Prospect Capital's Dividend Safety Score Downgraded to Unsafe on Investment Performance Risks

Prospect Capital (PSEC) is one of the largest and oldest business development companies, or BDCs.

All BDCs are basically middle market lenders, which means they lend to or take equity stakes in the 200,000 or so subprime businesses that generate about a third of the U.S. economy.

Essentially, BDCs serve a market of small companies across the country that regular banks don’t want to touch, helping those businesses fund acquisitions, leveraged buyout transactions, recapitalizations, and growth projects.

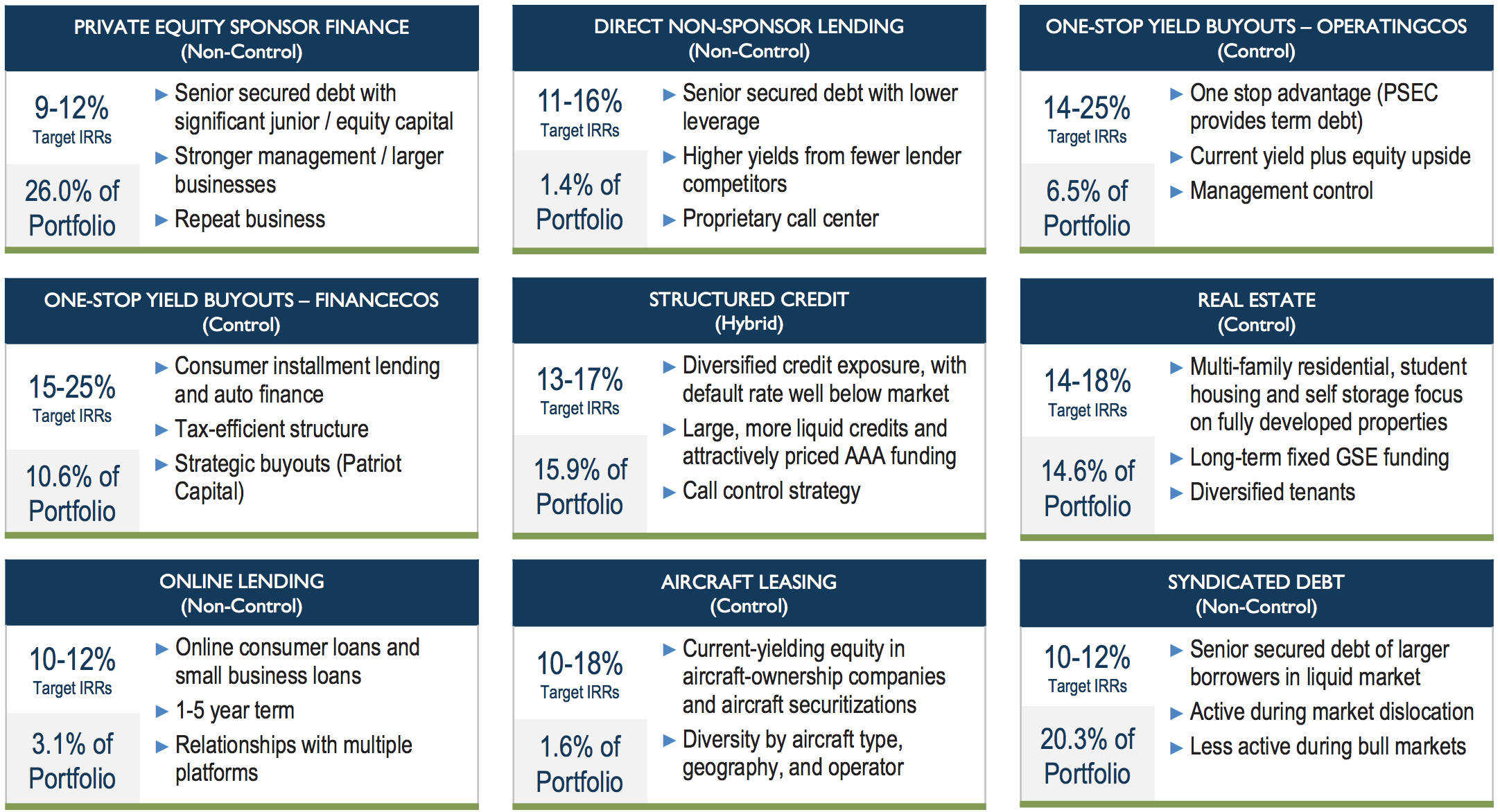

Prospect Capital's portfolio includes more than 130 investments across nearly 40 industries and nine different investment strategies. The portfolio's annualized yield exceeds 10%, reflecting its higher risk profile.

Source: Prospect Capital Investor Presentation

BDCs are able to dole out large dividends when their portfolio companies are healthy enough to make their interest payments and repay principal.

However, given the more speculative nature of the companies they invest in, plus their high payout ratios and use of leverage to magnify returns, it doesn't take much for many of their dividends to end up on the chopping block.

Prospect Capital is no exception, and we are downgrading the firm's Dividend Safety Score from Borderline Safe to Unsafe, reflecting its rising payout ratio and struggling investment performance.

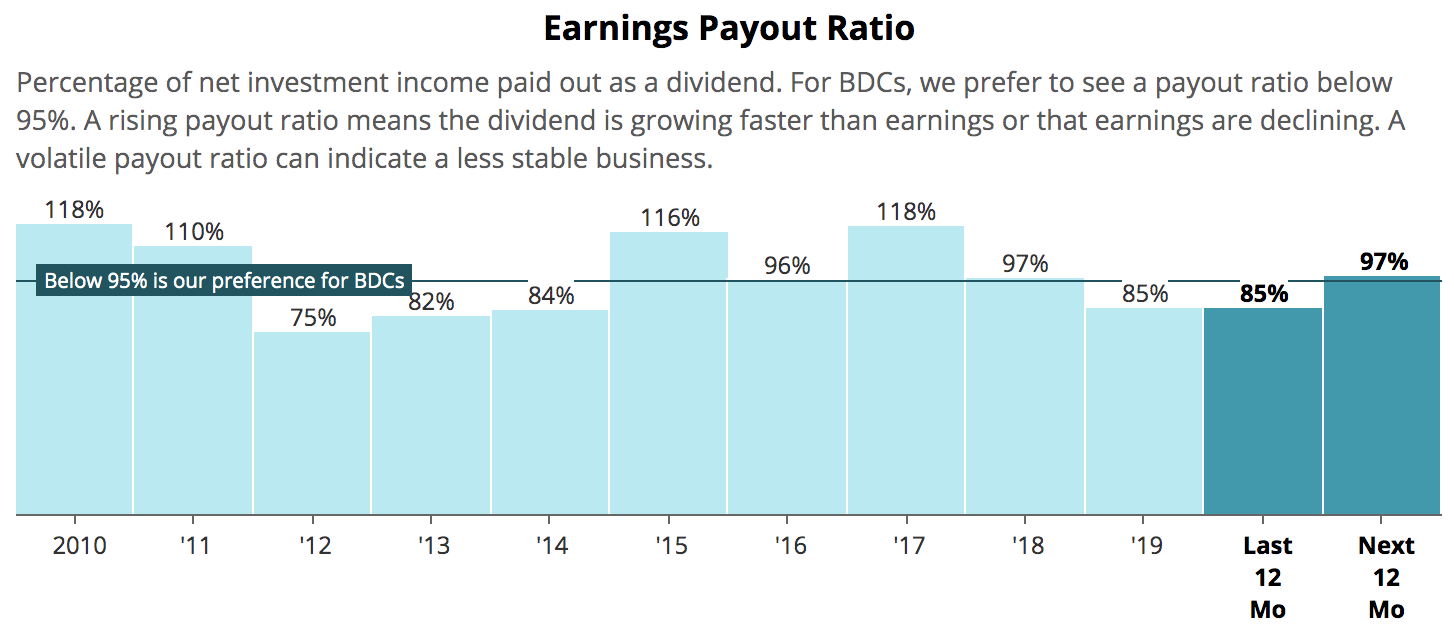

As you can see, Prospect Capital's payout ratio is expected to reach 97% over the next 12 months. Analysts expect the firm's earnings per share to fall more than 10%, driven by rising investment portfolio risk.

Source: Simply Safe Dividends

The firm may not cut its dividend as long as its payout ratio remains below 100%, but you can see that Prospect Capital's historical coverage has been volatile. All it takes is a couple of bad investments for the dividend to no longer be covered by net investment income, and the company has little wiggle room today.

Standard & Poor's also has concerns. On September 16, the ratings agency revised its outlook on Prospect Capital from stable to negative, threatening Prospect Capital's investment grade credit rating (BBB-).

S&P cited "the risk of increasing losses in PSEC's investment portfolio, reflecting an elevated level of loans at cost on nonaccrual status, investment concentration within its top five positions, and holdings of subordinated structured notes."

Even if its investment performance stabilizes and the dividend is maintained for now, Prospect Capital looks like a low quality BDC that conservative investors should avoid.

Despite its relatively large size for a BDC, the company employs an external management team. Under this arrangement, Prospect Capital pays hefty fees to an outside investment advisor, Prospect Capital Management L.P., to run its business.

Under this agreement, Prospect Capital pays its external investment advisor a base management fee calculated at an annual rate of 2% on its total assets, and an incentive fee which includes 20% of the firm's realized capital gains each year.

Just how significant are these fees? In fiscal 2019 Prospect Capital paid about $200 million in management fees while generating $704 million in total investment income.

Externally managed BDCs like Prospect Capital have higher costs, which requires them to reach further for yield in order to cover their dividends. This often means lending to riskier, often distressed companies or getting involved in more complex investments.

Worse, the firm's investment advisor is highly incentivized to grow Prospect Capital's asset base at any cost, since that drives the 2% base management fee. It doesn't matter how well the investments perform as long as the company's asset base continues rising.

Debt and cash that's not yet invested are even included in Prospect Capital's asset calculations. Management can sell new shares and take on extra debt to grow its fees, even if the resulting shareholder dilution destroys investor value over time.

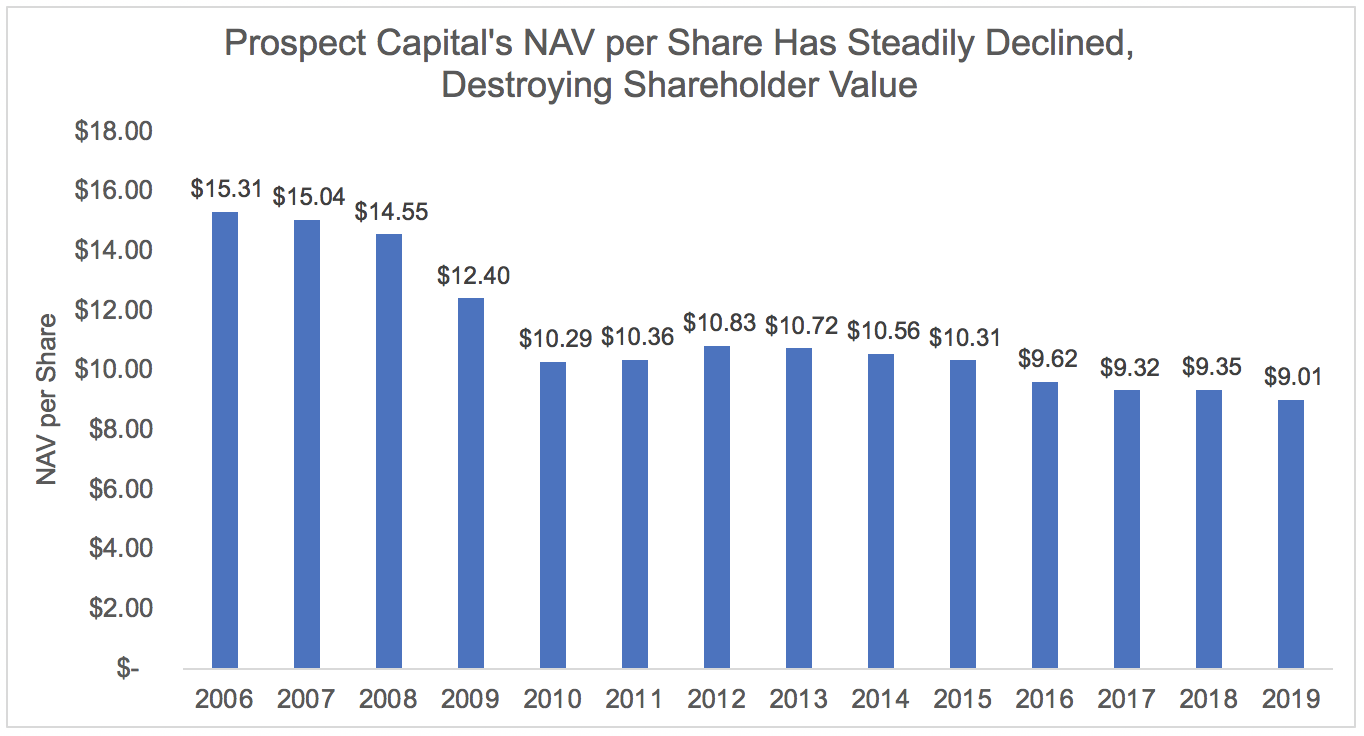

Prospect Capital has done this for years, with the resulting dilution and excessive management fees causing a steady decline in the firm's net asset value (NAV) per share. NAV takes a firm's total assets and subtracts out its liabilities, effectively representing the net worth of the company.

Source: Simply Safe Dividends, Company Filings

Prospect Capital's current share price ($6.65) is well below its NAV per share of $9.01, preventing its ability to grow by issuing equity without diluting shareholders. The stock's discount to NAV likely reflects worries about the BDC's excessive management fees and the quality of its assets.

Prospect Capital has come under pressure in the past over how some of its illiquid investments are valued on its books. The firm's portfolio also appears to consist of riskier investments compared to the average BDC.

For example, approximately 44% of Prospect Capital's earning assets were from first lien secured loans (first to be paid when a borrower defaults), which S&P notes is "a low percentage compared to most peers."

The company also owns a significant amount (about 16% of its portfolio) of collateralized loan obligations, or CLOs.

A CLO investment is typically diversified across 100 to 200 loans and consists of various tranches investors such as Prospect Capital can buy. The most senior tranche is paid off first, with credit losses being absorbed from the lowest rung.

Prospect Capital often takes a significant position in the subordinated interests and debt of CLOs, making some of these investments "riskier and less transparent" than the direct investments it makes in underlying companies (not to mention harder to value), according to the firm's 10-K.

The bottom line is that Prospect Capital's investment portfolio carries meaningful risk, especially over a full economic cycle. The firm's earnings and NAV will likely have higher volatility than its peers who invest more of their portfolios in secured first lien debt.

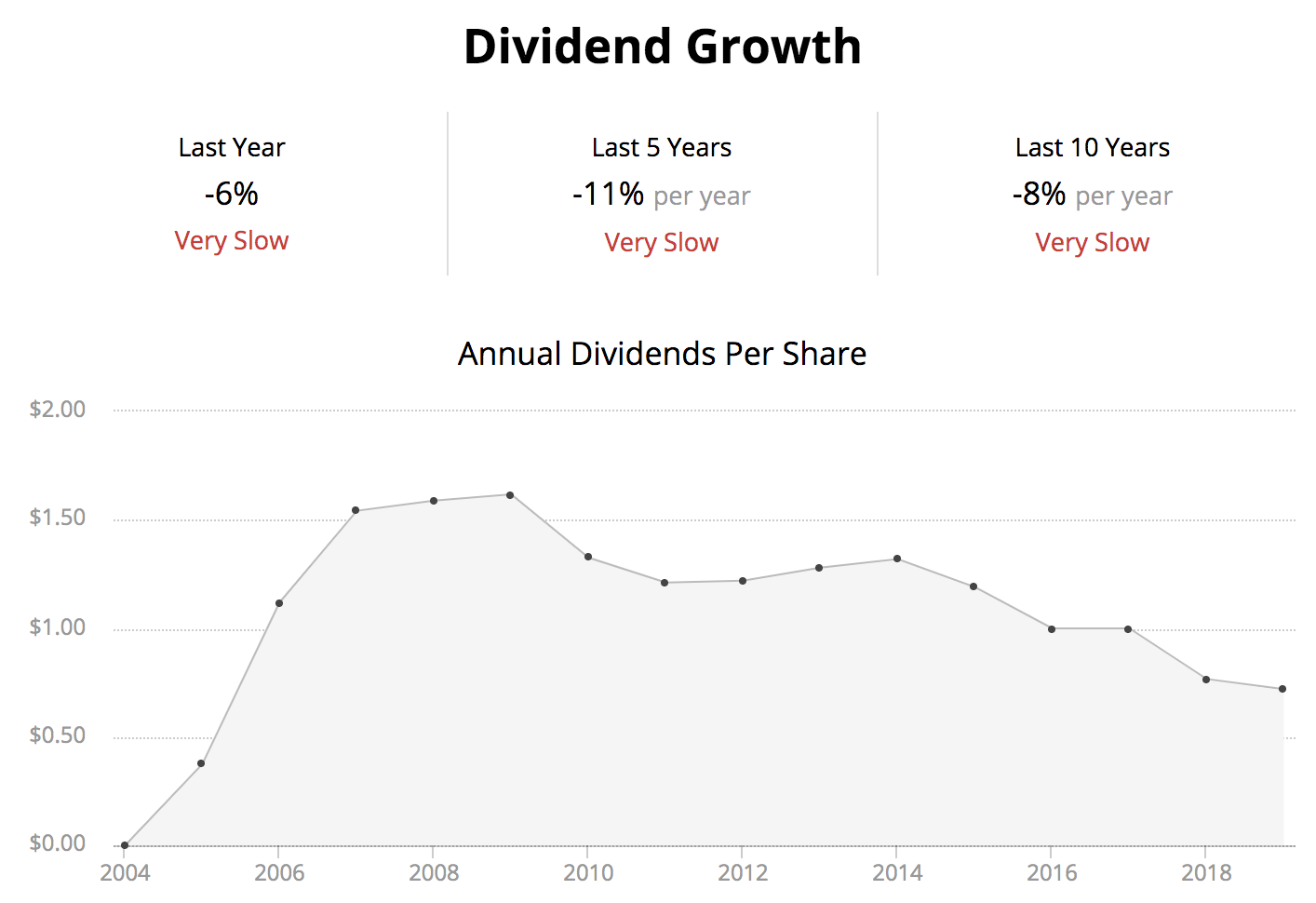

Combined with substantial management fees and dilution over the years, Prospect Capital has been no stranger to dividend cuts. In fact, over the last 10 years Prospect Capital's dividend per share has declined by 8% annually.

Source: Simply Safe Dividends

Prospect Capital's stock performance has been equally disappointing. The S&P 500 has roughly doubled PSEC's total return since the firm went public in 2004. Over the last five years, the S&P 500 has nearly tripled Prospect Capital's total return.

Overall, Prospect Capital appears to be a speculative dividend stock, and one that will likely perform poorly during the next recession. While the double-digit dividend yield may look tempting, continued erosion of the dividend over the long term seems probable due to the firm's business model and investment risks.