Altria's Dividend Safety Score Downgraded to Borderline Safe on Increased Merger Uncertainty

Increasing regulatory headwinds in recent weeks have clouded the long-term outlook for part of Altria's (MO) business.

These issues appear unlikely to threaten Altria's dividend assuming the company remains independent. However, they have created greater uncertainty about the terms Altria would receive if management decides to push forward with a merger with Philip Morris (PM).

Due to this uncertainty, which has potential to result in a moderate (10-15%) dividend reduction for Altria shareholders if a merger takes place, Altria's Dividend Safety Score is downgraded to Borderline Safe until more clarity is provided.

We plan to continue holding our Altria shares in our Top 20 Dividend Stocks portfolio and expect more information on a potential merger to be known within the next quarter or two.

Let's review the latest events and how they could impact income investors.

The business environment seems to get worse for Altria with each passing month. September isn't over yet but it has already delivered several unpleasant developments:

September 11: the Trump administration plans to ban flavored vaping products, citing concerns about health risks and rising use by teens (flavored e-cigarettes account for more than 80% of Juul's U.S. sales)

September 23: Federal prosecutors launch criminal probe of Juul's marketing practices

These headlines have weighed on Altria due to the firm's $12.8 billion investment it made in December 2018 for a 35% stake in vaping leader Juul.

This deal was criticized immediately due to valuation concerns (Juul was valued at about 40 times sales), despite Juul's rapid growth and dominant U.S. market share.

Today Altria's vaping investment is increasingly looking like it could go up in smoke as regulators worldwide clamp down on e-cigarettes.

That's not to say vaping won't still have a future, but the industry's growth prospects over the medium term have taken a big step back as health concerns and rising teen use are addressed.

Your guess is as good as mine regarding the vaping industry's future, but what happens if Altria's investment in Juul is now worthless?

From a financial perspective, there actually seems to be little short-term impact. The money funding the investment is already gone (a sunk cost), and Juul was not expected to contribute meaningful cash flow to Altria for years as it continued reinvesting heavily for growth.

Simply put, Altria's business, funding needs, and deleveraging plans weren't dependent on Juul to be a material earnings contributor anytime soon.

Analysts still expect Altria's earnings per share to grow about 8% over the next year, the company's payout ratio is projected to remain just below management's 80% target, and leverage appears somewhat elevated but still manageable.

Source: Simply Safe Dividends

If Juul's worth goes to $0, I would be surprised if it affected Altria's dividend safety. Yes, the firm has reduced financial flexibility going forward until its balance sheet improves, but Juul wasn't a bet-the-firm investment.

In fact, Altria's $12.8 billion purchase represents only around 12% of the company's enterprise value today (market cap plus debt).

Trends in Altria's core cigarette business will remain the biggest driver of the company's ability to pay its dividend for the foreseeable future.

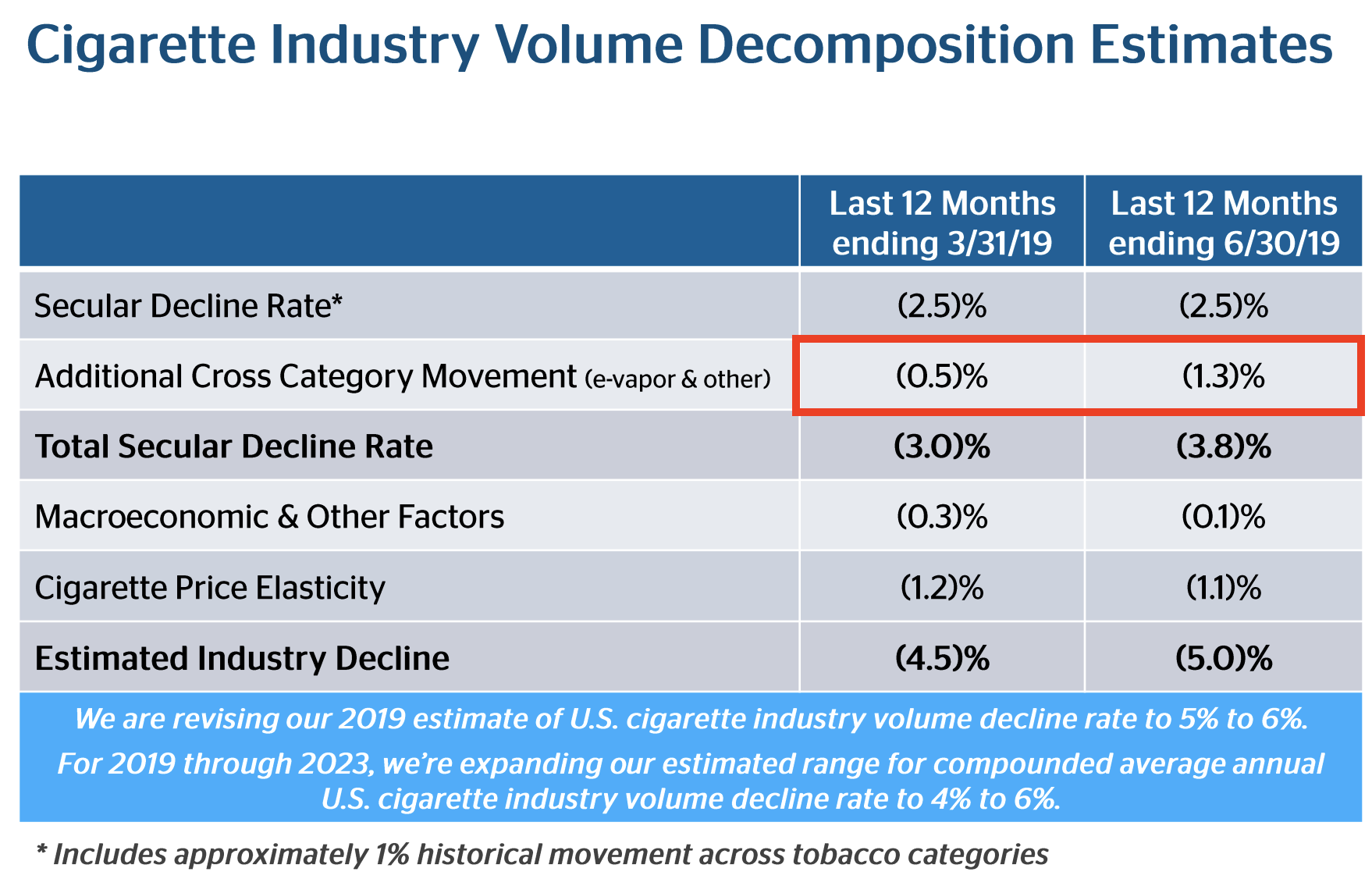

One of the main reasons Altria invested in Juul was because smokers were moving to other categories at an accelerating pace, pressuring cigarette industry volumes.

As you can see, last quarter Altria expanded its estimated range of the U.S. cigarette industry volume decline rate to 4% to 6% "primarily due to increased adult smoker movement to the e-vapor category."

Source: Altria Earnings Presentation

If most U.S. e-vapor products are taken off the market in the next year, it's possible that cigarette volume declines experience a little relief with fewer nicotine alternatives in the market.

That's important since cigarettes generated about 85% of Altria's adjusted operating income through the first six months of the year.

As long as the cigarette industry does not experience another step down in demand, lose its favorable price elasticity, or face new challenges from regulators, it's hard to imagine Altria needing to cut its dividend in response to its elevated debt load from acquiring a stake in Juul.

However, there are two other problems Juul could have caused for Altria besides the $12.8 billion sunk cost and management's weakened credibility.

First, Juul and Altria are subject to numerous lawsuits related to their marketing practices and the detrimental health effects of their e-cigarette devices.

I'm not a legal expert, so it's hard to say how confined these lawsuits are to Juul's corporate entity. Altria is a minority shareholder, no longer sells its own vaping products (has a non-compete with Juul), and notes in its 10-K filing that Juul's "strategy and its material decisions are not controlled by us."

Regardless, Altria is a prime candidate for lawyers to target for a settlement due to the firm's substantial size and vast cash flow. It's too soon to say, but material legal liabilities related to vaping would put more pressure on Altria's balance sheet and the amount of cash flow it has after paying dividends to reduce debt.

If severe enough, these legal obligations could affect Altria's dividend safety profile. We will continue monitoring the situation, which is admittedly murky and could take years to play out.

For now, assuming Altria remains a standalone company and cigarette volume declines trend as management expects, the firm's dividend appears to remain on solid ground.

So why was Altria's Dividend Safety Score downgraded to a Borderline Safe rating?

The latest vaping developments have cast more uncertainty over Altria's worth, threatening the ownership level (and therefore the amount of dividends) shareholders might receive in a possible merger with Philip Morris.

With Juul's value taking a hit in recent weeks, Altria has likely lost some negotiating power with Philip Morris. The two tobacco giants announced they were discussing a "merger of equals" on August 27, but no details were given about the potential ownership split if a deal moves forward.

If Altria's management feels desperate to do a deal and agrees with Philip Morris that Juul is no longer worth as much as it was a month ago, then Altria shareholders face a wider range of outcomes, including some that could result in an effective dividend cut (albeit a moderate one).

Let's look at a few hypothetical merger scenarios. Besides the PM-MO ownership split, there are numerous factors for income investors to consider.

For example, the combined company could decide to:

Maintain Philip Morris's current $4.68 per share dividend,

Set a new target payout ratio and dividend per share amount, or

Maintain the total amount of dividends paid by Altria and Philip Morris today after they combine

Let's start with arguably the worst-case merger scenario for Altria income investors.

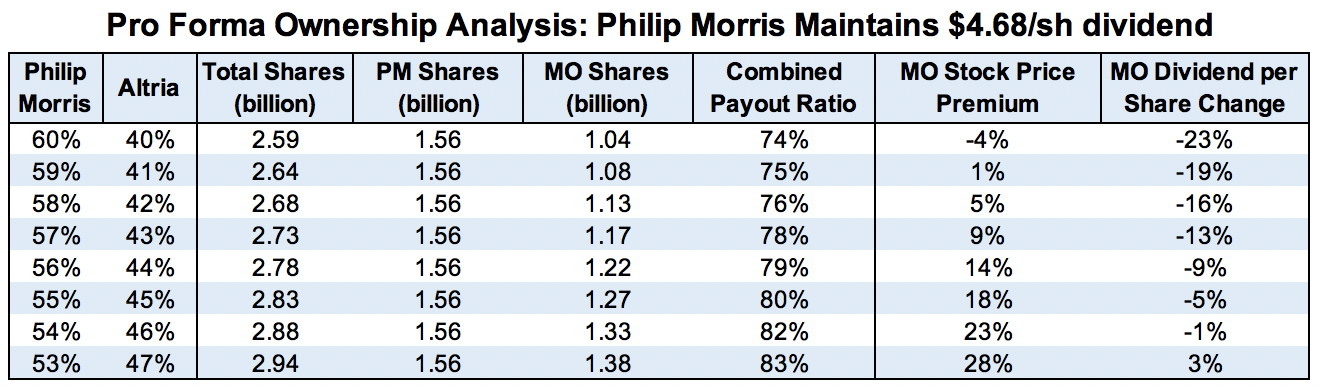

1) Combined company maintains Philip Morris's $4.68 per share dividend In the first scenario, we assume the combined company keeps Philip Morris's current $4.68 per share dividend after the companies merge.

Each row in the table below represents a different ownership split, with Altria's stake ranging from 40% to 47%. (Someone briefed on the initial deal's terms told The Financial Times that Altria would own between 41% and 43% of the combined company.)

Again, if Juul's valuation has taken a hit and Altria wants to continue pursuing a deal, that could pressure the ownership level Altria is able to negotiate, impacting the level of dividends current shareholders would receive if a merger occurs.

Here's a look at the potential outcomes for Altria shareholders based on different ownership splits.

Note that the "MO Stock Price Premium" column represents the acquisition premium over Altria's current stock price. The "MO Dividend per Share Change" column represents the effective change in annual dividend income an Altria shareholder would face if a merger took place at each ownership split level.

Source: Simply Safe Dividends, Company Data

If Altria gets 42% of the combined company, for example, investors would receive just a 5% premium to the current share price.

After shares are exchanged, Altria investors' annual dividend income would decrease by 16%. (MO shareholders receive $3.36 per share today; after the exchange in this scenario, their shares in the new company would pay the equivalent of $2.82 per share.)

In this scenario, the combined company's EPS payout ratio would be 76%, below Altria's 80% target and well below Philip Morris's payout ratio, which has remained between 87% and 92% in each of the last five years.

If Altria's ownership stake approaches 40%, investors could be looking at a zero premium buyout and an effective dividend cut near 20%. However, I can't imagine shareholders accepting such a deal, and the combined company also seems very unlikely to maintain a sub-75% payout ratio given each firm's history.

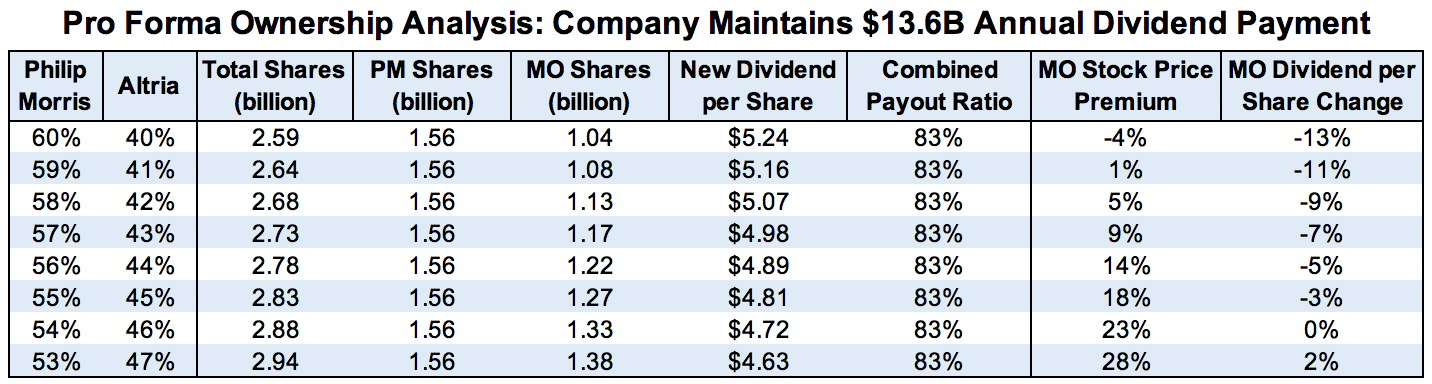

What if the combined company's dividend policy sought to maintain the current dividend dollars paid by each firm instead of matching Philip Morris's per share payout?

2) Combined company maintains $13.6 billion annual dividend payment Factoring in their latest dividend increases, Altria and Philip Morris are currently expected to dole out approximately $6.3 billion and $7.3 billion in annual dividend payments, respectively.

In the event of a merger, perhaps management would want to advertise that the combined company's total payout is unchanged ($13.6 billion).

While that might sound good on the surface, it could once again result in an effective dividend cut for Altria shareholders depending on the ownership level they receive in the new company.

The acquisition premium doesn't change across any of these scenarios, but Altria investors would need to own 46% of the combined company to continue receiving the same amount of dividend payments they enjoy today.

Source: Simply Safe Dividends, Company Data

In this fixed $13.6 billion dividend scenario, the combined company would have a payout ratio of 83%, which seems reasonable. In a worst-case ownership split here, where Altria receives 41% of the new company, shareholders would face an 11% dividend reduction and just a 1% acquisition premium.

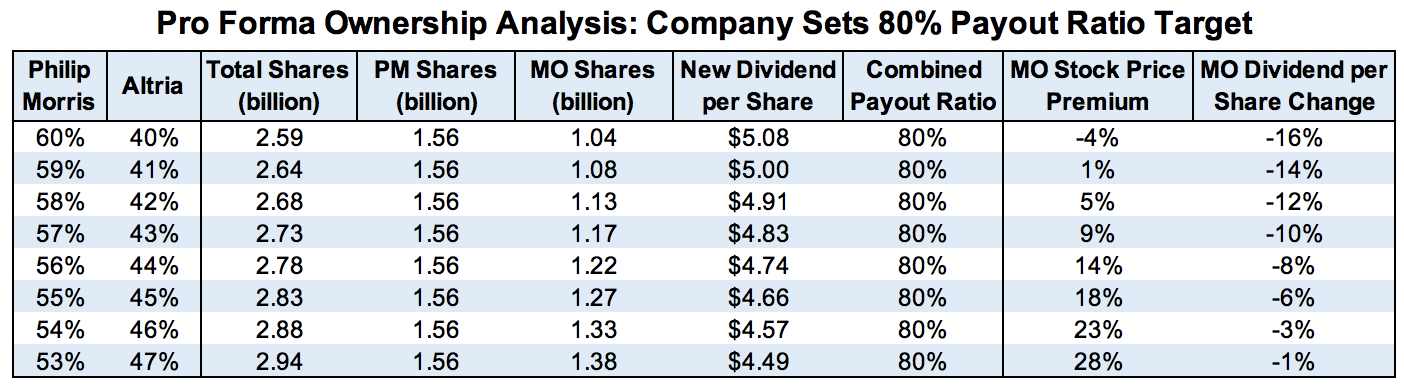

3) The combined company sets an 80% payout ratio target Instead of maintaining Philip Morris's current dividend per share rate or equaling the combined dividend payouts of Altria and Philip Morris, management could install a new payout ratio target.

In this scenario, the combined company declares it will distribute 80% of its adjusted earnings as dividends, providing flexibility for reinvestment and deleveraging purposes. Philip Morris and Altria's combined net income over the year ahead totals $16.5 billion, according to the latest analyst estimates.

An 80% payout ratio would result in total dividends of about $13.2 billion, or 3% less than the $13.6 billion in dividends these firms pay today. The combined company's new dividend per share amount would vary depending on how many shares are issued to Altria investors.

In a deal where Altria investors own 41% of the new company, Altria shareholders would face an effective 14% dividend cut.

Source: Simply Safe Dividends, Company Data

I would be surprised if management implemented this dividend policy since it would represent a decrease in aggregate dividends paid. Philip Morris shareholders would also be at risk of a headline dividend cut if they didn't own at least 58% of the new company.

What if a higher payout ratio is targeted?

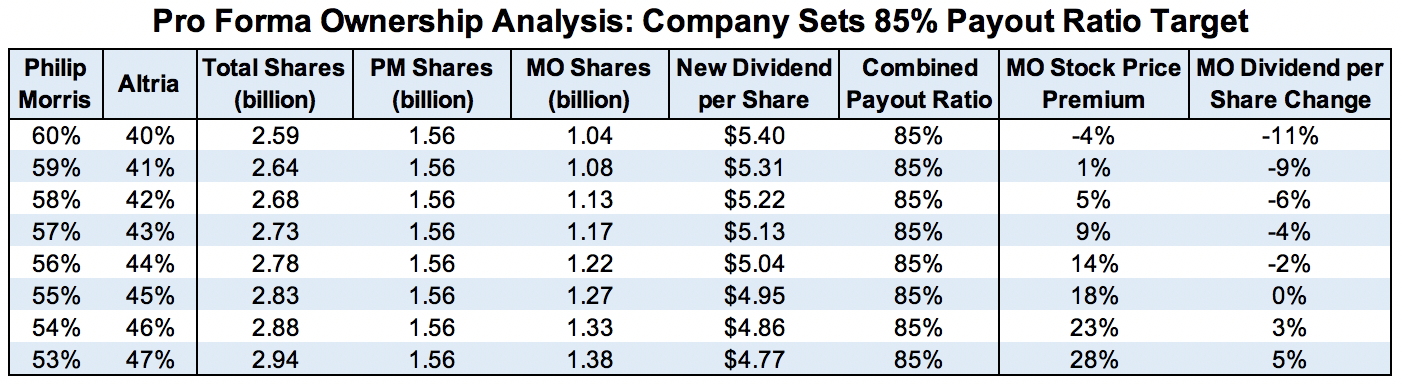

4) The combined company sets an 85% payout ratio target An 85% payout ratio would be above Altria's 80% target but below Philip Morris's historical level near 90%.

The result would be about $14 billion in dividends paid in the year ahead, or 3% more than what Altria and Philip Morris currently pay.

A merger-driven dividend raise seems unlikely, but you can see it helps cushions the dividend cut risk faced by Altria investors.

Even in a worst-case scenario where management agrees to only own 41% of the new company, existing shareholders' dividend income would fall by less than 10%.

Source: Simply Safe Dividends, Company Data

5) More possibilities... So few details are available about a potential merger's terms that this is all speculation for now. But other scenarios exist in the event of a merger.

For example, perhaps Philip Morris and Altria would elect to spin off their non-combustible businesses into an independent company. The spin-off would have potential to achieve a higher valuation without the anchor of declining cigarette volumes.

However, it would also take a chunk of Philip Morris's business with it (nearly 20% of net revenue is from smoke-free products), resulting in a more complicated dividend policy for management to figure out for the remaining company.

Or maybe Altria investors would receive some sort of special dividend to keep them whole in one of the merger scenarios laid out above. No one knows what management is considering.

The bottom line is that Altria's dividend safety profile remains complicated by its possible merger with Philip Morris more than anything else.

While I believe a combination with PM makes long-term strategic sense (better diversification, stronger balance sheet), the latest developments hurting Juul's value make the possible terms of a merger even less clear for Altria shareholders.

We always try to take a conservative view with our ratings, and that's what our Borderline Safe score reflects with Altria. Until we know more about management's intentions and priorities, Altria's score is unlikely to be upgraded. We will continue monitoring the situation and provide updates as warranted.

.png)