Labor Market Disruption Seems Unlikely to Affect Paychex's Dividend

Paychex (PAYX) provides payroll and human resource services to small- and mid-sized businesses across a wide range of industries. The firm's operations historically generated predictable free cash flow and high margins.

Even during the 2007-09 financial crisis, Paychex's payroll services segment only experienced 2-3% annual revenue declines, and its human resources division grew each year. Each year free cash flow continued covering Paychex's dividend, which management has paid without interruption for more than two decades.

Paychex's businesses are driven by its number of clients and how many people its clients employ. These factors determine how many paychecks get sent out, as well as the level of HR benefits and services that can be provided.

Unfortunately, the coronavirus pandemic has begun to cause significant disruption in the labor market.

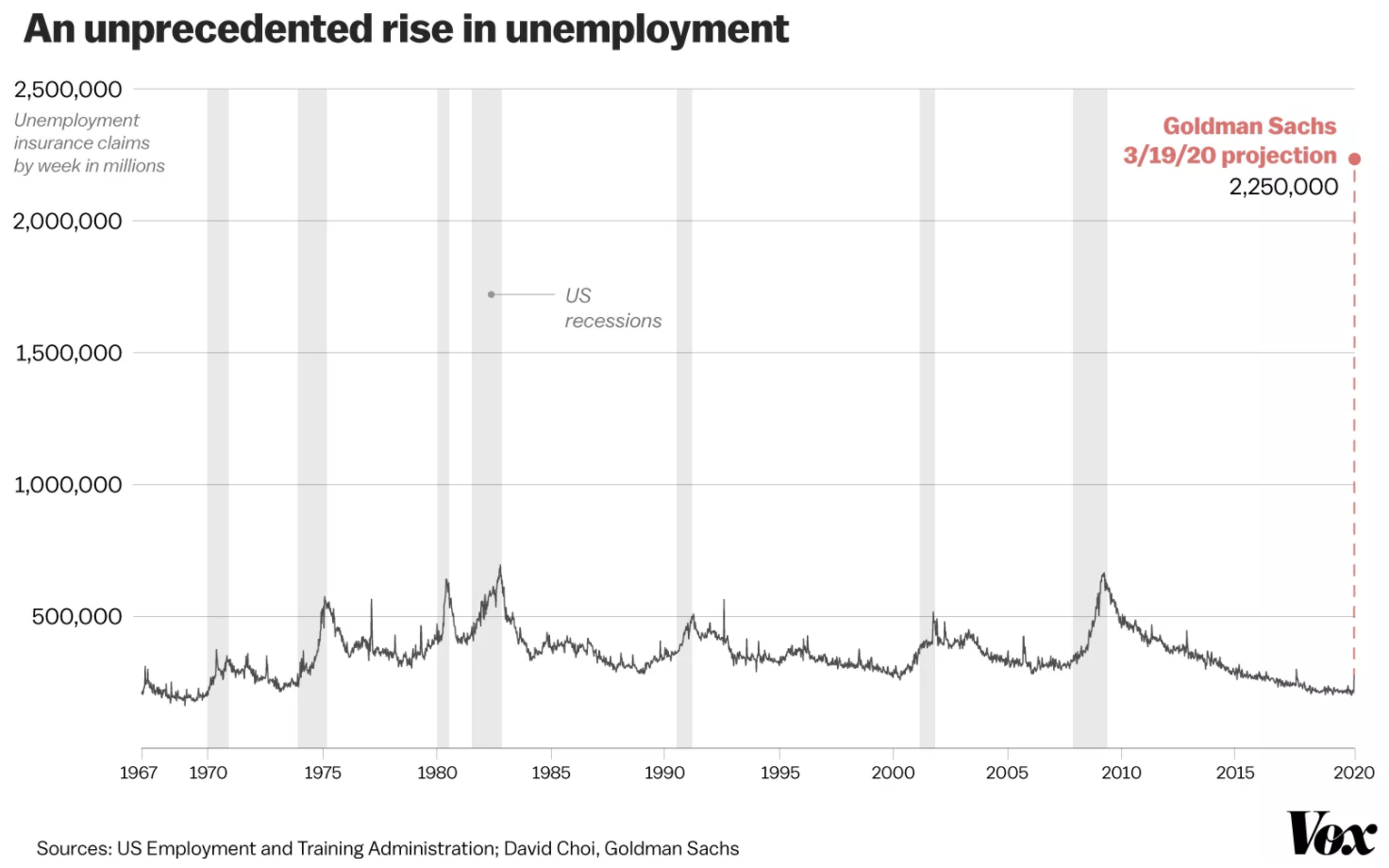

Analysts at Goldman Sachs predict more than 2 million people could lose their jobs very soon as coronavirus related closures lead many businesses to reduce headcount. That would be about three times the hit experienced in 2009.

Source: Vox

Of course, this is a very fluid situation as lawmakers continue debating fiscal stimulus packages designed to keep folks employed and getting paid until the virus is better contained.

In other words, it's hard to imagine unemployment figures staying that poor for long. The government is motivated to do nearly anything to prevent such a situation.

Paychex's business, which touches approximately 1.5 million of its clients' employees, could take an unusual short-term hit depending on what shakes out.

However, based on what we know today, we would be surprised if it was enough to cause management to rethink the firm's dividend strategy.

Paychex was tracking to generate about $1.3 billion in annual cash flow from operations. Capital expenditures are minimal in this business (mostly software and services rather than selling tangible products) and usually run around $100 million to $150 million per year.

That leaves roughly $1.2 billion of free cash available for Paychex's $900 million dividend, representing a payout ratio around 75% to 80%. While that may sound high, Paychex's durable cash flow has allowed it to always run its business like this, including during the last recession.

Source: Simply Safe Dividends

We estimate that Paychex's revenue could fall by more than 30% next quarter (or about 8% over a full year) and its dividend could still be covered by free cash flow this year, assuming a return to normal in subsequent quarters.

For context, during 2008 and 2009 the number of checks per client Paychex sent declined by 2% to 3% each year despite experiencing the worst business conditions in the company's history, according to management (in 2009):

It was difficult to watch our client losses due to companies going out of business or having no employees rise by 17% over the prior year. At the same time, our new client sales from new business formation declined by 19%.

We believe both conditions were the worst in Paychex's history, which explains our experiencing negative client growth for the first time in our history. While pricing conditions were more competitive, they did not have any significant impact on client share, as we believe we increased our market share in comparison to our significant competitors. On the new sales front, we added over 111,000 clients during the worst business environment most of us can remember.

Paychex's cost structure provides it with some flexibility to preserve cash flow during periods of weak demand, too.

The majority of Paychex's expenses are variable in nature, with compensation accounting for over half of the total. If business conditions really weakened for a sustained period of time, Paychex could consider trimming back its sales staff.

The company's balance sheet remains strong as well. Paychex has over $600 million in cash and access to $1.5 billion of borrowing capacity under its credit revolver. Paychex does have $800 million of debt (it was debt-free in 2009), but none of it is due until 2026 at the earliest.

Finally, we don't see material risk in the company's investment portfolio either. Parts of Paychex's payroll and insurance businesses involve collecting cash from clients before it needs to get remitted elsewhere (e.g. withholding taxes) or paid out as benefits (e.g. workers compensation) in the future.

Paychex invests these funds in a portfolio consisting of highly liquid, investment-grade securities. These investments seem very unlikely to get the company into trouble, and the firm did not realize any impairment losses on its portfolio during the 2007-09 financial crisis.

We plan to continue holding Paychex in our Conservative Retirees portfolio. The company reports earnings on Wednesday and can share its outlook on how it's prepared for a wide range of labor market scenarios to unfold.

From unprecedented unemployment claims to a temporary suspension of withholding taxes, Paychex faces some short-term uncertainty but we believe its dividend and long-term outlook remain intact.