Gap's Dividend Safety Score Downgraded to Unsafe on Operating Challenges, Upcoming Spinoff

In February 2019, Gap (GPS) announced plans to separate into two publicly traded companies in 2020, hoping to unlock value from its faster-growing Old Navy brand. Since then, the apparel retailer's performance has deteriorated, and Gap's CEO unexpectedly resigned in November.

As a result of the company's persistent performance challenges and weakening fundamentals, the risk of Gap cutting its dividend next year as part of its separation plans has increased. As a result, we are downgrading Gap's Dividend Safety Score from a low Borderline Safe rating to Unsafe.

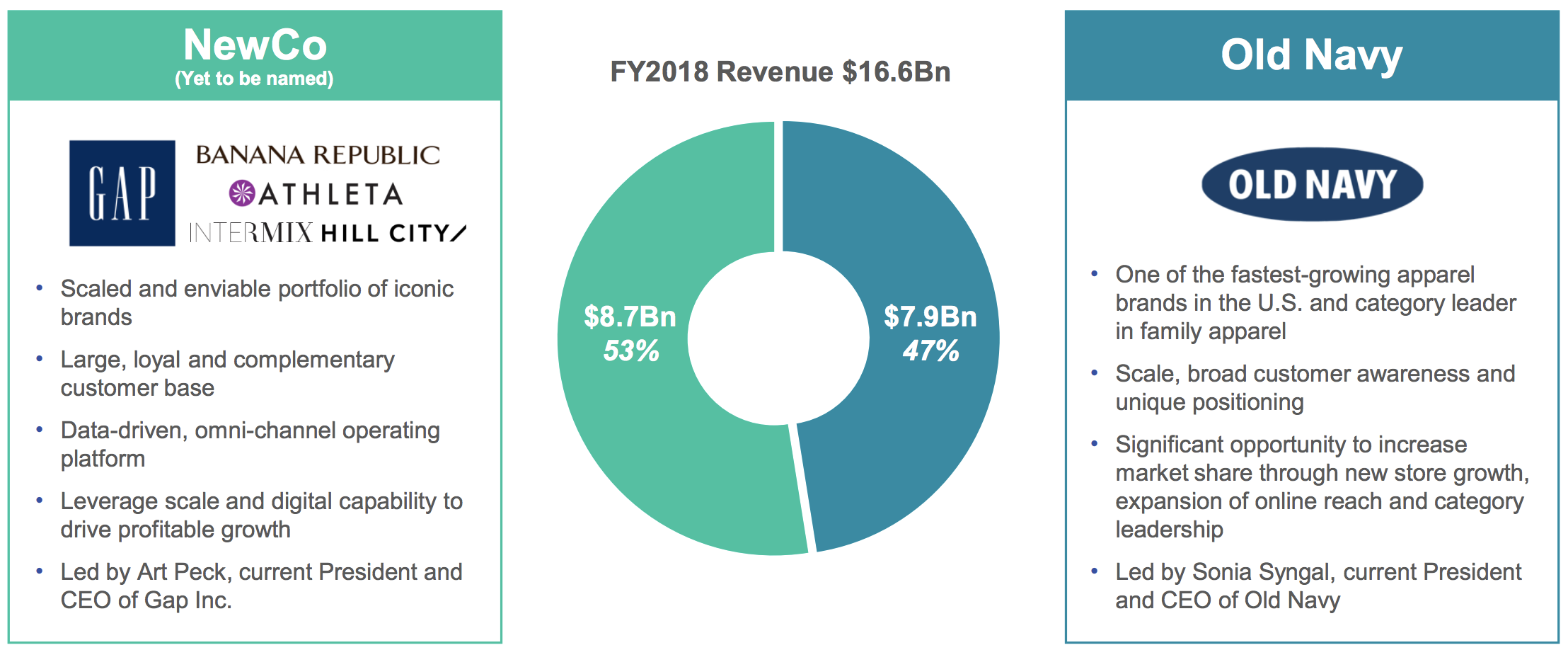

Gap's business consists of more than 3,000 company-owned apparel stores, and about half of its revenue is generated by its Old Navy brand. While Gap's revenue has shrunk by 25% since fiscal 2005 and management is closing stores, Old Navy has delivered more consistent growth and has potential to nearly double its footprint, according to management.

Source: Gap Investor Presentation

Gap believes that by separating these two companies, the market will reward Old Navy with a higher valuation. Management also justified Gap's spinoff plans by citing the diverging priorities of each brand (Old Navy is more focused on the value space) and the increased organizational complexity that built up over time and caused operational inefficiencies.

Investors were initially excited by Gap's separation plans. However, a combination of poor execution, weak mall traffic, fashion misses, and growing competition from fast fashion and off-price retailers has pressured same-store sales across Gap's core brands.

Even Old Navy is on pace of its first same-store sales decline in the last five years, likely hurting the brand's standalone value which was a key driver behind Gap's separation plans.

Source: Gap, Simply Safe Dividends

Further complicating the picture, Gap's CEO Art Peck, who helped orchestrate the separation plan and was expected to lead the remaining company, stepped down in November.

Despite these challenges, management plans to move forward with the Old Navy spinoff next year, and the separation won't come cheap.

Management expects separation expenses and capital costs to total nearly $1 billion. For perspective, that's more than the total net income Gap is expected to generate next year, according to analysts.

While Gap holds about $1.1 billion in cash on its balance sheet, the company has a junk credit rating. The firm's earnings are also under pressure due to Gap's falling same-store sales, high fixed costs, and need to discount more merchandise.

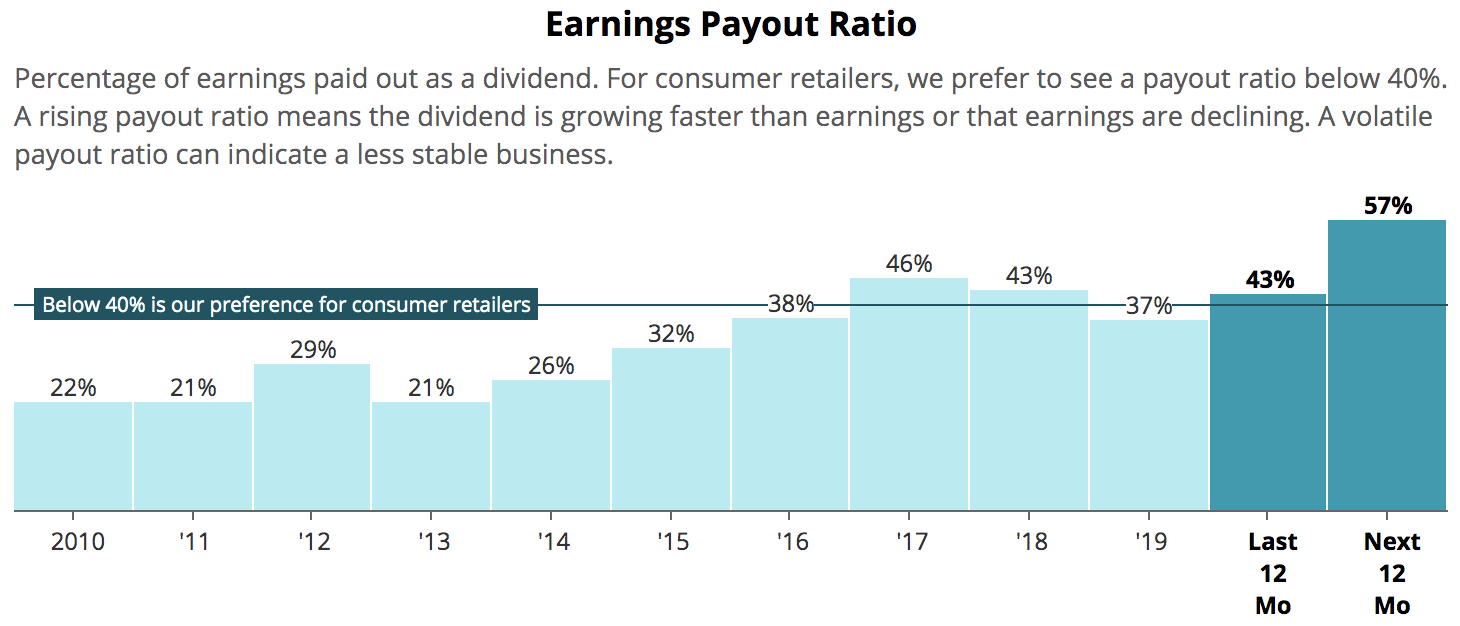

As a result, next year Gap's payout ratio is expected to hit its highest level in more than a decade.

Source: Simply Safe Dividends

Making matters worse, each separate company will incur higher ongoing costs since they no longer can share logistics infrastructure, technology systems, headquarters locations, and other expenses.

Gap expects "gross dissynergies" in the $150 million to $175 million range for Old Navy and $225 million to $250 million for Gap, or about 2% to 2.5% of revenue. For a business that has a single-digit profit margin already, that's significant.

Gap plans to implement mitigating actions to reduce dissynergies by about half, but the company's ongoing profitability would still face about a $200 million annual headwind going forward.

Analysts expect Gap to generate approximately $650 million in profits next year, and the current dividend consumes roughly $370 million annually. Simply put, after accounting for net dissynergies, the business seems like it will be challenged to keep income investors whole when the two companies separate.

Management hasn't made any specific comments about each separate company's dividend plans. In September 2019, Gap CFO Teri List-Stoll only acknowledged that both companies will evaluate their capital allocation plans, which will likely include dividends:

"Our primary use of cash is to invest in the business for growth. But we have a long history of providing a return of cash through a combination of dividends and share repurchase. And we would expect that to continue frankly for both companies. And the question is what is the right mix. What is the right mix of cash return that appeals to the target investors? And what is the right level initially on a going basis that fits the strategic priorities of each business? So more to come on that."

Old Navy generates the bulk of Gap's current profits and will likely want a lower payout ratio to help fund its long-term growth plans, which include expanding its locations from about 1,200 stores to 2,000.

Meanwhile, Gap plans to close nearly 20% of its locations by the end of 2020 at a cash cost of $250 million to $300 million (about 3% of standalone sales) as its business remains under pressure and in need of improving its weak profitability. That's not exactly a position of strength from which to pay generous and sustainable dividends.

Overall, Gap does not appear to be a reliable income investment, and it appears increasingly likely that management will use the mid-2020 separation to reduce the company's dividend.

Apparel retail is a ruthlessly competitive and fast-changing industry that conservative income investors are best off avoiding. Gap does not appear to hold any differentiated assets that can move the needle, especially as its mall-based Gap and Banana Republic concepts (about 50% of total sales) continue facing secular headwinds and competition from fast fashion and off-price retail grows.