Boeing's Dividend Profile Remains Stable After MAX Grounding Update

Boeing's (BA) best-selling plane model, the 737 MAX, has been grounded since mid-March following two deadly crashes. Analysts had estimated this plane series would account for about two-thirds of the company's future deliveries and roughly 40% of Boeing's total profit.

Understandably, many investors remain concerned about the risks Boeing faces from this ordeal. Based on what we know today, Boeing's dividend continues to look safe. However, further setbacks could result in the company's Dividend Safety Score being downgraded to our Borderline Safe rating.

This past week the company provided two updates. First, on July 18, Boeing announced it would take an after-tax $4.9 billion charge "in connection with an estimate of potential concessions and other considerations to customers for disruptions related to the 737 MAX grounding and associated delivery delays."

Essentially, the 737 MAX's grounding has affected the schedules of airlines that use its planes, so Boeing has to make that up to them. Southwest Airlines (LUV), for example, said earlier this week that the MAX grounding "reduced its operating income an estimated $175 million" in the second quarter.

Boeing's attempt to quantify those damages is helpful as investors try to gauge the company's financial risk. For context, in 2018 Boeing recorded over $100 billion in revenue, generated more than $13 billion in free cash flow, and repurchased $9 billion worth of its shares. In other words, a $4.9 billion charge appears manageable for a company of this size.

Boeing's compensation to its customers seems unlikely to be in the form of straight cash, too. Instead, as Standard & Poor's notes, airlines will likely enjoy price discounts on future orders or free upgrades and services. That further lessens the strain placed on Boeing.

Of course, the $4.9 billion after-tax charge is merely an estimate made by management. The amount of damages owed to customers could escalate if the 737 MAX remains out of service for longer than management expects, and Boeing would likely face rising production costs as well.

On that note, Boeing reported second-quarter earnings on July 24. A longer than expected reduction in the 737 MAX's production rate caused Boeing to increase its estimated production costs of the program by $1.7 billion. The company continues building these costly planes, but it can't deliver them to customers.

Boeing has to keep its finished 737s in storage and can't get paid for its capital-intensive efforts until airlines are able to begin accepting deliveries again. That won't happen so long as the 737 MAX remains grounded.

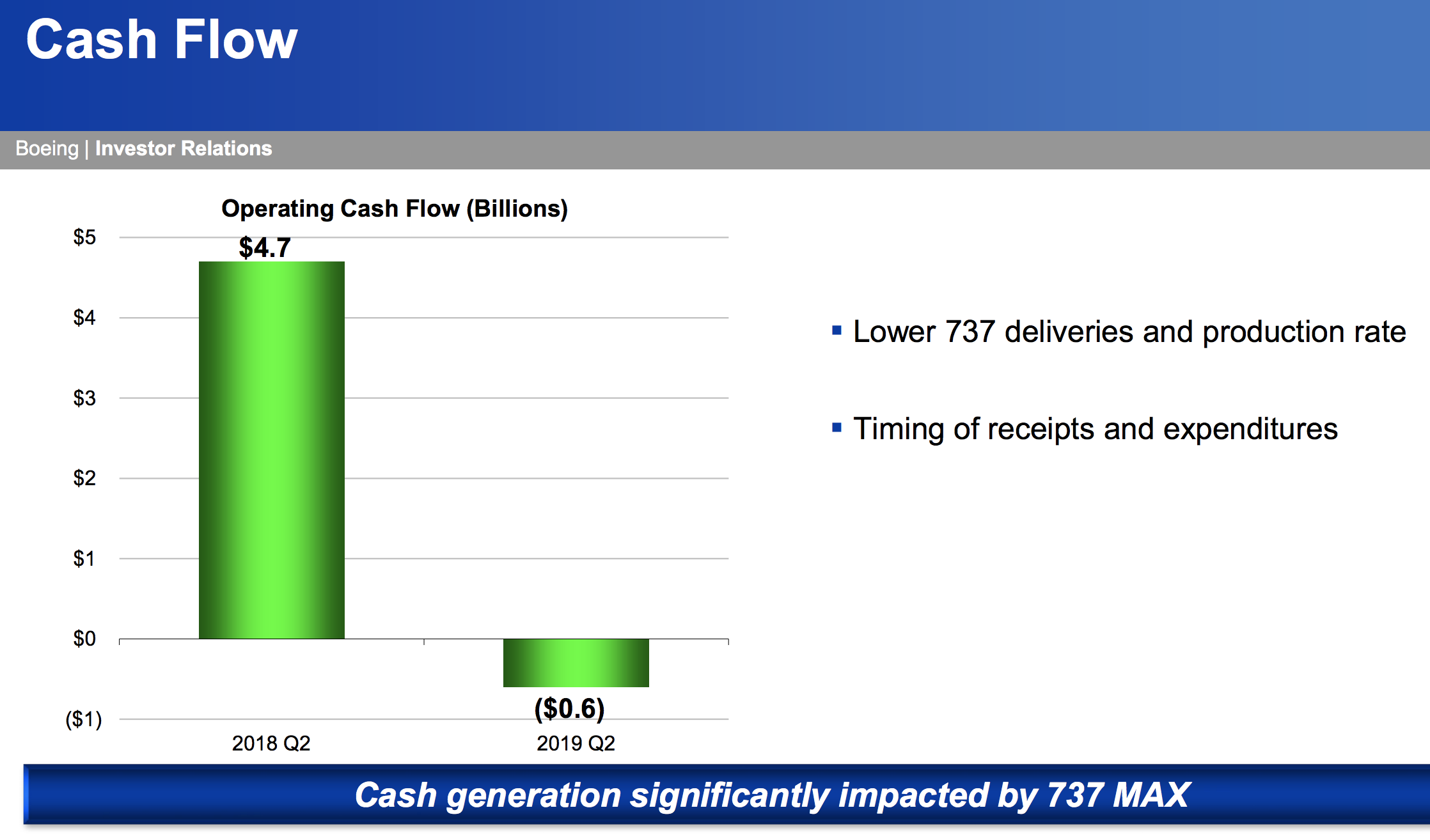

As a result of Boeing's ballooning inventory, the company's operating cash flow declined $0.6 billion last quarter, compared to $4.7 billion increase in the second quarter of 2018. The company also paid $1.2 billion in dividends, further hurting its cash flow position.

Source: Boeing Investor Presentation

A situation like this can spell bad news for a company's dividend if it proves to be anything more than temporary. Fortunately, management still expects better times ahead, issuing the following guidance:

Regulatory approval of MAX return to service in the U.S. and other jurisdictions begins early in fourth quarter 2019

Planes will be delivered to customers over several quarters beginning in January 2020 following regulatory approval of return to service

A gradual increase in the 737 production rate from the current 42 per month to 57 per month in 2020

Based on these expectations, Moody's believes Boeing will generate negative free cash flow of $5 billion or more in 2019, but the firm has potential to produce "positive free cash flow in excess of $10 billion in 2020, assuming deliveries re-start by January 2020 and no new capital-consuming issues arise."

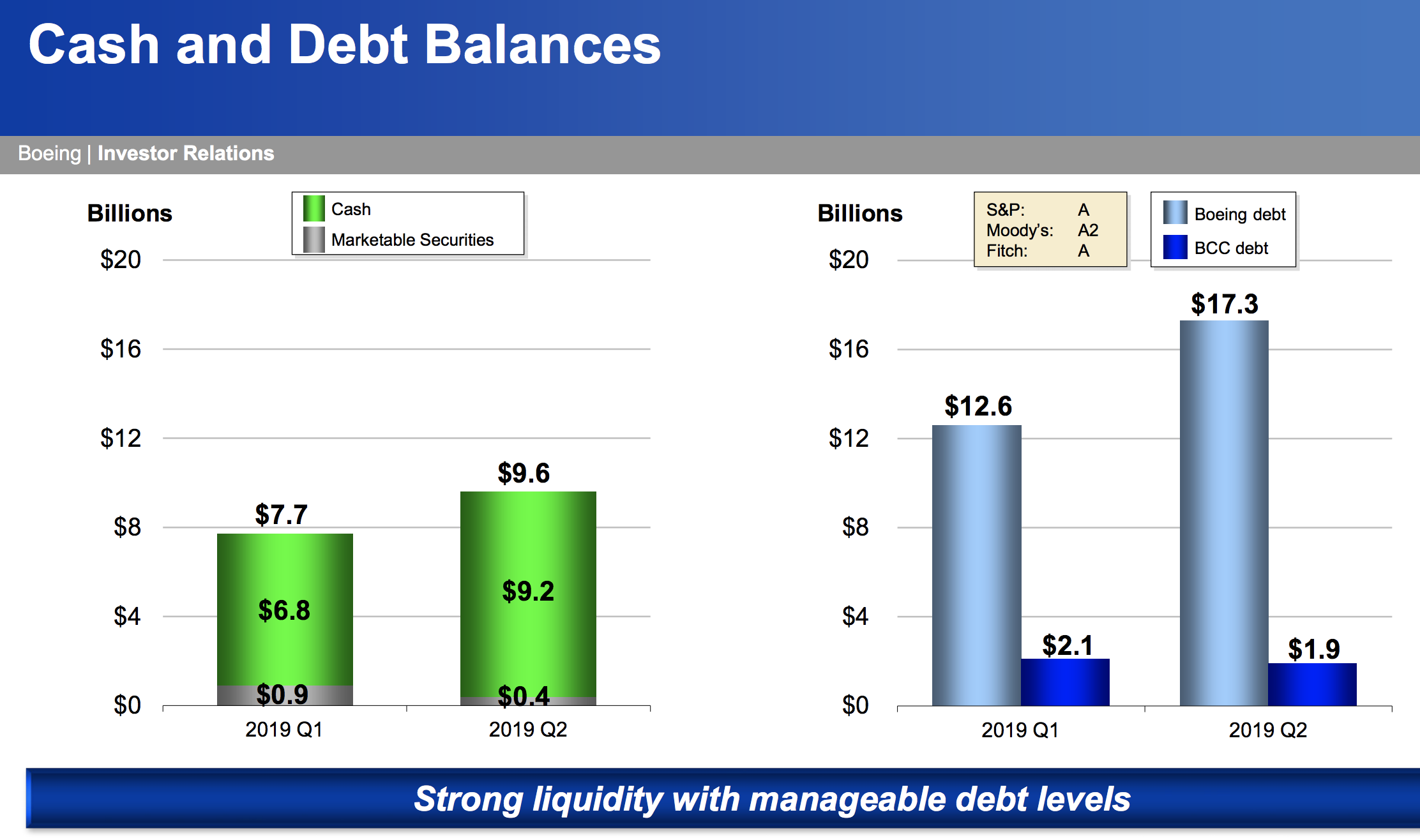

To preserve liquidity, Boeing already suspended its share repurchase program until it has greater clarity on the MAX's return to service. The company also has nearly $10 billion in cash on hand (thanks in part to issuing debt recently), plus an unused credit facility of $6.6 billion.

Source: Boeing Investor Presentation

Basically, Boeing's liquidity position looks solid as it works through the current 737 MAX challenges. It would be very surprising if the dividend came under pressure based on management's latest guidance.

However, no one really knows what will ultimately happen with the 737 MAX. On the earnings call, management noted that if their estimate of the anticipated return to service is pushed beyond the fourth quarter of 2019, then they "might need to consider possible further rate reductions or other options, including a temporary shutdown of the MAX production."

Predicting the behavior of regulators such as the U.S. Federal Aviation Administration (FAA) or the European Union Aviation Safety Agency (EASA) is impossible. An issue like this could potentially last much longer than Boeing expects.

The liabilities that would mount with each passing month would be substantial, especially given the complexities of Boeing's supply chain and the steep cost associated with ramping up and down the production rates of capital-intensive planes.

If Boeing finds itself in a place where it can no longer predict when the 737 MAX is returned to service, and it worries about its future liquidity for whatever reason, then its nearly $5 billion annual dividend commitment could be tested.

Such an outcome seems like a low probability event, especially since Boeing appears open to ceasing production to preserve working capital. However, investors holding shares of Boeing should understand that the stock could be more volatile than usual in the months ahead. The stock's risk profile has increased following the MAX's grounding, and the short-term financial stakes are high if the return-to-service timeline is pushed out.

Fortunately, while Boeing's reputation has taken a hit, the firm's long-term outlook seems likely to remain intact. Boeing's commercial airplane backlog remains strong at $390 billion, global air traffic continues rising, and the rest of the company's business continues firing on all cylinders.

The Wall Street Journal has also observed that historically "crashes don't tend to affect the popularity of plane models." According to their article, the 737 plane model has flown in the skies since 1966 and represents the best-selling commercial plane family in history with over 10,000 delivered. It's hard to imagine a sustained world-wide rejection of the MAX.

For these reasons, the market has thus far reacted calmly to the predicament Boeing is in. Investors seem to believe management's expectation that a timely return to service will occur, allowing cash flow to jump significantly next year once MAX deliveries are finally made.

As we stated in our April 2019 note, we will continue monitoring the situation to ensure that Boeing's market share remains stable and the MAX grounding is indeed temporary rather than longer term in nature. Otherwise, Boeing's cash burn and liquidity position will need to be evaluated, and its Dividend Safety Score could be downgraded.