirus-related challenges facing Urstadt Biddle (UBA).

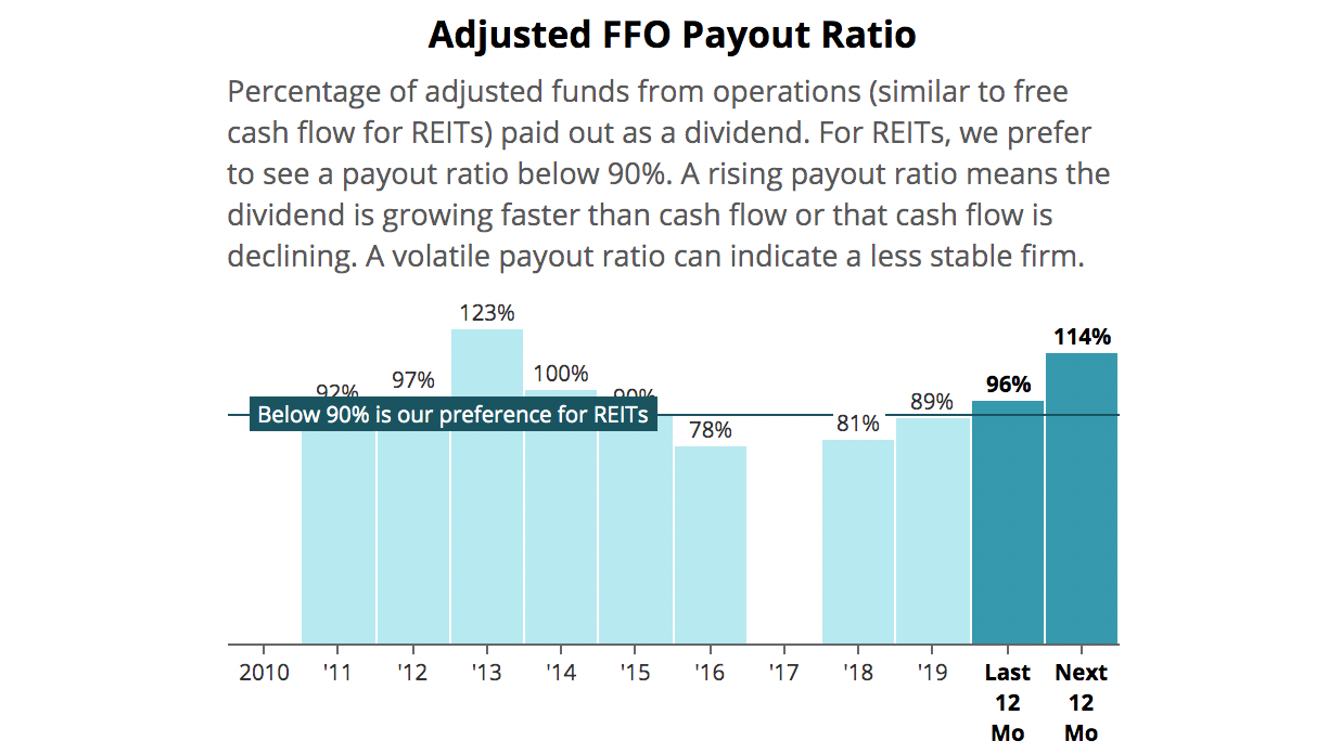

Our primary concerns were the firm's small size (only 81 properties), concentrated operations in ground zero of the pandemic (New York), relatively high payout ratio entering the crisis (80% to 90%), and signs that numerous tenants (e.g. Staples) may skip their rent.

More news has arrived over the past month, and it doesn't bode well for Urstadt Biddle's dividend safety profile.

On May 11, New York City's Mayor Bill de Blasio said the city's lockdown will likely continue into June.

Urstadt Biddle's properties aren't located directly in downtown Manhattan, but most of them are within 50 to 75 miles away. Tenants could now be looking at extended lockdowns, making them even less willing or able to pay rent.

Most retail-focused REITs have also reported earnings in recent weeks. Based on the reports we've seen, shopping center REITs on average collected only around 60% to 70% of April rent.

Given Urstadt Biddle's footprint, we expect its rent collection figure to be even lower. The REIT also has exposure to various troubled industries including restaurants (12% of rent), gyms (5%), clothing / accessories / jewelry (5%), department stores (5%), and bedding (2%).

We estimate that the dividend would no longer be covered by cash flow if rent collections fell by around 5% to 10%. That seems like almost a certainty at this point, and analysts have also begun to forecast the REIT's payout ratio above 100% this year.

Source: Simply Safe Dividends

As it pertains to dividend safety, the question then becomes how willing Urstadt Biddle will be to borrow to pay its dividend until rent collection improves.

The REIT has paid uninterrupted dividends since its founding in 1969 and increased its dividend for 26 consecutive years, but management has never experienced a crisis like this one.

Although its balance sheet has capacity, we would be surprised if Urstadt Biddle was willing to increase its leverage for the sake of maintaining its dividend.

That's not a conservative approach, especially in this environment, and a V-shaped recovery for its tenants (and rental income) seems unlikely.

Many retail-focused REITs have opted to temporarily suspend their dividends, even if they had investment-grade credit ratings, healthy liquidity, and above-average rent collection rates.

Notable exceptions include Realty Income (O), National Retail (NNN), and Federal Realty (FRT) which have similar dividend streaks to defend but are much larger and more diversified than Urstadt Biddle.

Based on what we know today, Urstadt Biddle may announce a substantial dividend cut or even a temporary suspension when it declares its next payout in early June.

Therefore, we are downgrading Urstadt Biddle's Dividend Safety Score from Borderline Safe to Unsafe.

However, we believe Urstadt Biddle has the balance sheet and liquidity to survive this crisis.

In its annual reports, management focuses on the company's total debt to total assets ratio, which sat near 30% last quarter.

Urstadt Biddle has in the past highlighted that other shopping center REITs have a debt to assets ratio around 40%, and even its ratio has sat near 35% at times.

In other words, there's flexibility for leverage to move higher if rent collection is so poor that the REIT's expenses are not covered in the short term. (We estimate that could happen if revenue falls around 40% to 50%.)

Liquidity isn't an issue for now either. Urstadt Biddle maintains a $100 million revolving credit facility and has no significant debt maturities until 2022.

For perspective, the firm's adjusted funds from operations (similar to free cash flow for REITs) was projected to be around $50 million prior to the pandemic.

Looking ahead, the coronavirus pandemic has potential to accelerate the decline of financially weaker retailers and some of the secular headwinds (e.g. e-commerce) facing parts of brick-and-mortar retail.

Urstadt Biddle's properties seem somewhat insulated since new supply is limited in the densely populated markets it serves. However, it could take a long time for the business to return to pre-pandemic rent and occupancy levels, assuming the value proposition of its shopping centers remains intact.

Urstadt Biddle's valuation doesn't look very demanding, but current shareholders should weigh if they are comfortable owning a stock that could reduce its dividend significantly while also facing a potentially long road to recovery.