Initiating Dow's Dividend Safety Score With a Borderline Safe Rating

In December 2015, Dow (DOW) and DuPont (DD) announced plans to merge, then break up into three independent companies. The idea was to create larger, more focused businesses by combining the areas of overlap in their complementary portfolios.

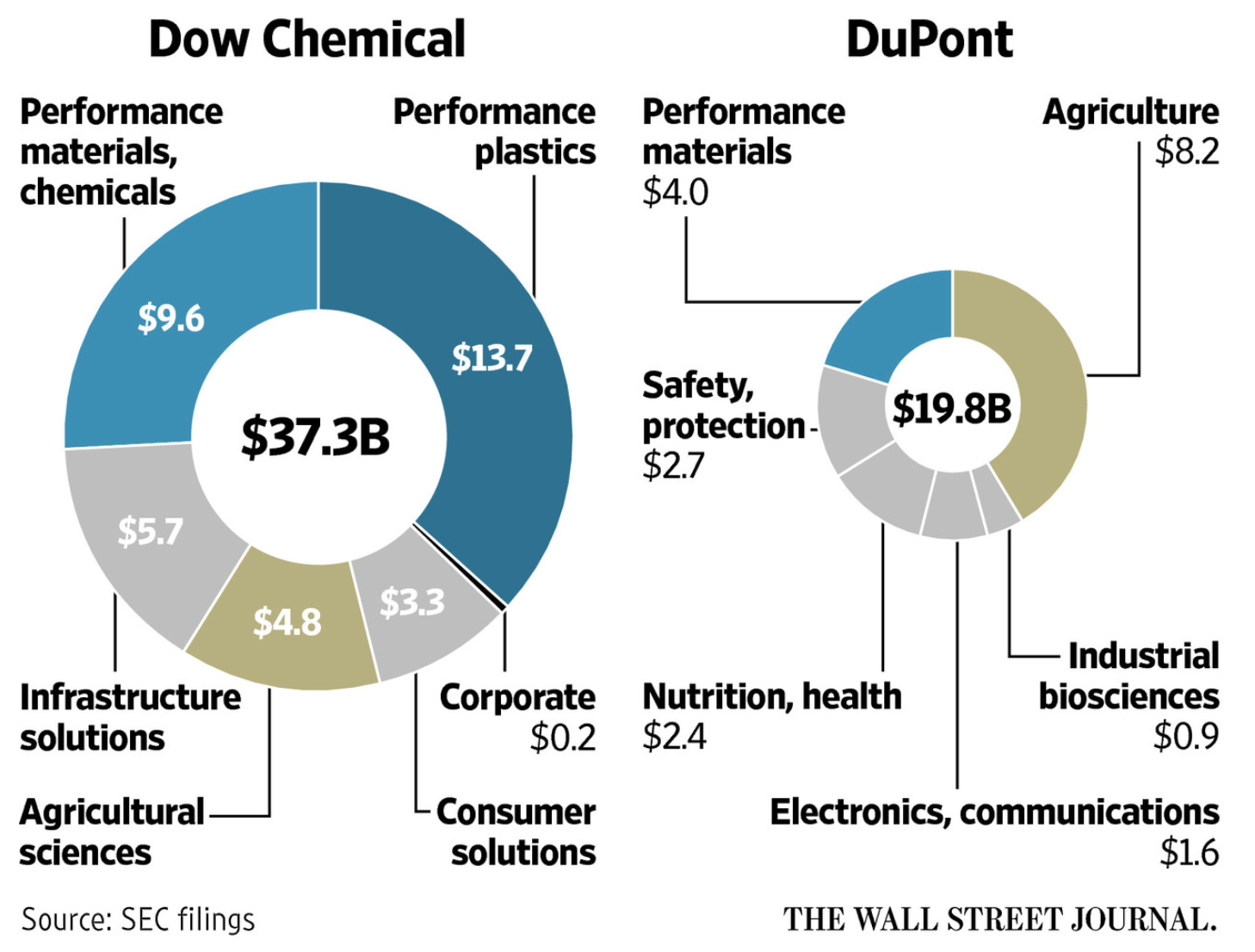

Here's a look at each company's 2015 revenue mix. As you can see, Dow and DuPont each had large agriculture and performance materials businesses which management believed would be better off together.

2015 Revenue Breakdown – Source: The Wall Street Journal

In September 2017, Dow and DuPont officially combined in a merger of equals under the name DowDuPont with three divisions intended to be split off into independent companies – Agriculture, Materials Science, and Specialty Products.

The DowDuPont chemical conglomerate finally separated into three publicly traded companies during the second quarter of 2019. DuPont retained the Specialty Products business, Corteva (CTVA) inherited the Agriculture division, and Dow took the Materials Science segment.

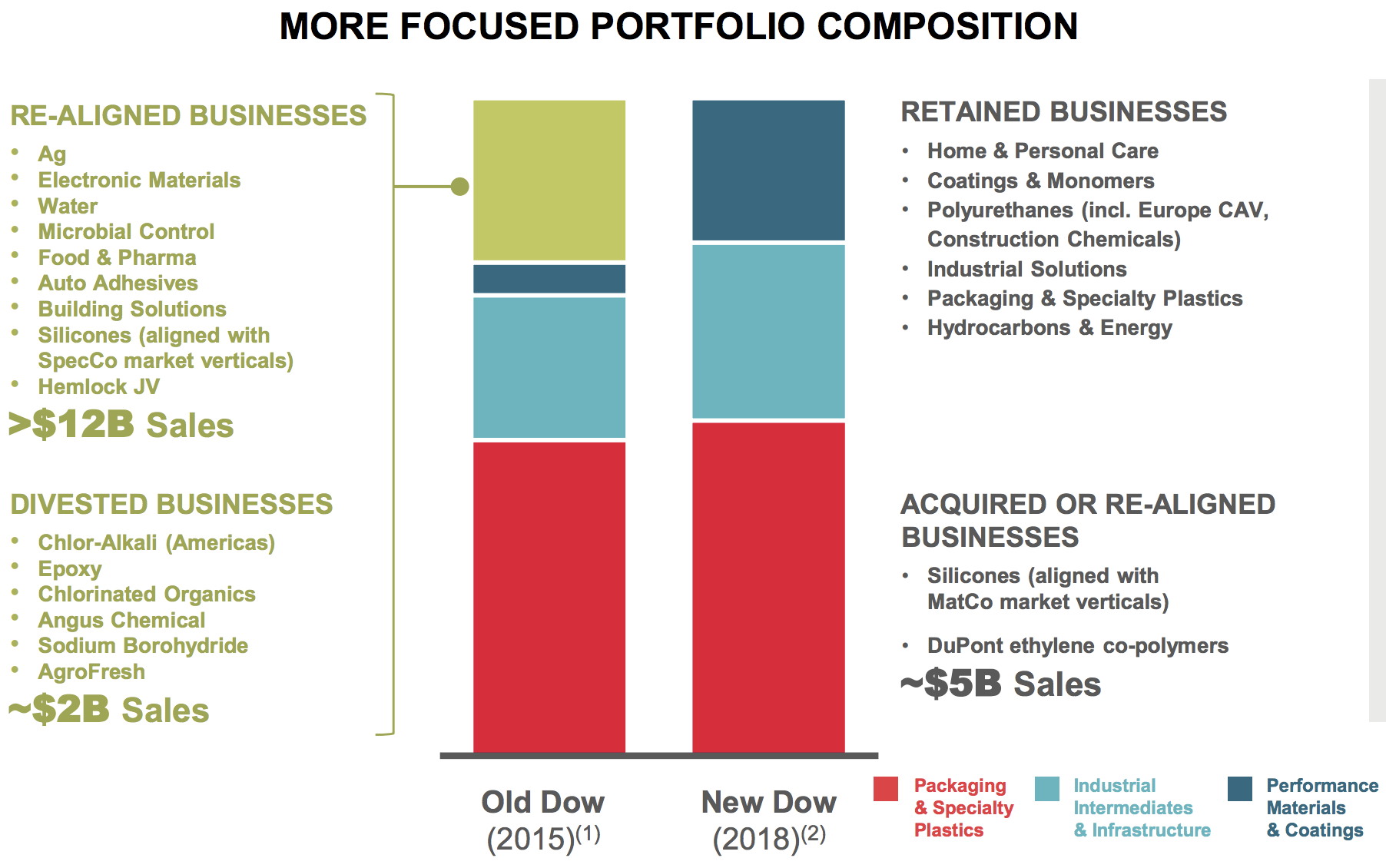

The new Dow actually isn't all that different from its pre-merger version. The company remains a commodity chemicals conglomerate with many moving parts. The main difference is that Dow no longer has some of its higher-margin, more specialized businesses such as agricultural pesticides and electronic materials.

Source: Dow Investor Presentation

However, with more than $40 billion in annual revenue, the new Dow remains one of the largest chemical companies in the world. The firm's offerings span more than 3,500 product families and reach thousands of customers in approximately 160 countries.

Here's how Dow organizes its business:

Packaging & Specialty Plastics (51% of 2018 EBITDA): Dow is a world leader in plastics, producing flexible and rigid packaging for food, consumer, health, and hygiene markets, as well as artificial turf, pressure pipe, and power transmission applications.

Industrial Intermediates & Infrastructure (27% of 2018 EBITDA): sells intermediate chemicals (solvents, lubricants, surfactants, etc.) used in manufacturing processes, as well as downstream materials used in applications including insulation, furniture, bedding, footwear, water treatment, energy, appliances, and construction products.

Performance Materials & Coatings (23% of 2018 EBITDA): consists of Dow's acrylics, synthetic plastics, and silicone technology platforms that provide solutions across consumer and infrastructure end markets, including paints, home care, and personal care.

Given the wide scope of Dow's business and the essential nature of many of its chemicals as inputs in other products, the company seems likely to remain relevant for years to come, just like it has since its founding in 1897.

However, Dow doesn't strike me as a great business, and it's a stock that most conservative income investors probably want to avoid.

As the industry's name suggests, the commodity chemicals space is characterized by relatively low margins and a lack of pricing power. Dow's profitability is driven mostly by factors outside of its control, such as oil and gas prices and global supply-demand balances across its major products.

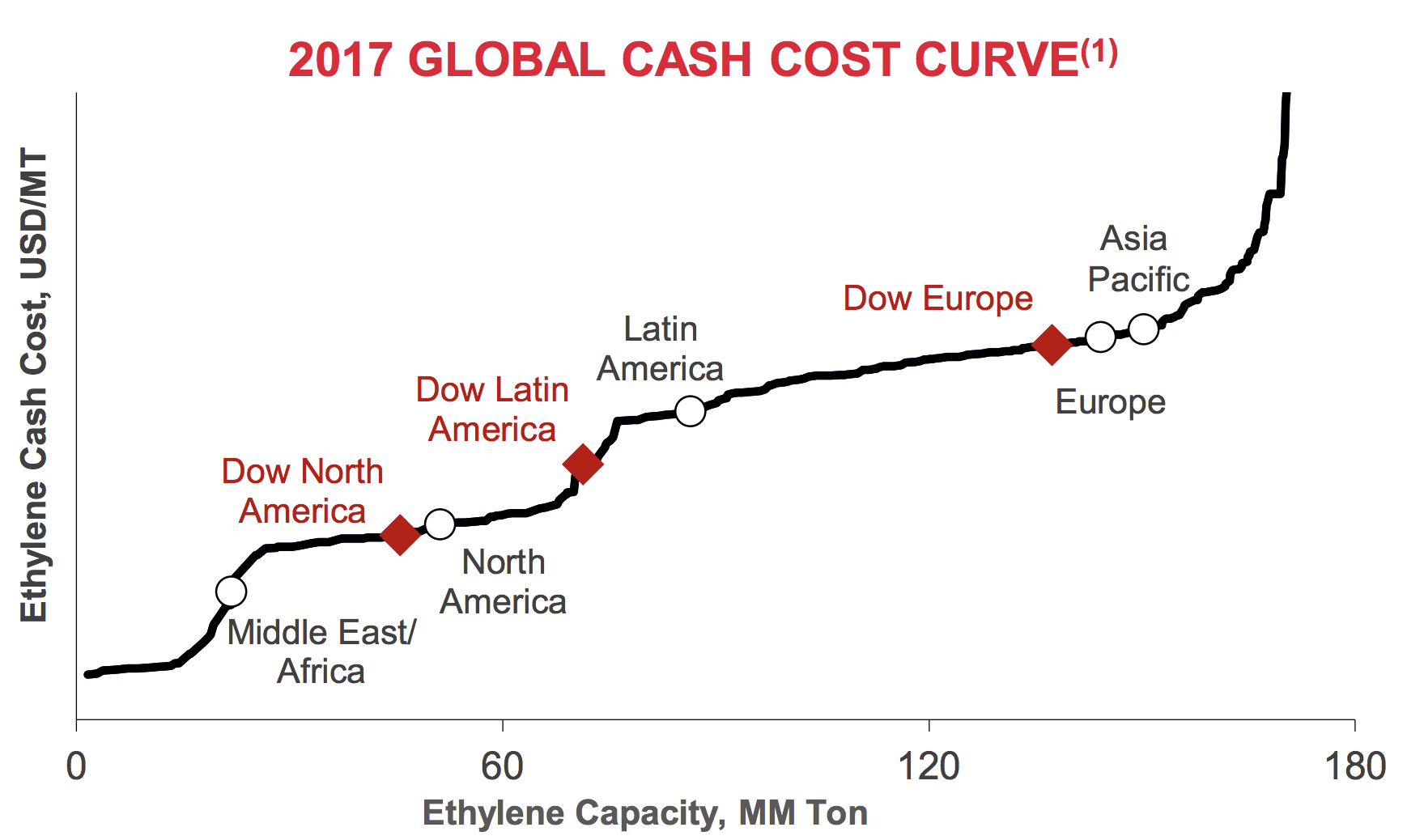

Natural gas (power source) and natural gas liquids such as ethane (feedstock) are core inputs for many of Dow's chemicals. Thanks to the U.S. shale boom, which has caused a surge in gas production and a corresponding plunge in prices, Dow's American chemical plants enjoy a favorable position on the global cost curve.

Meanwhile, the price of many of Dow's products such as polyethylene (its biggest business – plastics) is often tied to the global price of oil, which is a key feedstock used by many international rivals who have a higher cost of production compared to their American counterparts.

Source: Dow Investor Presentation

As a result, Dow usually benefits the most when the price of oil is high (maximizing selling prices in export markets) and the price of natural gas is low (minimizing input costs).

Besides commodity prices, industry supply-demand trends also affect Dow's profitability. When competitors bring new chemical plants online, industry operating rates can take a hit until the new capacity is absorbed.

These facilities represent a major investment with substantial fixed costs, so their operators are usually keen on maximizing their output. Constructing an ethylene cracker, for example, often takes years of time and can cost more than $1 billion.

If too much supply hits the market, or demand unexpectedly weakens, a glut of commodity chemicals and plastics can suppress industry pricing and Dow's profitability until a more favorable equilibrium is achieved.

Since Dow will never be able to command premium prices for most of its chemicals, the firm instead relies on its scale, low-cost U.S. operations, diversified product portfolio, and vertical integration to generate cost advantages over smaller rivals and reduce the volatility of its earnings.

The company is also executing on an ambitious cost-cutting plan to improve its cash flow generation in the years ahead. Efforts are focused on reducing the firm's number of management layers, rationalizing its manufacturing footprint, and improving the efficiency of its production processes.

Ultimately, Dow is a volatile, capital-intensive business that is most sensitive to factors outside of its control. While demand across Dow's end markets seems likely to grow at least in line with global GDP in the long term, the firm's short-term results are much less predictable.

With that backdrop, let's take a look at Dow's dividend profile.

We assign the new Dow a Borderline Safe Dividend Safety Score, reflecting the company's cyclical profits, above-average payout ratio, and moderate leverage.

Likely in an effort to attract investors, management targets a long-term payout ratio across the cycle of approximately 45% of operating net income.

As the company notes, this is an "industry-leading" payout ratio, meaning Dow has decided to distribute a higher proportion of its earnings as a dividend compared to its peers.

During good times, this is a nice benefit for income investors, especially since management intends to grow the firm's dividend as earnings and free cash flow expand (likely no more than a low single-digit pace).

However, a generous payout also reduces Dow's margin of safety during recessions, when its cyclical chemical businesses can experience a sharp drop in profits. This could pressure Dow's credit rating during a downturn, creating a need to conserve capital.

After all, management desires to maintain a "strong investment grade credit rating across the cycle" and targets a 2.5 to 3.0 gross leverage ratio. That's already at the high end of our preferred range for chemical producers.

Moody's has said that Dow's BBB-equivalent rating could be downgraded "if credit metrics weaken sustainably with Debt/EBITDA remaining above 3.0x", which seems like a possibility in the event of a prolonged recession.

Investors need to respect this risk since protecting its investment grade credit rating was a key driver behind Dow's only dividend cut in its 100-plus year history.

Dow began making dividend payments in 1912 and maintained or increased its payout each year until the financial crisis, when it cut its dividend by 64% in 2009.

As MarketWatch noted, Dow faced "uncertain credit markets, lower demand for its products and legal wrangling over a failed joint venture and acquisition of Rohm & Haas." The firm's former CEO said that the top priority in times of economic uncertainty had to be the company's investment grade rating, so the dividend was axed to preserve capital.

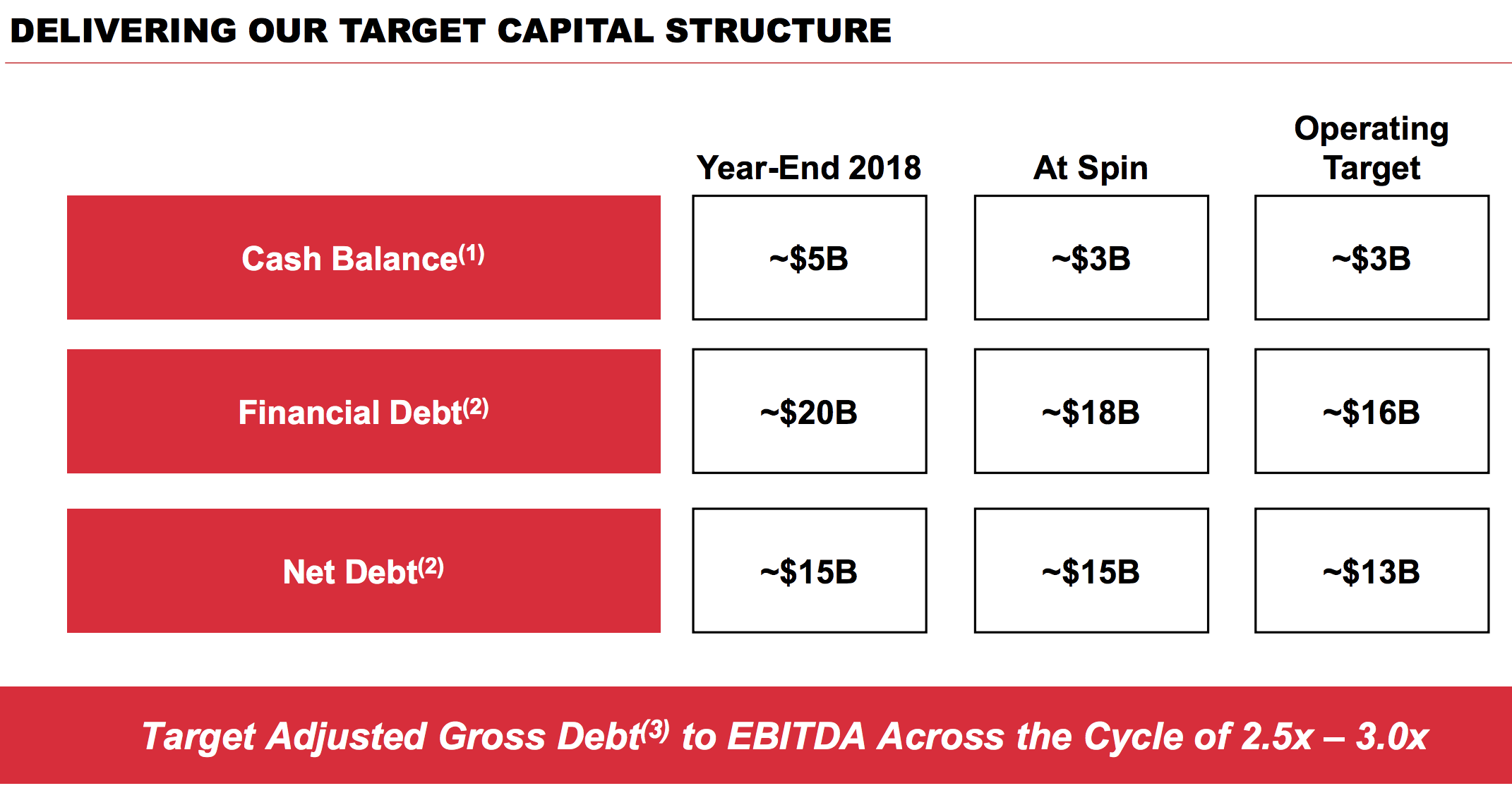

Today, Dow's target capital structure calls for the company to maintain a healthy cash balance of $3 billion, which exceeds its $2.1 billion annual dividend commitment. The firm also maintains a $5 billion credit revolver and has manageable debt maturities for the next few years, providing it with solid liquidity for the foreseeable future.

Source: Dow Investor Presentation

Overall, Dow's Borderline Safe Dividend Safety Score reflects the uncertainties that a cyclical, moderately leveraged business like this faces during economic downturns.

The company seems committed to its dividend over a full cycle, but that requires the firm to be managed conservatively. Dow's payout ratio and leverage targets feel a little aggressive to me, making its long-term dividend safety outlook somewhat murky.

Aside from those concerns, Dow's large size, low-cost assets, vertical integration, essential products, cost savings plan, and more disciplined capital spending support the company's ability to generate decent cash flow and pay generous dividends over time.

However, as a conservative income investor with a fairly concentrated portfolio, I prefer to avoid almost all commodity companies, especially those with meaningful leverage, capital-intensive operations, and a high dependence on uncontrollable macro factors (oil-gas spread, industry capacity additions, global economy, etc.).

The new Dow looks even more cyclical and sensitive to commodity prices than the old Dow, reducing its appeal to me. It's hard to keep track of all those moving parts, and I'd rather own businesses that can deliver more predictable earnings and dividend growth.