Oil Price Shock Expected to Pressure Shell's Balance Sheet

Oil prices plunged as much as 30% last weekend as Saudi Arabia and Russia engaged in a price war that threatens to take market share from higher-cost U.S. shale producers.

We analyzed this event in a note here, but the bottom line is that we believe oil prices could now remain at historically weak levels (i.e. $35 per barrel or lower) for at least a few quarters, if not for more than a year.

If such an environment persists, then Royal Dutch Shell (RDS.B) seems likely to struggle to both improve its balance sheet and continue its streak of paying uninterrupted dividends as it has since World War II.

In light of this development, we are downgrading Shell's Dividend Safety Score from Safe to Borderline Safe.

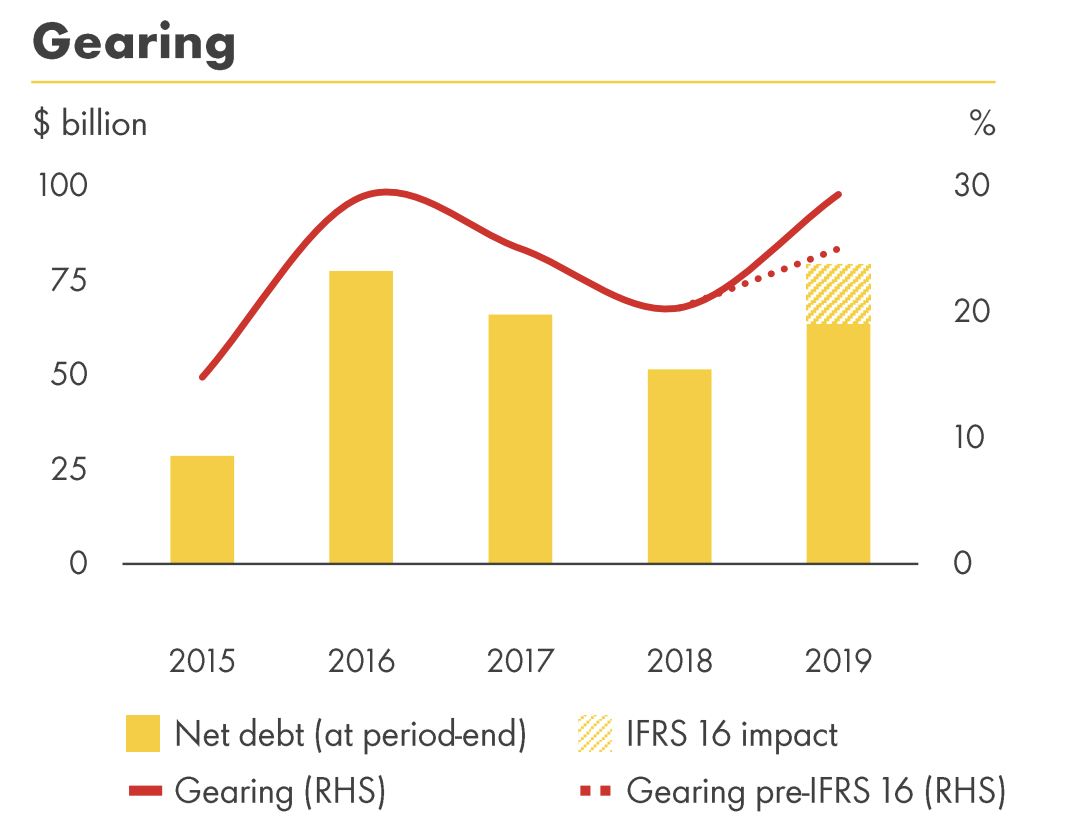

Leading up to the 2014-16 oil crash, Shell maintained a very strong financial profile. By the company's measurement, its net debt to capital ratio, or gearing, was 12.3% at the end of 2014.

Gearing measures the proportion of a company's financing that is from debt (net of cash) rather than equity. Shell's target gearing range through a cycle is 15% to 25%.

The company's gearing spiked to 29.6% in 2016 following its $53 billion acquisition of liquefied natural gas producer BG Group. Despite some progress reducing debt in the years that followed, Shell's gearing remained high at 29.3% at the end of 2019.

Source: Shell Earnings Presentation

For comparison, Chevron (CVX) and Exxon Mobil (XOM) maintain gearing levels below 20%, providing them with greater flexibility to borrow during downturns.

Shell's lack of balance sheet flexibility is concerning given that the company's breakeven point to cover its capital expenditures and dividends requires an oil price above $60 per barrel.

For example, in the fourth quarter of 2019 when Brent oil averaged $62 per barrel, Shell generated $3.9 billion of organic free cash flow, just barely covering its $3.7 billion quarterly dividend.

In May 2019, Shell's management said that for every $10 in oil price movement, the company would lose $6 billion of cash flow.

Therefore, if $35 per barrel oil is the new normal for at least the year ahead ($25 per barrel below the firm's breakeven point), then Shell could need to borrow $15 billion to continue funding its capital expenditures and dividend, all else equal.

This would increase the company's net debt from $79.1 billion to $94.1 billion, raising its gearing from 29.3% to 33.1% (every $20 billion of incremental borrowing raises gearing by 5%).

Shell's AA- credit rating could face pressure in that scenario, and management has said that the firm is committed to protecting its rating and deleveraging its balance sheet to bring gearing down to 25%.

Returning to 25% gearing from 2019's level would require a $15 billion reduction in Shell's net debt. The company can't get their organically in a $35 per barrel oil environment and will instead be swimming the other way.

Shell had hoped to deliver more than $10 billion of asset divestments across 2019 and 2020 to help its balance sheet, but that target seems increasingly unrealistic given the market's lack of appetite for energy assets.

Management appears to have relatively few other levers to pull. Shell has stated that its annual sustaining capex totals $20 billion, which is only a few billion below last year's total investment. In other words, the company doesn't have much discretionary spending it can reduce to really move the capital preservation needle.

Simply put, Shell faces a tough decision if oil prices remain depressed for the foreseeable future. The company may have to decide between lowering its sacrosanct dividend or risking its credit rating by stretching its balance sheet even further while hoping for better market conditions sooner rather than later.

Shell's dividend has been a safe bet for more than 70 years, but this time could be different, depending on how conservative management wants to be given the uncertainty facing the energy market.