Preferred Apartment Retains Borderline Safe Rating But Transformation Creates Uncertainty

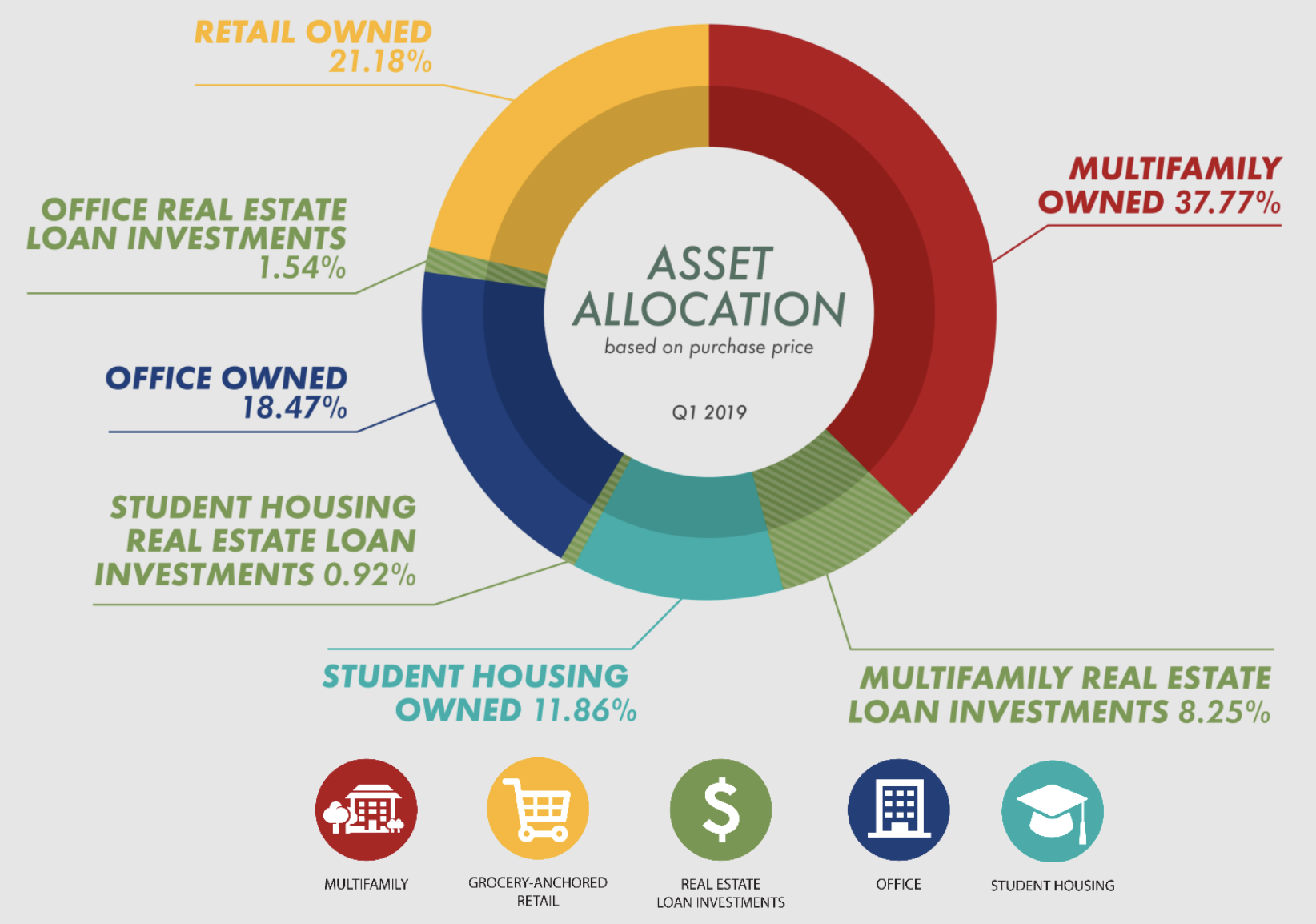

Preferred Apartment Communities (APTS) was founded in 2011. The REIT focuses on multifamily buildings (e.g. apartments), student housing properties, office buildings, and grocery-anchored retail centers. It also originates real estate loans to developers, receiving interest payments and the option to purchase finished projects.

Source: Preferred Apartment Investor Presentation

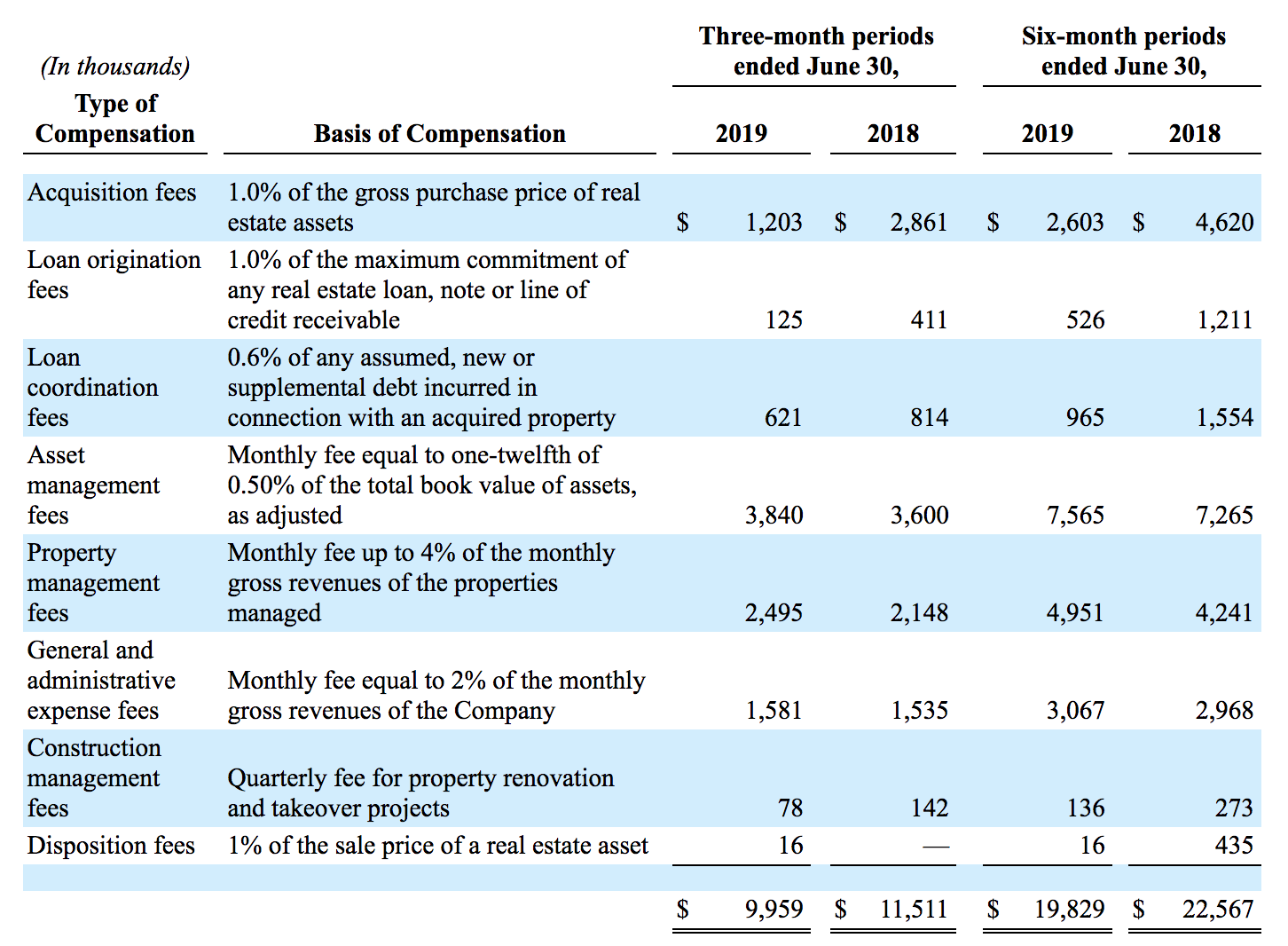

Preferred Apartment Communities, or PAC, is one of the few publicly traded REITs that has an external management team. Under this arrangement, PAC does not have any employees and instead pays fees to an outside manager to run its business.

This structure was put in place when the company was started because it was more economical compared to paying for its own staff when revenue was minimal.

However, PAC has grown its asset base from $0 in 2011 to nearly $5 billion today. The business generates more than $400 million in annual revenue, so doling out management fees based on a percentage of PAC's assets makes less sense.

As you can see, PAC's manager is on pace to generate about $40 million in fees this year, or nearly 10% of the REIT's total revenue. Most investors do not like external management structures because of the fees that reduce their returns and the conflicts of interest such arrangements can create.

Asset management fees, for example, encourage the manager to pursue growth at any cost rather than maximize the performance of existing assets.

Source: Preferred Apartments 10-Q Filing

As PAC has grown, its strategy has recently evolved in several ways that create some uncertainty for dividend investors going forward.

First, earlier this year PAC announced it was considering making a proposal to internalize its management team by potentially acquiring its manager.

Over half of REIT internalizations involve some form of equity or stock consideration, according to law firm Vinson & Wilkins. And they can be costly deals that impact a REIT's ability to maintain its common stock dividend.

In 2017, for example, Bluerock Residential (BRG), another small apartment REIT, decided to internalize its management team. The company issued about $40 million in equity to fund the transaction, diluting existing shareholders and pushing its payout ratio to an unsustainable level. As a result, Bluerock reduced its dividend by 44%.

In its 2018 annual report, PAC noted that internalizing its management could dilute its stockholders, result in higher costs, and reduce its earnings per share:

"There is no assurance that internalizing our management functions will be beneficial to us and our stockholders. Such an acquisition could also result in dilution of our stockholders if common stock or securities convertible into common stock are issued in the internalization and could reduce earnings per share and funds from operations attributable to common stockholders and unitholders, or FFO..."

Compared to Bluerock, PAC has a few advantages that could keep its dividend safe in the event of an internalization transaction. First, its payout ratio has historically been much lower (near 80% most years) than Bluerock's, which had exceeded 100% before its internalization transaction.

However, PAC's AFFO payout ratio is expected to approach 100% over the next year due to another strategic decision by the REIT to exit its student housing portfolio, which lacks the scale needed to be competitive and accounts for around 10% of PAC's assets and earnings.

Source: Simply Safe Dividends

PAC will receive cash proceeds when it closes the sale of its student housing properties, but the company's earning power will take a hit until that money can be reinvested in higher-return properties and loans.

Unfortunately, management is struggling to find many attractive investment opportunities today due to compression in cap rates, which have fallen along with long-term interest rates.

As a result, it's not clear what impact an internalization transaction could have on PAC's ability to continue paying its common dividend. If PAC decides to acquire all of the equity interest in its manager by issuing a substantial amount of equity, then its payout ratio could exceed 100%.

If management did not see a reasonably safe and efficient path back to a payout ratio closer to 80%, PAC could consider reducing its payout to a level more in line with other multifamily REITs.

PAC's dividend risk profile is further muddied by the REIT's unique financing arrangement. The company maintains many relationships with broker-dealers and registered investment advisors. Through these channels, PAC sells a lot of preferred stock to achieve stable capital inflows.

In recent quarters, PAC has issued between $40 million and $45 million of its preferred stock into these channels monthly, putting it on pace to sell more than $500 million in preferred stock this year alone. For context, PAC's market cap is less than $700 million.

Preferred stock is a critical component of the REIT's capital structure. In fact, for every $1 of common stock outstanding, PAC has issued nearly $3 of preferred stock. PAC is able to sell so much preferred stock in part because it offers brokers a 7% commission on these sales.

PAC's preferred stock carries a 6% yield and is a nontraded investment, meaning you can't buy or sell it on public exchanges. The stock can be redeemed at 97% of its face value after five years and also comes with warrants to purchase PAC's common stock at a 20% premium to the stock's price on the date the warrants were issued.

This arrangement seems to have made the most sense for PAC's external management, who were incentivized to grow the business as much as possible to maximize their asset management fees.

PAC's preferred stock isn't a low-cost source of capital with a 6% dividend and 7% commission, so it's hard to imagine the REIT was earning a great spread on the real estate and loan investments it made using this capital.

Regardless, if PAC internalizes, it may not be able to continue handling this large, steady inflow of capital unless it truly has many attractive and accretive investment opportunities to pursue.

If not, then PAC's preferred and common stock dividend liability would continue rising faster than its cash flow per share, putting further pressure on its payout ratio.

The bottom line is that PAC's business is undergoing structural changes that reduce its near-term cash flow and dividend coverage visibility. On the REIT's last call, management noted that some volatility is expected:

"The cumulative effect of these potential large and strategic moves...may create some short term volatility on earnings and FFO per share. Until we have full visibility to it as and when these moves materialize in final form, we are not currently adjusting our 2019 FFO guidance of a $1.44 to $1.50 per share."

On the bright side, the company's liquidity position looks solid. PAC holds $94 million in cash and has an untapped $200 million credit revolver, providing management with some flexibility to navigate a period of potentially spotty dividend coverage (PAC's common dividend consumes about $45 million annually).

Ultimately, PAC's focus on markets with favorable economics and hopes to move to an internal management structure are long-term positives for the company. However, these actions complicate PAC's short-term outlook.

Until more clarity is provided about PAC's internalization plans, evolving capital structure, and ability to find accretive investments to improve its dividend coverage, conservative income investors may want to remain on the sidelines.

Depending on how they play out, these moving parts, especially the terms of an internalization, could pressure PAC's Borderline Safe Dividend Safety Score.