PPL's Rumored Merger with Avangrid Provides Interesting Potential

PPL (PPL) is in discussions to merge with Avangrid (AGR), according to The Financial Times. Neither company has publicly confirmed the rumors, and it's possible no deal is reached. However, a marriage of these two utilities could unlock some benefits for PPL shareholders.

We've held shares of PPL in our Conservative Retirees portfolio since July 2015, but I've had the stock under review for potential sale for most of this year due to PPL's outsized exposure to the United Kingdom (U.K.).

The U.K. accounted for just over half of PPL's 2018 earnings. Besides Brexit-related political instability and currency volatility, my main concern is the profitability of PPL's core electricity distribution operations.

This business seems likely to be challenged by U.K. regulators beginning in 2023, when the current regulatory framework for electricity distribution ends. More will be known about regulators' intentions next year when discussions for the new framework become more serious.

PPL's dividend continues to look safe for now and its valuation appears undemanding, so I've not been in a hurry to find a replacement. Rumors of a potential merger with Avangrid further reduce my urgency to replace PPL, and I'm willing to wait to see if a deal shakes out.

Combining with Avangrid would reduce PPL's U.K exposure and potentially provide a path for the company to shed this business completely, removing an overhang on the stock. Avangrid's business has several other appeals, too.

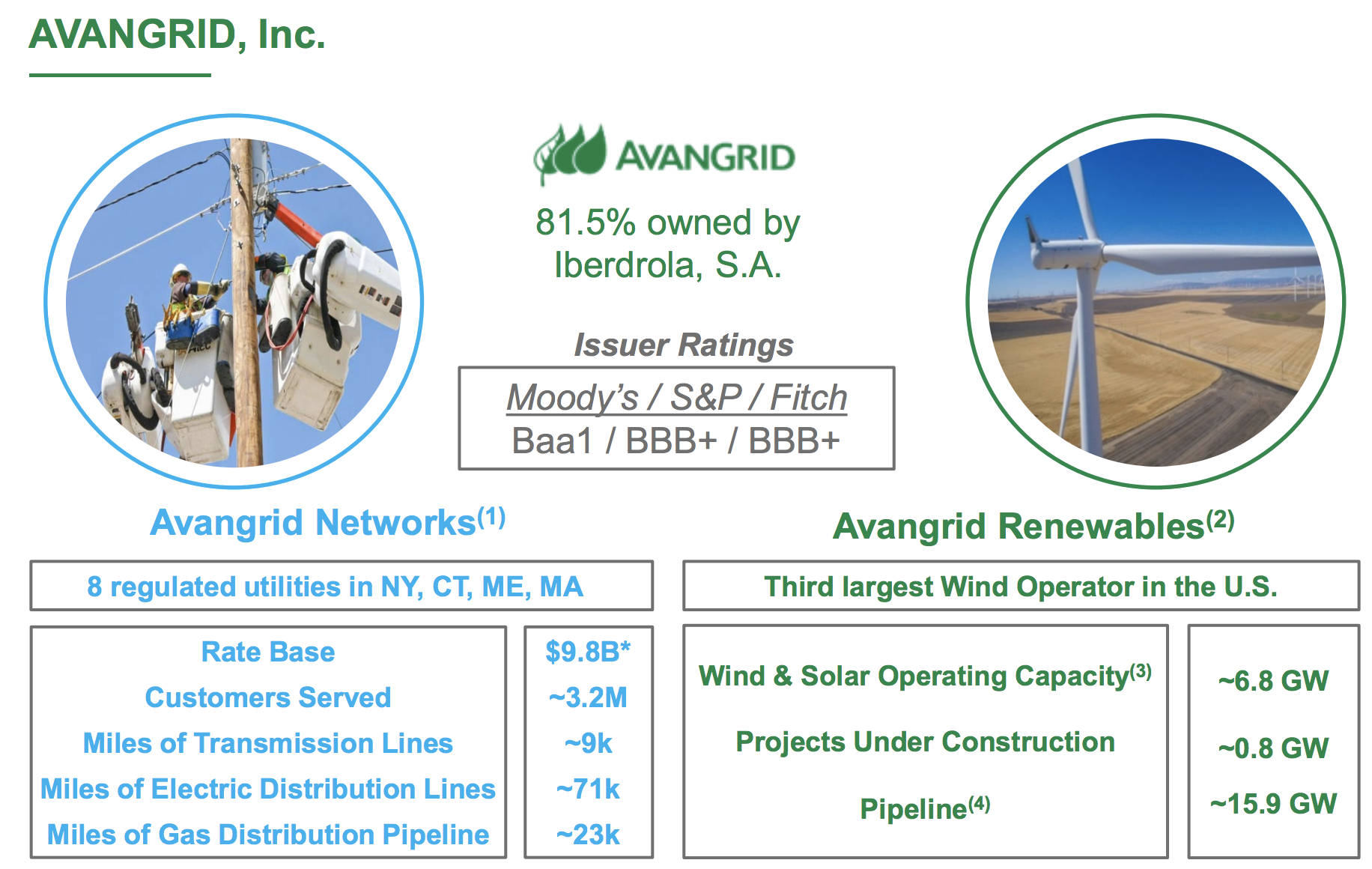

Avangrid is a U.S. utility with a mix of regulated operations and renewables businesses focused primarily on wind. Regulated utilities generate about 70% of Avangrid's adjusted net income, with renewables contributing the remaining 30%.

The firm's regulated utilities deliver natural gas and electricity to customers in New York, Maine, Connecticut, and Massachusetts.

Avangrid is also the third largest wind operator in America. While this business is unregulated and can be affected by weather, over 70% of the company's capacity is under long-term contracts with other utilities, reducing market risk.

Source: Avangrid Investor Presentation

Importantly, Iberdrola (IBDRY), a major utility based in Spain with a market cap nearly three times larger than PPL's, owns 81.5% of Avangrid.

Iberdrola generates close to 20% of its cash flow (EBITDA) from the U.K. and might be interested in combining PPL's U.K. operations with its own, perhaps in the form of a new spin-off. Of course, such a plan would require regulators to give their blessing, which may be unlikely.

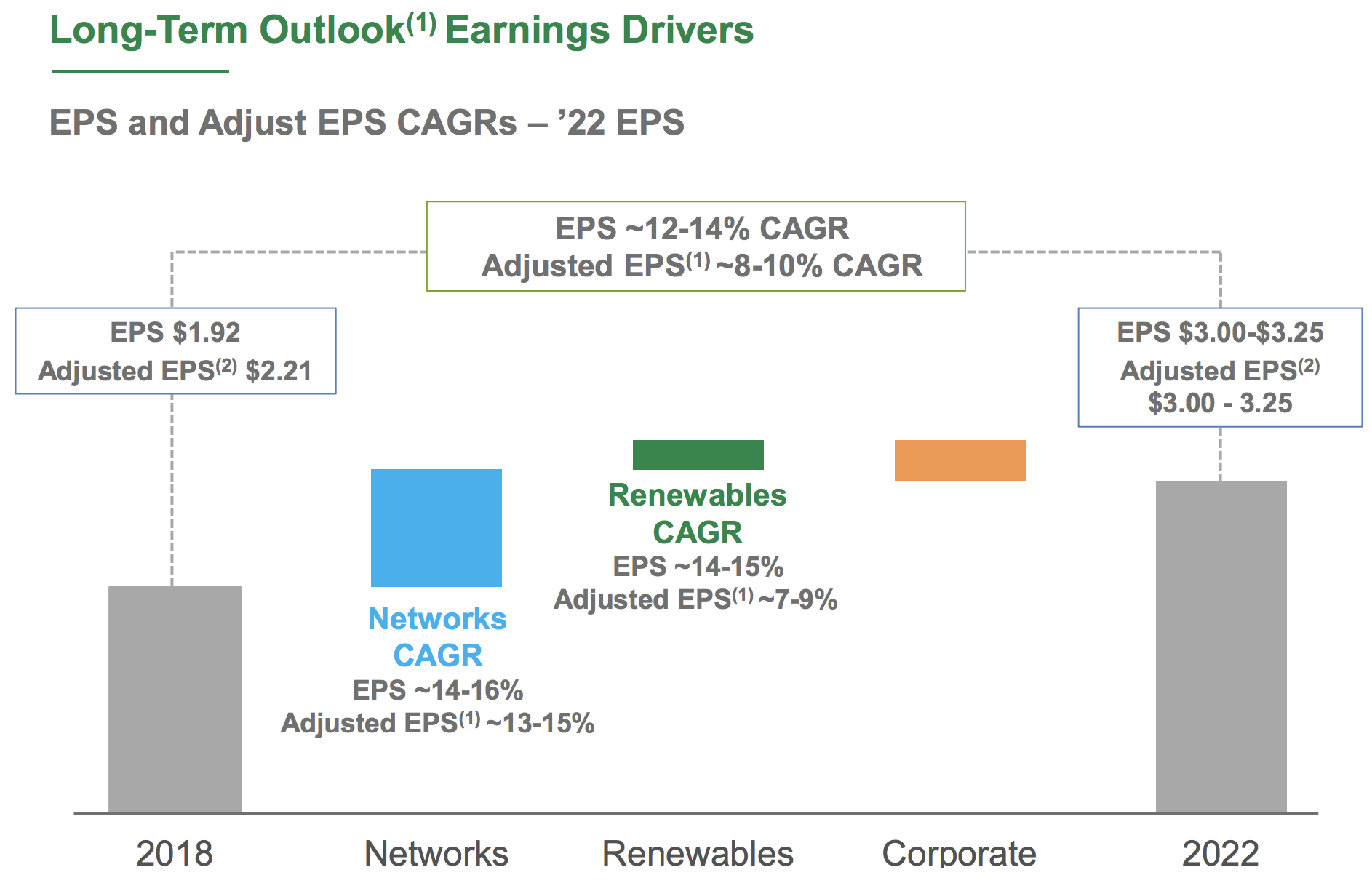

However, if successful, this would leave the PPL-Avangrid entity as an all-U.S. business with healthy exposure to renewables and predictable growth. In fact, Avangrid targets 8-10% adjusted EPS growth from 2018-22, and PPL's earnings are expected to grow at a mid-single digit pace, according to management.

Source: Avangrid Investor Presentation

Iberdrola is also investing aggressively in renewables, which account for over 20% of its cash flow. It's possible Iberdrola would feel more incentive to invest in a larger PPL-Avangrid company to help the utility's clean energy operations grow even faster.

From a financial perspective, Avangrid has an investment-grade credit rating (BBB+ from Standard & Poor's), the backing of a majority owner with deep pockets (Iberdrola), and a reasonable 65-75% dividend payout ratio target.

Avangrid's earnings are somewhat more volatile due to its mix of unregulated renewables, but this also provides the firm with an attractive long-term growth driver as the utility industry evolves.

Overall, barring a major spin-off to unlock value and shed exposure to the U.K., I would expect the combined company to maintain a safe dividend in the event of a merger.

In light of this emerging development, I plan to continue holding our shares of PPL until we know if anything comes from these rumors. Given PPL's undemanding valuation (5+% dividend yield) and potential synergies with Avangrid and Iberdrola's U.K. operations, I'm willing to remain patient.