Whirlpool's Dividend Looks Safe, But Severity of Downturn Looms Large

Whirlpool (WHR) reported earnings on April 30 and provided investors with a first glimpse into the impacts of the pandemic on sales in the home appliance maker's two most important regions, the U.S. (54% of 2019 revenue) and Europe (21%).

Both regions saw sharp drop-offs in retail sales in March as people began to stay home and stores closed. Demand has since started to recover, albeit slowly.

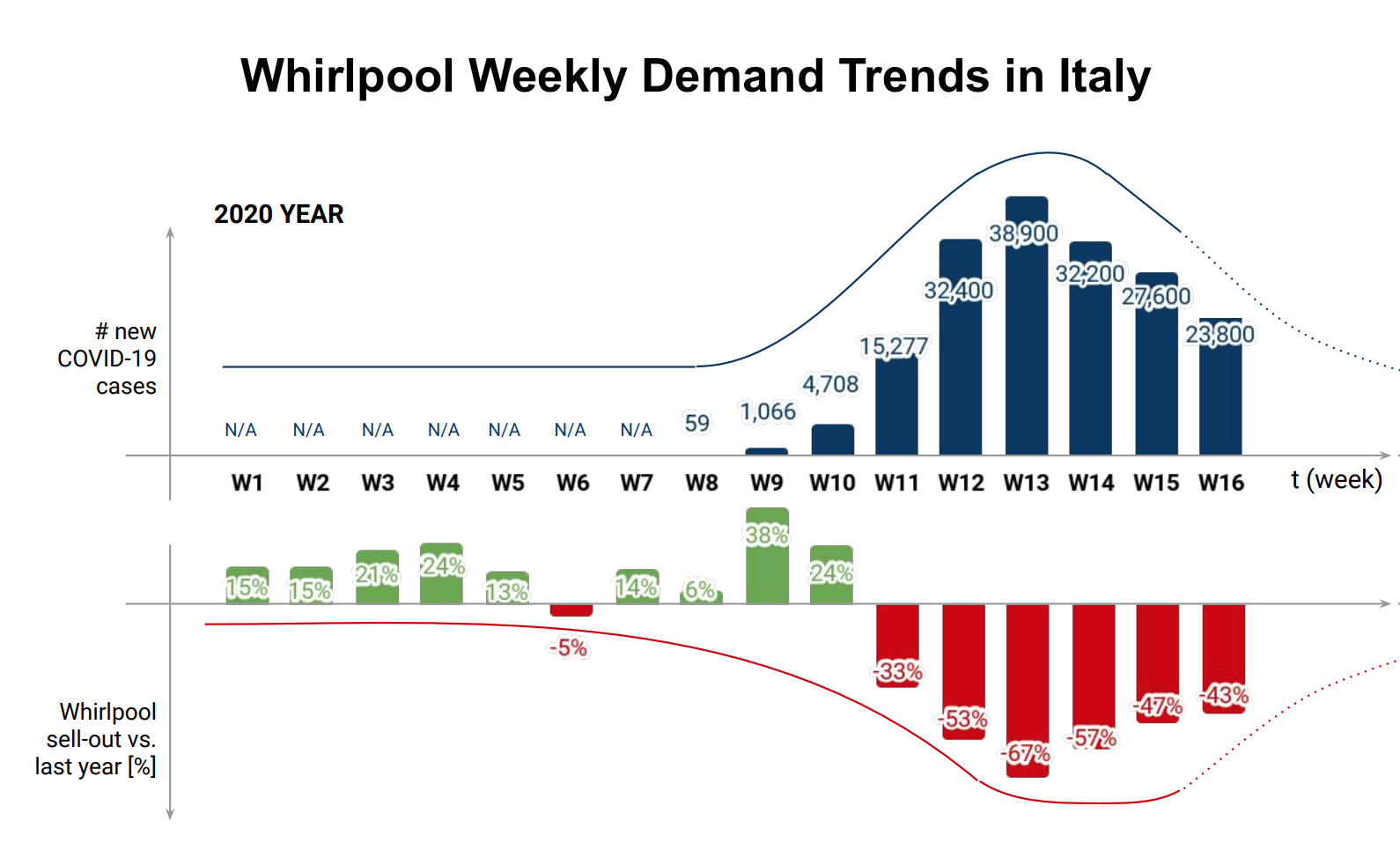

In Italy, demand bottomed out at negative 67% year-over-year in mid-March but has improved each week since. Similar trends were observed elsewhere in Europe.

Source: Whirlpool Investor Presentation

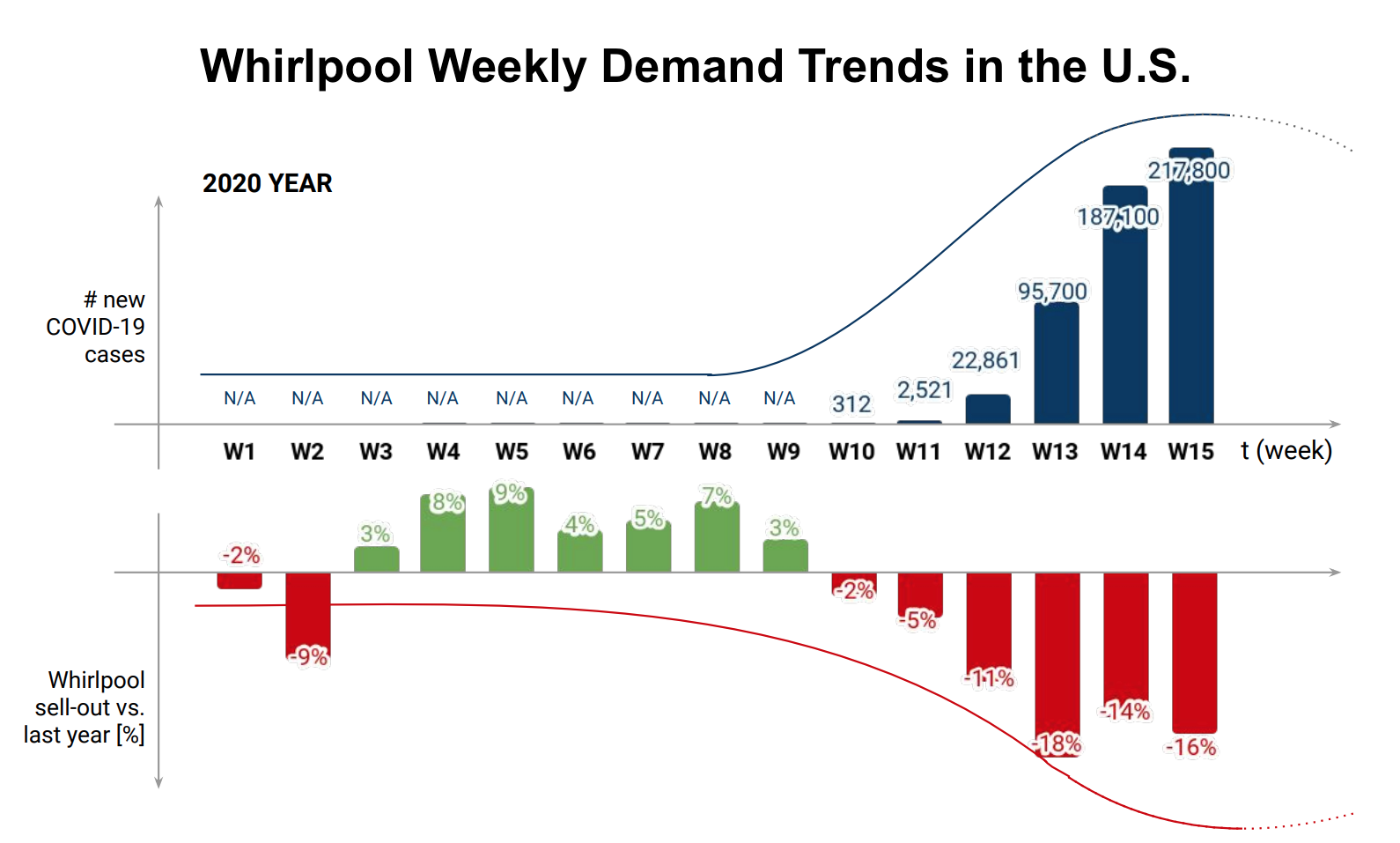

The trough was less pronounced in the U.S. at an 18% year-over-year decline in demand near the end of March. Management expects improvement in the months ahead similar to what's been observed abroad.

Source: Whirlpool Investor Presentation

While acknowledging the difficulty in making predictions in the midst of the pandemic, management felt they had enough data to suggest that the most likely outcome is a U-shaped recovery with a return to growth by the end of the year.

For 2020 as a whole, Whirlpool believes organic revenue will decline 10% to 15%. Fitch Ratings similarly forecasts a sales decline of around 15% this year.

For context, Whirlpool's organic sales (which excludes the impacts of newly-acquired businesses and foreign currency) dropped 12% during the last recession.

In other words, the magnitude of the current downturn is shaping up to be worse than the financial crisis, though a total disaster appears unlikely.

Moreover, Whirlpool's sales may return to growth faster than during the last recession, which dragged out for several years. Time will tell.

Nevertheless, Whirlpool's Very Safe Dividend Safety Score was premised on the company facing a downturn no more severe than the financial crisis, which was an unusually bad recession and period for dividends.

Given the increased likelihood of a relatively more severe downturn, we are downgrading Whirlpool's Dividend Safety Score to Safe.

If evidence grows that the looming downturn will be more severe and prolonged than management is expecting, we would consider another downgrade.

For now, we expect Whirlpool's low payout ratio and moderate leverage coming into the pandemic to support the dividend during this rough stretch.

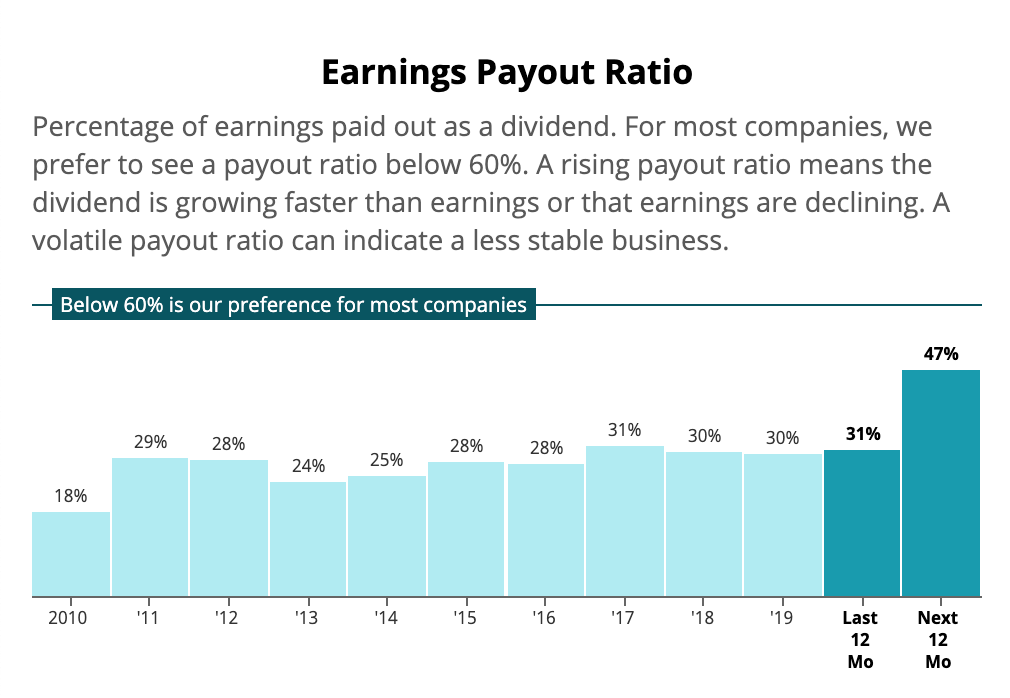

Analysts currently forecast Whirlpool's earnings per share to fall 35% over the next twelve months, pushing up the company's earnings payout ratio to 47%.

Source: Simply Safe Dividends

While Whirlpool hasn't seen a payout ratio this high in at least two decades, it's still not an alarmingly high level given the firm's healthy financial position.

The company currently has $2.8 billion in cash on hand and access to an additional $2 billion through its revolving credit facilities. No debt matures this year, and only $300 million of debt is due for repayment in 2021.

Whirlpool's substantial cash reserve (the dividend costs just $310 million compared to $2.8 billion in cash) and minimal financing needs make it easier to continue paying out cash to shareholders.

Furthermore, analysts at Fitch expect Whirlpool to generate enough free cash flow this year to cover the dividend and capital expenditures, so maintaining the payout shouldn't require burning through cash.

Fitch also reaffirmed Whirlpool's investment grade BBB credit rating in April with the expectation that, as cash flow falls this year, leverage (debt to EBITDA) will rise but return to reasonable levels within the next few years.

In addition, Whirlpool isn't at risk of breaching debt covenants with lenders, an important consideration when cash flow declines sharply.

The firm's credit agreement stipulates that the company's debt to capital ratio cannot exceed 65%. Whirlpool's current debt to capital ratio is about 50%, which we estimate leaves room for an additional $3.4 billion in debt to be taken on.

Whirlpool must also maintain an interest coverage ratio (EBITDA to interest expense) above 3x (currently 10x). EBITDA could fall roughly 70% before this covenant is breached, a long ways from the 20% drop forecasted by analysts.

Of course, these thresholds are not necessarily Whirlpool's internal targets, but they demonstrate the company's financial flexibility at a time when many businesses are scrambling to preserve cash and shore up their balance sheets.

Thanks to this flexibility, management declared the company's regular quarterly dividend payable in June and reiterated their commitment to the payout:

Lastly, I'd like to touch on our capital allocation plans which have temporarily changed in light of our current situation.

Although we repurchased approximately $120 million in shares in the first quarter, we will be suspending additional share repurchases until our future liquidity needs become clear.

That said, we did declare our quarterly dividend and remain strongly committed to returning value to shareholders through these difficult economic times.

All said, the economic environment is changing rapidly as the pandemic progresses and more is learned about consumer spending during the pandemic.

A lot could change in the next several months. We will continue to continue to monitor Whirlpool's results, and we'll provide updates as necessary.