Macy's Dividend Safety Score Downgraded to Unsafe due to Ongoing Struggles and Outlook

Earlier this year, we published a note reviewing Macy's dividend safety profile and struggles turning around its brick-and-mortar retail business. In the note, we said that Macy's Borderline Safe Dividend Safety Score was predicated in part on the company's turnaround efforts not stalling more than they already have.

Unfortunately, Macy's turnaround efforts have appeared to do just that.

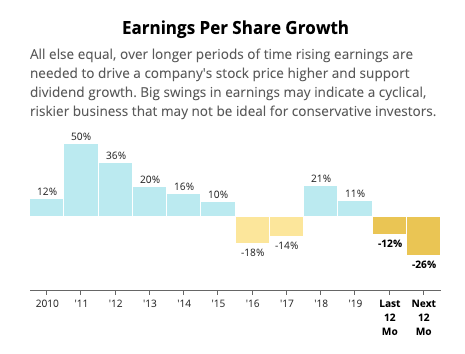

Despite a healthy economy and strong results from other retailers, Macy's reported disappointing earnings last month, forcing management to lower its full-year earnings guidance. Macy's earnings per share have now declined 12% over the past year, and analysts expect Macy's EPS to drop a further 26% over the next twelve months.

Source: Simply Safe Dividends

Management cited transient factors such as missed fashion trends and warmer weather as the reason for the decline in profits. However, given the hit the firm's financials have taken and the unfavorable long-term prospects of department stores in general, we've decided to downgrade Macy's Dividend Safety Score to Unsafe.

An Unsafe rating does not mean a dividend cut is imminent. Instead, it indicates that Macy's is now more reliant on favorable conditions to be able to maintain its dividend. Simply put, Macy's has less margin for error, a problem given that the company operates in the fast-changing, cutthroat, and increasingly competitive retail industry.

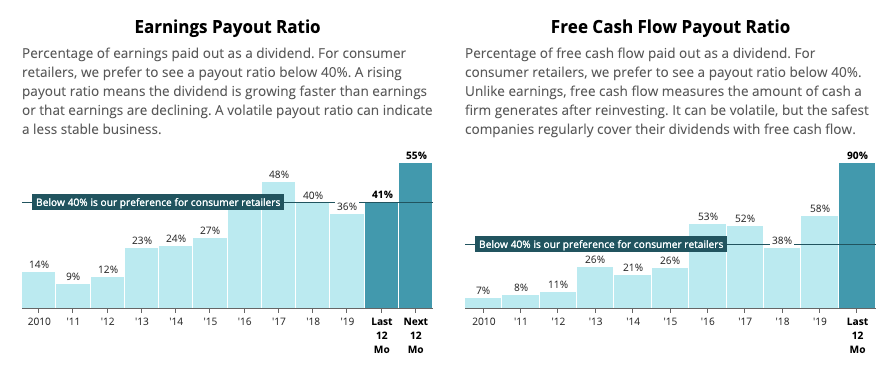

The squeeze is illustrated by Macy's earnings and free cash flow (FCF) payout ratios, both of which are above (or expected to be above) what we feel are comfortable levels in the challenging consumer retail industry:

Source: Simply Safe Dividends

Over the past twelve months, Macy's generated just $520 million in free cash flow while paying out $470 million in dividends (resulting in a 90% FCF payout ratio). In comparison, the retailer produced over $800 million of free cash flow in each of the last ten years.

The decline in free cash flow is due in part to Macy's struggle to attract shoppers without discounting prices. Even though sales have somewhat stabilized, the markdowns required to lure customers and clear out inventory have resulted in less overall profit.

Meanwhile, in order to remain relevant in retail, Macy's has ramped up investments in e-commerce initiatives and in-store modernization projects, further pressuring the cash Macy's has leftover to return to shareholders.

In the company's most recent earnings call, management reaffirmed that their top priority is to continue reinvesting in the business. Macy's will spend about $1 billion in capital investments this year (up from $932 and $760 billion the past two years), and the company will continue to need substantial amounts of cash to restructure its stores and attempt to return to profitable growth.

In addition to the company's large investment requirements, management has a stated goal of reducing its debt load. The company is targeting a leverage ratio of 2.5 to 2.8, and Macy's current leverage ratio of 2.7 is at the high of that range.

With a credit rating of BBB- (just one notch above junk status), the company needs to avoid a credit downgrade and may be forced to use excess cash to reduce debt, especially if the firm's leverage metrics are threatened by further declines in cash flow.

Macy's does own substantial real estate that the company could sell to raise funds for deleveraging, but cutting the company's dividend (which is entirely discretionary) seems like an easier, more prudent move in a crunch. It's also hard to say how valuable Macy's real estate is given that low foot traffic is part of the reason many locations are struggling.

Regardless, Macy's will return cash to shareholders in the form of dividends only after the company's reinvestment and debt reduction goals are met. So far, management has felt these these goals were adequately met and has thus continued to maintain the dividend.

However, the fourth-quarter holiday shopping season is critical. In recent years Macy's has generated more than 70% of its operating cash flow during the fourth quarter. If the retailer's profitability misses expectations again, reducing the dividend may become a necessity.

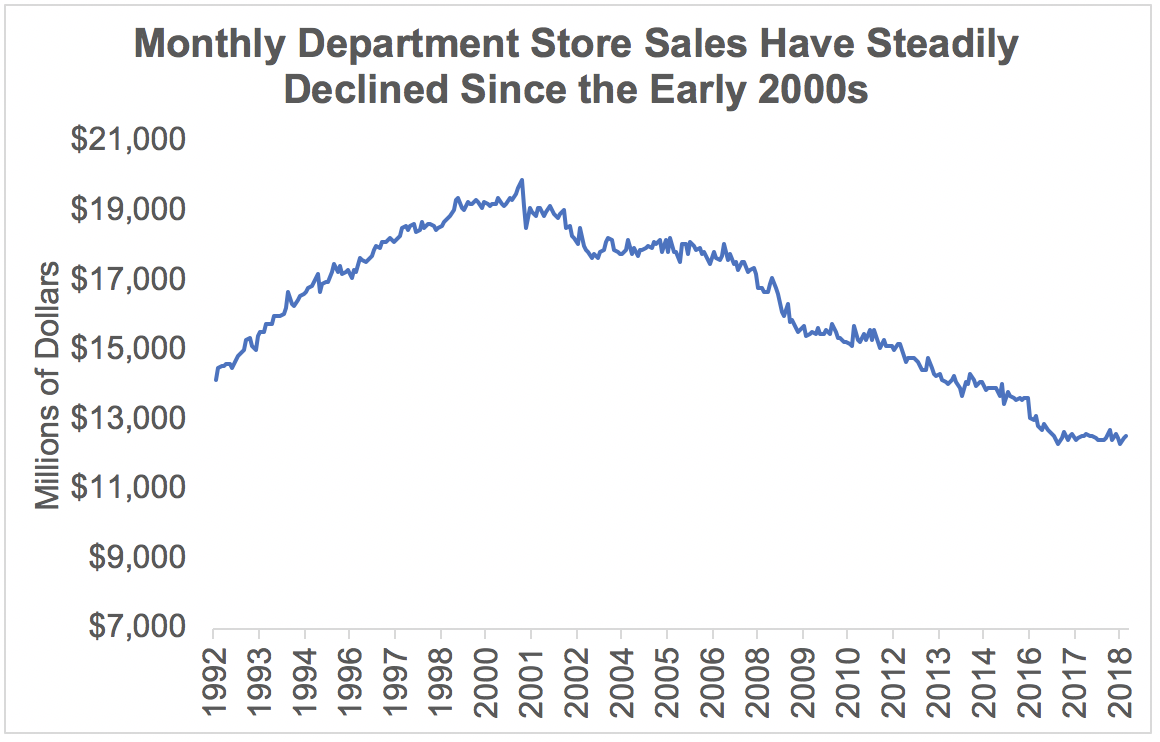

Even if the dividend is maintained next year, the long-term outlook of department stores is not particularly bright. Monthly sales at department stores peaked in the early 2000s and have witnessed a persistent decline since then:

Source: Simply Safe Dividends, U.S. Bureau of the Census

In short, e-commerce behemoth Amazon entered the scene and set new standards for convenience and selection. Discounters like Walmart, Target, and TJ Maxx have adapted in response and further raised the bar in the retail industry, leaving department store operators like Macy's behind in the race to survive in the age of online shopping.

Even if Macy's finds its niche and is able to the right the ship, the firm's financials leave little breathing room to pay the dividend in the event of a recession. During downturns, retailers — especially higher-end ones like Macy's — tend to see less traffic. (Macy's cut its dividend by 62% in February 2009 despite recording a 20% free cash flow payout ratio in fiscal 2008.)

In summary, we consider Macy's to be a speculative dividend stock given the pressure the dividend is placing on the business' investment and deleveraging needs, as well as the company's murky short-term and long-term outlooks.

Macy's valuation does not look demanding today, but our preference would be to move on in a case like this one. Turnarounds have a low success rate with a wide range of potential outcomes. Cheap stocks with high debt loads and questionable futures often find ways to become even cheaper.