COVID-19 Threat Continues to Mount, Pressuring Ventas' Dividend

On March 16, we discussed how the coronavirus pandemic could hurt the performance of Ventas' (VTR) senior housing business.

Since then, the number of challenges facing Ventas across almost all parts of its portfolio has continued to rise.

As a result, the firm's cash flow now seems likely to fall short of its dividend for the foreseeable future. While Ventas could borrow to continue paying its dividend, it may choose not to in this highly uncertain environment.

Given this backdrop and the conservative view we take when assessing dividend risk, we are downgrading Ventas' Dividend Safety Score from Borderline Safe to Unsafe.

Let's take a closer look at what has changed since mid-March. As you can see, senior housing is Ventas' most important business, accounting for just over 50% of net operating income (NOI).

Source: Ventas Investor Presentation

The firm generates a little over 30% of its NOI from senior living properties it operates itself. While this eliminates credit risk, it exposes Ventas more to the ups and downs of the industry than if the firm solely collected rent from outside operators.

Another 20% of NOI is from senior housing leased to third-party operators who pay Ventas rent.

In recent weeks, it's become clear that the coronavirus is materially impacting the fundamentals of the senior housing industry.

Peer National Health Investors (NHI) reports weekly data regarding the prevalence of coronavirus across its 238 senior living and skilled nursing properties.

On March 18, the company stated it was unaware of any positive COVID-19 tests.

However, as of April 21, NHI said that 21 of its 160 senior housing buildings had at least one COVID-19 case, up from 12 at the end of March.

Another 133 of NHI's senior living communities are either self-quarantined, have testing in progress, or are located in areas with more than 100 confirmed cases.

As testing increases and awareness rises (some infected people are asymptomatic), more communities could join the list.

As of March 28, Ventas said that 33 of its 740 senior housing communities had experienced at least one confirmed COVID-19 diagnosis.

If its trajectory has followed NHI's, then it's possible that this figure has since doubled to represent close to 10% of Ventas communities.

This development, and the widespread fear it has caused for existing and future residents, doesn't bode well for the industry's outlook.

For example, healthcare REITs New Senior Investment Group (SNR) and Healthpeak Properties (PEAK) both reported 30% to 40% declines in move-ins last month compared to earlier this year.

Some analysts believe senior housing demand could fall by as much as 15% and occupancy could slip to a record low.

In a March 31 filing, Ventas said that occupancy in its senior housing operating portfolio started trending lower in the second half of March.

The REIT also noted that "inquiries and tours have begun to decrease materially and move-ins have begun to slow...[and] move-outs may become elevated as a result of the pandemic."

Ventas has also seen costs rise as operators take actions to protect caregivers and residents and increase screening and infection control efforts.

While Ventas collected "substantially all" of its rent for March, the outlook isn't good going forward.

Prior to the pandemic, Ventas' senior housing operators had rent coverage (i.e. ratio of cash flow to rent expense) of just 1.1x.

In other words, operators were already barely able to cover their rent payments with cash flow. With occupancy slipping and operating costs rising for the foreseeable future, some of these operators will be unable to pay their full rent.

Ventas recently established an April rent deferral program for its senior housing tenants (20% of NOI), allowing them to defer 25% of their April 2020 payment until the earlier of October 1, 2020, or receipt of government assistance.

The deferred payments are required to be used for operating expenses to care for seniors at Ventas communities and are expected to total $3 million to $9 million, or about 0.5% of the REIT's 2019 funds available for distribution (what pays the dividend).

While this is a dynamic situation, the challenges weighing on the senior housing industry seem likely to persist beyond April.

Other parts of Ventas' portfolio could face rent collection challenges as well.

Medical office buildings account for 20% of Ventas' NOI. These properties are leased to physicians, dentists, psychologists, therapists, and other healthcare providers.

While this is usually a resilient business, stay-at-home orders and social distancing have sapped demand for non-essential appointments.

Two-thirds of physicians surveyed by MDLinx said their patient visits have dropped by 50% or more in their practices, and dental practices have reported that patient volume in early April was less than 5% of normal.

Even though Ventas focuses on investment-grade tenants, it's hard to imagine all of them being willing or even able to pay their full rent given this backdrop.

Health systems such as hospitals account for another 6% of the REIT's NOI and face similar pressures.

The CDC in March recommended that non-essential procedures and appointments be rescheduled in order to keep hospital beds available for a potential surge in COVID-19 patients and to conserve protective equipment.

Hospitals make most of their money on elective procedures, so they have seen their largest revenue stream dry up, according to the Wall Street Journal.

For example, earlier this week HCA Healthcare said it has seen a 70% drop in outpatient surgeries at its hospitals in April so far, according to Reuters.

Envision Healthcare, one of the largest physician staffing firms in America, is said to be considering filing for bankruptcy due to the plunge in elective surgeries.

Overall, we estimate that around 80% of Ventas' NOI is under pressure from the pandemic and would be surprised if these headwinds quickly abated.

Extra precautions should continue at senior living facilities to keep them safe (keeping costs elevated), and many folks remain fearful of going in for non-essential appointments. A long, slow path to recovery could be the base outcome.

Unfortunately, this means Ventas may not return to covering its dividend for a while.

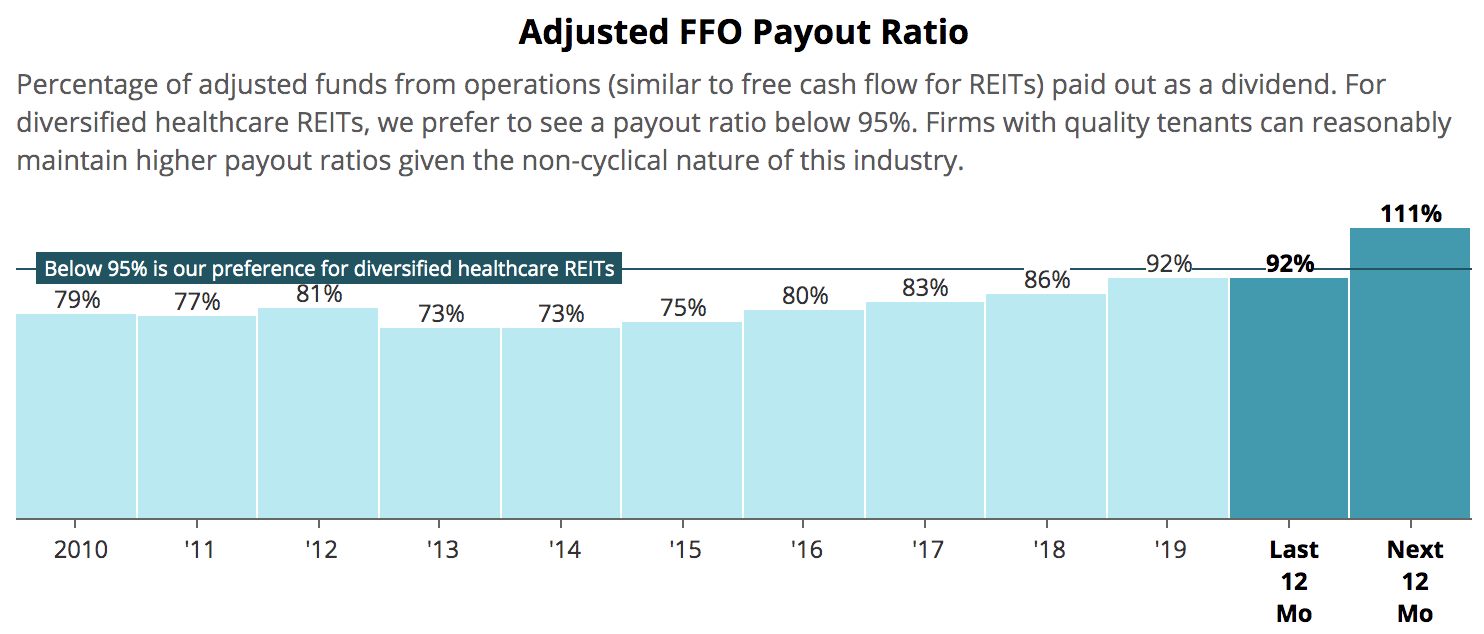

The REIT's payout ratio was above 90% heading into the pandemic as management had taken actions to shed weaker properties, and analysts now expect the dividend to exceed cash flow in the year ahead.

Source: Simply Safe Dividends

Reducing the dividend, which costs $300 million per quarter, would provide Ventas with greater flexibility to navigate these unprecedented challenges.

With that said, Ventas has the liquidity to wait things out if it wants to. As of March 27, Ventas had $2.9 billion in cash after drawing down its revolver. The firm also recently priced $500 million of notes.

If Ventas' rent revenue and resident fees fell 20% this year, which seems like an extreme outcome, we estimate the REIT would have a $700 million cash flow deficit after paying its current dividend.

Even after accounting for the REIT's $700 million of debt maturing through 2021 and moderate development spending, Ventas' current liquidity could handle that for a period of time.

But with Fitch and Moody's already revising Ventas' credit rating outlook to negative and no clarity on when the dividend will be covered by cash flow again, management may not feel it's prudent to go down that path.

Ventas' stock price already reflects at least some of these coronavirus-related risks, but investors should review whether they are comfortable with their positions given the growing uncertainty facing the industry. We will continue monitoring the situation.

.png)