GE's Dividend Safety Score Upgraded to Borderline Safe on Turnaround Progress

We are upgrading General Electric's (GE) Dividend Safety Score from Unsafe to Borderline Safe following continued improvement in the firm's cash flow generation and deleveraging progress.

In early 2019, GE believed its core industrial operations might burn through as much as $2 billion as the company's turnaround took time to gain momentum.

The company's money-losing Power division (about 20% of revenue), which builds turbines used by natural gas- and coal-fired power plants to generate electricity, was a primary culprit.

Aside from excess industry capacity and the ongoing shift from fossil fuels to renewables,, this business was hurt by years of mismanagement as GE chased unprofitable deals that were now working their way through the backlog.

CEO Larry Culp, who was appointed to the top job in October 2018, returned the power business to profitability in 2019 by taking out fixed costs and refocusing the sales team on margins rather than volume.

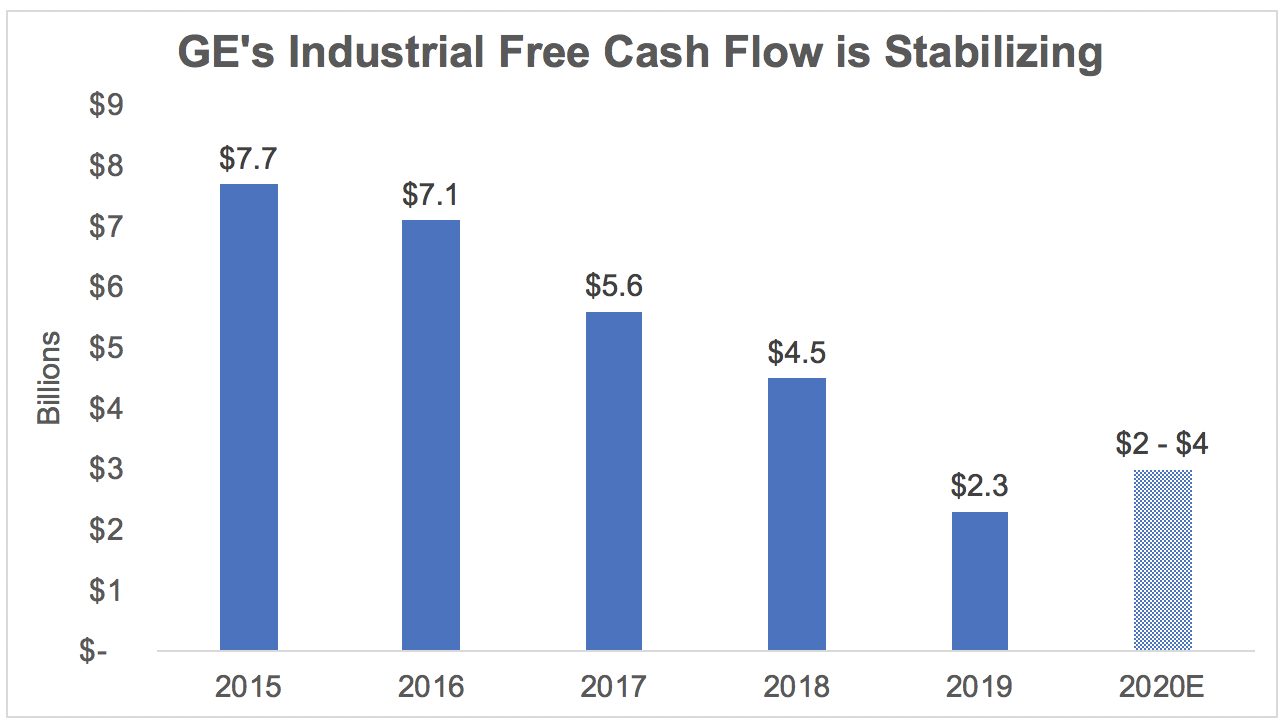

Thanks in part to these restructuring benefits and healthier end markets elsewhere, GE delivered $2.3 billion in industrial free cash flow in 2019 and expects to generate $2 billion to $4 billion in free cash flow in 2020.

The wide guidance range is largely due to the timing of when Boeing's 737 MAX returns to service, which affects demand for the engines produced by GE's high-margin aviation segment. Regardless, 2020 will hopefully prove to be a much needed year of stabilization for the company after years of falling cash flow.

Source: Simply Safe Dividends

For context, GE's dividend, which has been cut twice since 2017, consumes about $350 million annually. Based on 2020 cash flow guidance, GE's payout ratio should sit below 20% this year, leaving about $1.6 billion to $3.7 billion of free cash flow available after paying dividends.

This is a meaningful improvement from past years. Before right-sizing its payout in 2017, GE's industrial free cash flow didn't cover the firm's roughly $8 billion dividend commitment. To fill the gap, the firm relied on (shrinking) dividends from GE Capital, its financial services arm, which was selling off assets.

Going forward, a free cash flow payout ratio around 10% to 20% may sound like a comfortable margin of safety, but GE still isn't retaining much cash flow compared to the mountain of liabilities on its balance sheet.

The company ended last quarter with over $60 billion in industrial debt, more than $20 billion in unfunded pension liabilities, and multibillion-dollar liabilities related to legacy insurance operations. With a risky leverage ratio above 4x, paying down debt remains a top priority.

After all, some struggling companies with dividends well covered by cash flow have still reduced or suspended their payouts to accelerate deleveraging efforts. This was a key factor weighing on GE's Dividend Safety Score.

Fortunately, that scenario appears increasingly unlikely for GE as the firm continues progressing on its turnaround and has plans in motion to significantly reduce its debt this year.

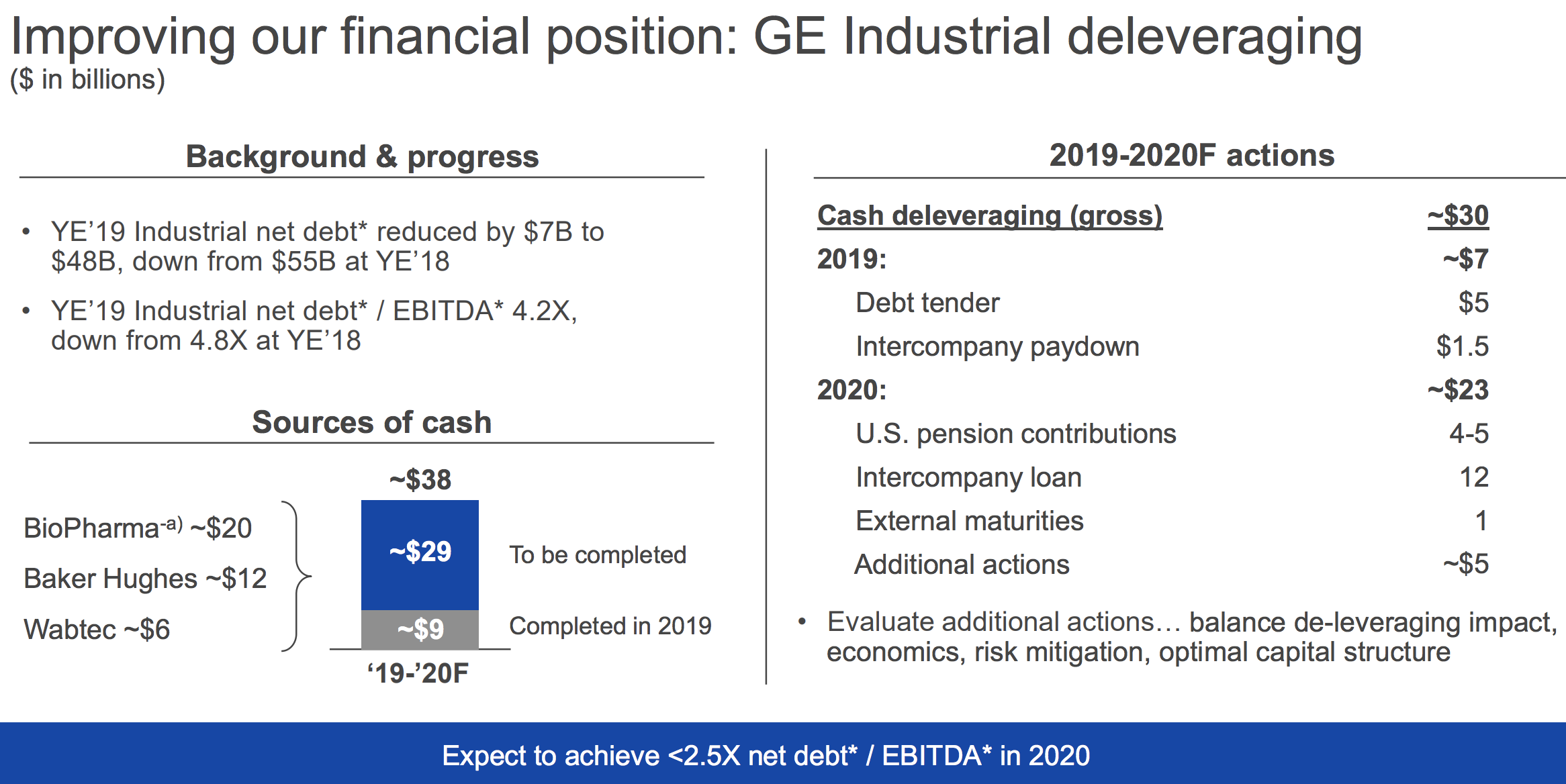

In 2019, GE's industrial business reduced its net debt to EBITDA leverage ratio to 4.2x from 4.8x in 2018. Leverage is expected to reach a much healthier level below 2.5x in 2020, driven by GE's sale of its biopharma assets to Danaher in early 2020 which will deliver net proceeds of $20 billion.

Source: General Electric Earnings Presentation

Meanwhile, GE holds nearly $18 billion in industrial cash and has access to $35 billion in bank lines. The company's liquidity looks healthy and supportive of its dividend.

Of course, with a measly 0.3% dividend yield following steep dividend cuts in late 2017 and 2018, GE shares aren't held by many investors for the income. All eyes are on Mr. Culp's ability to reverse the company's fortunes and get the stock price moving higher.

On that front, 2019 was a step in the right direction. Cash flow improved. Debt fell. The power business showed signs of stabilization. Aviation and healthcare (60% of revenue, nearly all of GE's profits) remained strong franchises.

Downside risk is receding, but GE remains an incredibly complex business with many moving parts, including its murky financial services arm and a culture that will take time to change.

Contrarian investors will need to remain patient and should understand that meaningful dividend growth is unlikely for the foreseeable future at this stage in the turnaround.

.png)