WPP's Dividend Safety Hinges on Success of Turnaround Plan

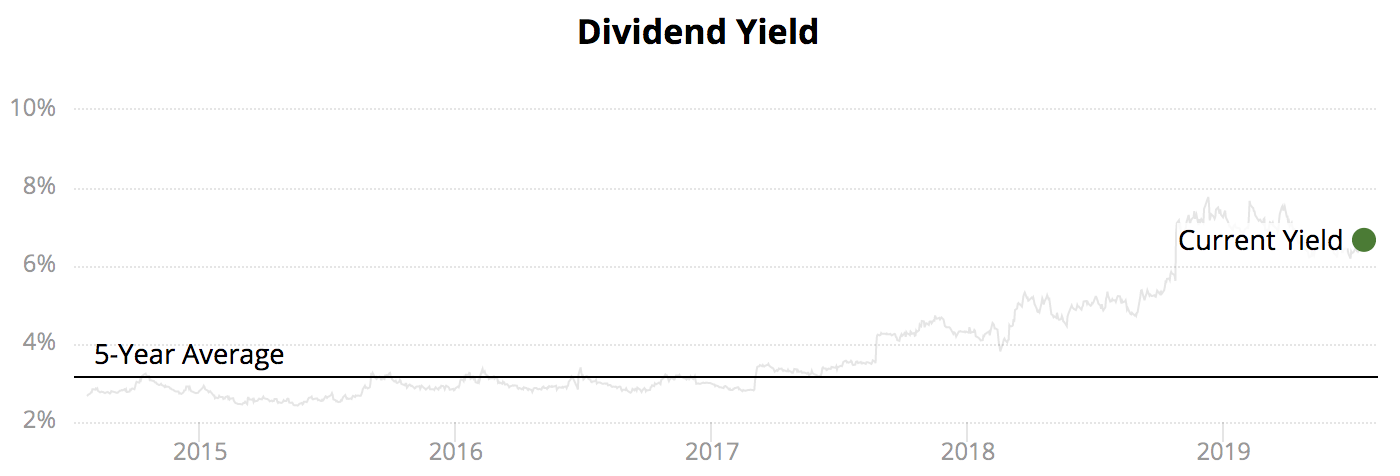

Down more than half from their mid-2015 high, shares of WPP (WPP) yield nearly 7% today. The global advertising conglomerate has paid uninterrupted dividends for more than 20 consecutive years, but its business has faced challenges from the rise of digital marketing and shifting client needs.

Source: Simply Safe Dividends

In recent years, some consumer staples giants such as Procter & Gamble have trimmed their marketing budgets. Media fees have also fallen, and a rise in in-house work and project-based assignments have reduced the average value of a creative agency account win, according to Adweek.

As a result, WPP's organic net sales declined in 2017 and 2018, and management expects 2019 to be another down year. However, each of WPP's major rivals – Publicis Groupe, Omnicom, Interpublic, Dentsu, and Havas – reported organic sales growth last year.

WPP's lackluster execution during this period of industry change has caused many investors to question its ability to grow again. It's hard to say exactly why WPP has fared so much worse than its peers, but the firm has lost notable accounts to competitors including Ford, Mercedes-Benz, PepsiCo, United Airlines, and American Express.

As the largest ad agency holding company in the world with more than 130,000 employees, WPP is not any easy ship to steer in a different direction. Here's what Standard & Poor's said in an October 2018 note when they maintained WPP's BBB credit rating but cut the firm's outlook to negative:

"Although large size and scale are crucial to profitability in media buying, and have benefited WPP previously, these advantages are becoming less relevant. In the current operating environment, it is more important to offer higher pricing transparency to clients, and to build on creative and data capabilities under a simpler operating structure that is more focused on the clients' needs.

WPP has been slower than peers to address these challenges and its operational performance has been weaker over the past two years. It has also suffered as some of its clients have cut their advertising spending and it has lost several large contracts to competitors."

After leading WPP for more than 30 years, Martin Sorrell stepped down in April 2018 following a personal misconduct investigation. Insider Mark Read, who ran WPP's digital agency, was named as CEO in September 2018.

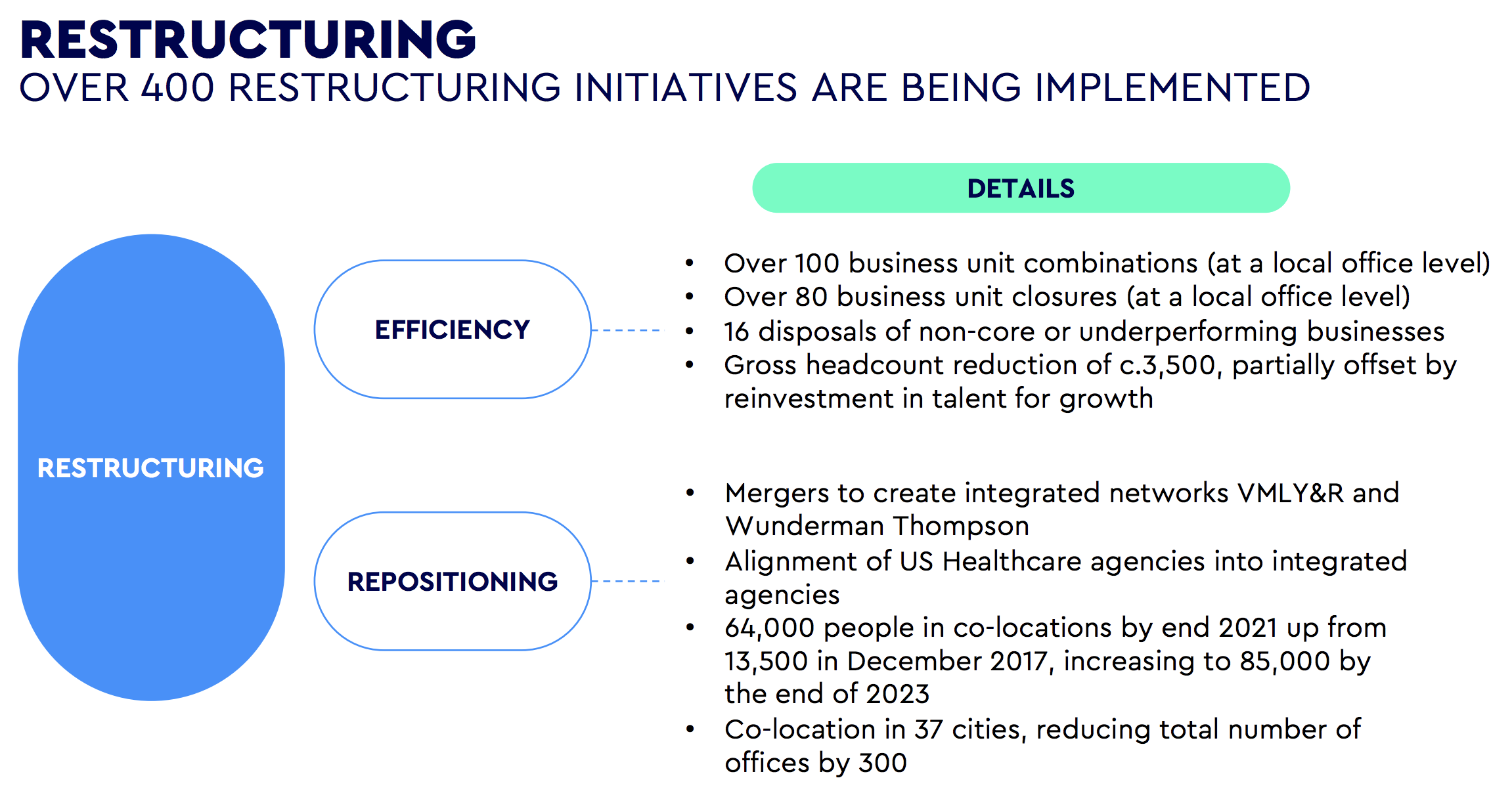

Mr. Read laid out a multiyear turnaround plan in December 2018 that he hopes will get WPP's organic growth rate in line with industry peers by the end of 2021.

Source: WPP Investor Presentation

To get there, WPP is engaged in hundreds of restructuring initiatives to simplify its organizational structure, shed non-core businesses, invest in talent that is better aligned with client needs, and shrink its footprint of offices.

In total, WPP expects its restructuring plan to cost £300 million ($375 million) and deliver £275 million ($345 million) of gross savings by 2021, representing about 1.8% of revenue.

Source: WPP Investor Presentation

It's too soon to say whether or not WPP's turnaround efforts will be successful. There are a lot of moving parts to a company this big, and management's cuts may not be enough. On a positive note, continued growth reported by its peers suggests the industry's changes are manageable for the incumbents rather than serving as an insurmountable secular headwind.

What about WPP's dividend? During major turnarounds, company's sometimes adjust their capital allocation policies to improve their financial flexibility. If a business has too much debt, cutting the dividend can be an appealing option to create more breathing room.

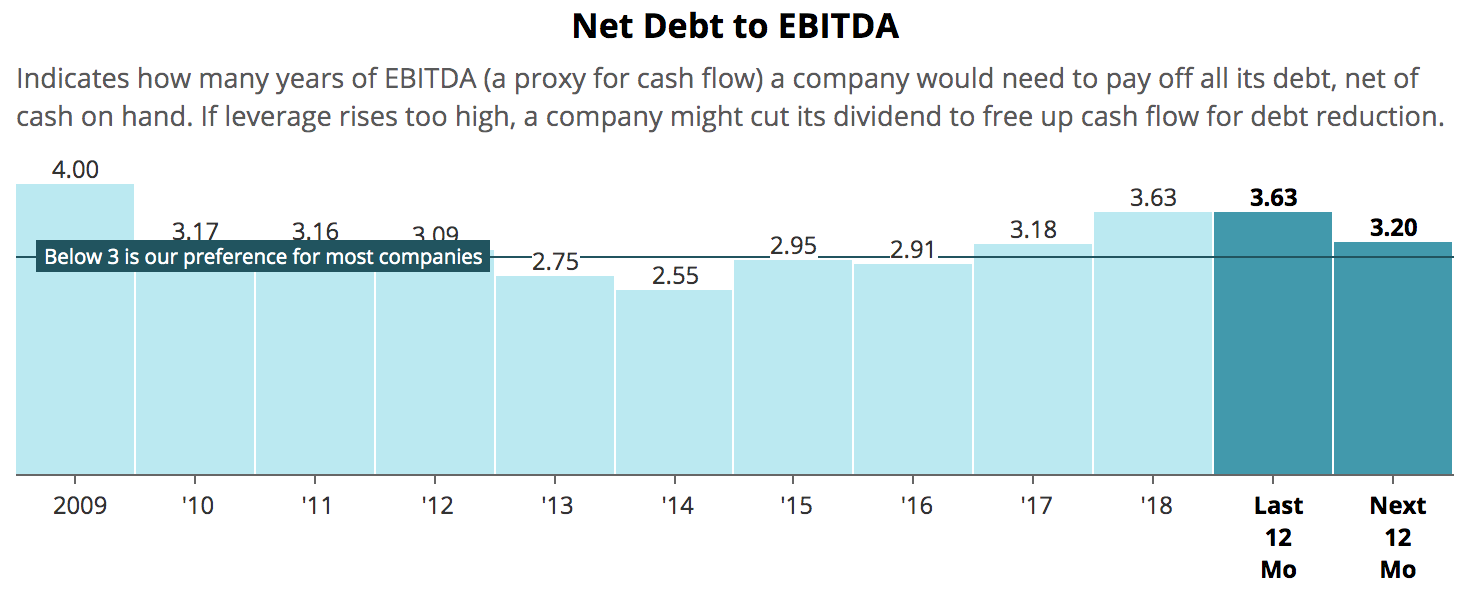

In WPP's case, the company maintains a BBB investment grade credit rating from Standard & Poor's. However, it has a negative outlook, and the firm's current leverage ratio is higher than our preferred level.

Source: Simply Safe Dividends

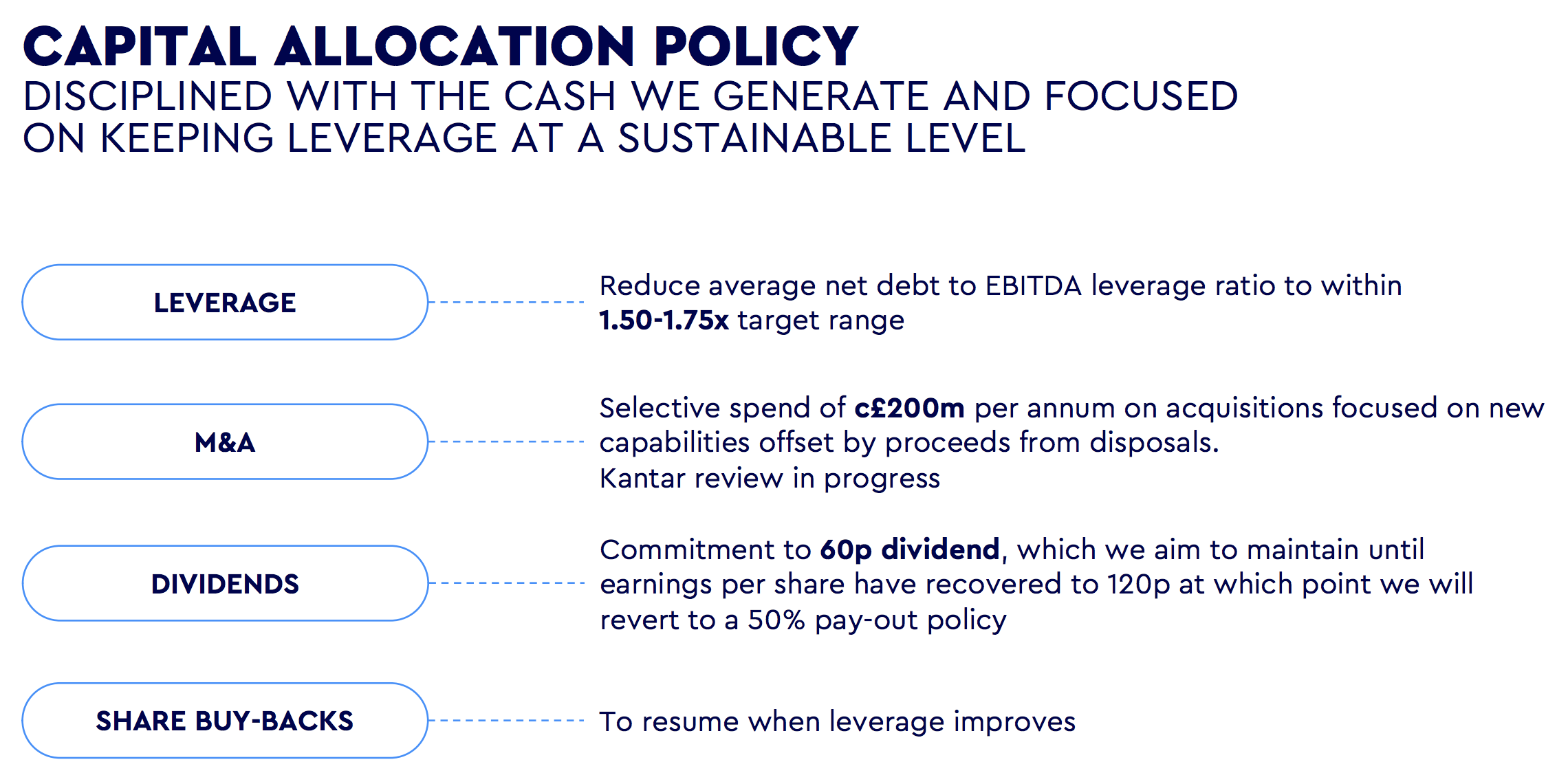

Management's priority is to reduce leverage. The firm's net debt to EBITDA ratio stood at 2.1 at the end of 2018, according to the company. (Our leverage measure is higher since we account for off-balance sheet debt.) WPP would like to reduce its leverage ratio to within 1.5 to 1.75. In the meantime, minimal money will be spent on acquisitions, and share buybacks are suspended.

Source: WPP Investor Presentation

The company says it will only "aim to maintain" the current dividend since WPP's payout ratio is higher than desired. WPP's earnings payout ratio was 50% in 2017 but increased to 56% in 2018 and is projected to sit at 63% over the year ahead. Management targets a 50% payout ratio, so the company needs earnings to improve in the future to justify the current dividend level.

Until the company's turnaround plan starts bearing fruit and its leverage and payout ratio decline to more comfortable levels, WPP's dividend profile looks somewhat speculative.

If the company's turnaround efforts don't bear fruit, reducing the dividend, which costs the company over $900 million annually, would free up capital WPP could use to invest in relevant services, acquire on-trend agencies, and maintain a healthy balance sheet.

In order to upgrade WPP's Dividend Safety Score to Borderline Safe or better, we need to see the company's leverage and payout ratio decline. The company's turnaround has to deliver traction and get organic growth back on track.

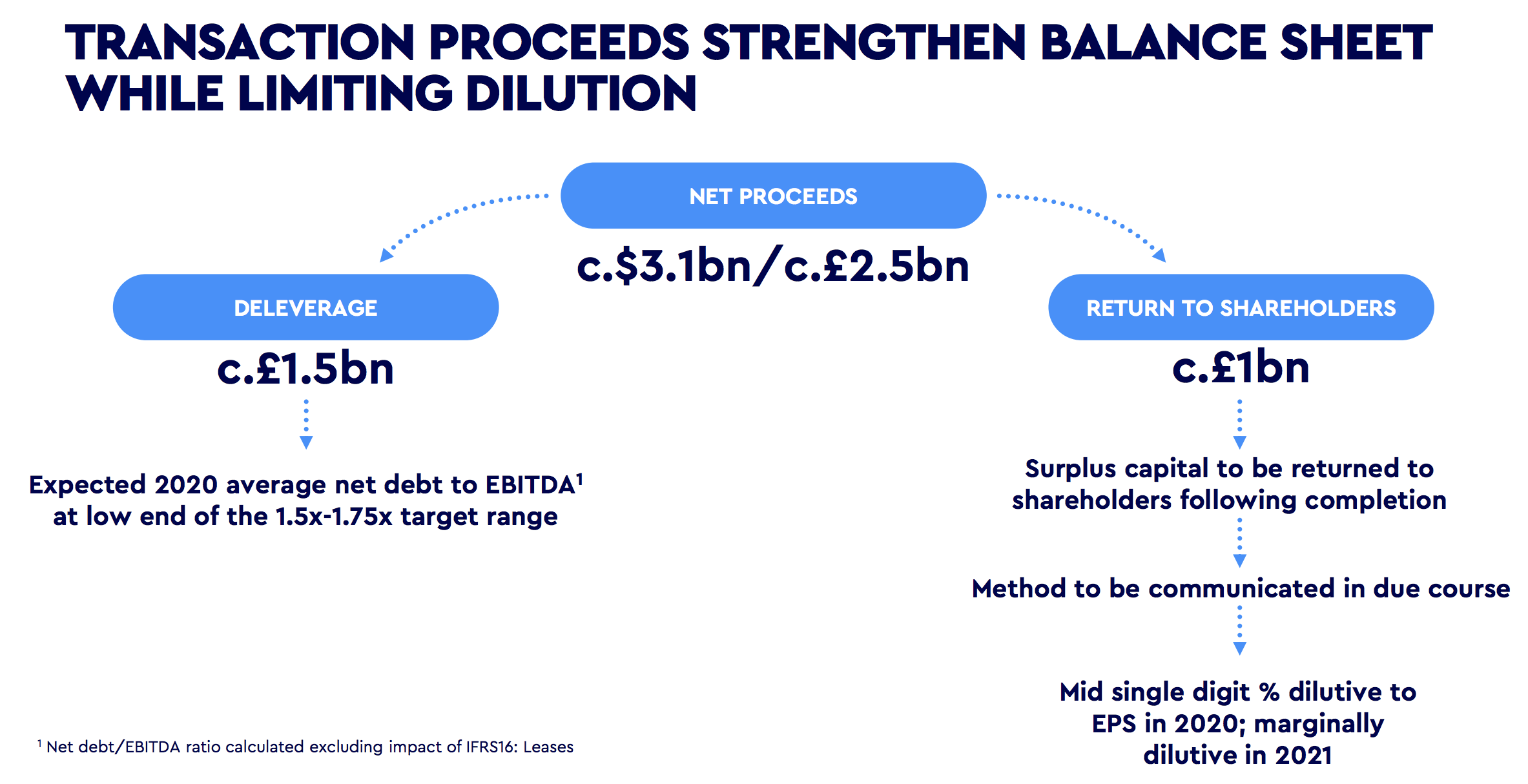

With that said, it is encouraging to know that management has publicly stated they will "prioritize the dividend over share buybacks." Earlier this month WPP also announced a deal that will take its net debt to EBITDA ratio to the low end of its target range next year, ahead of schedule.

Specifically, the company agreed to sell 60% of Kantar, a mature data and research business that accounted for about 15% of WPP's sales and profits. Management will use 60% of the proceeds for deleveraging while earmarking the remaining £1 billion ($1.25 billion) for a return of capital to shareholders.

Source: WPP Investor Presentation

Management hasn't said how the $1.25 billion in capital will be returned to shareholders, but that amount would more than cover the semi-annual dividend for a year and most of the turnaround's estimated restructuring costs. In other words, WPP's dividend does not appear to be at risk of an imminent cut.

However, selling a majority stake in Kantar is expected to reduce WPP's earnings in 2020 by a mid-single digit percentage. All else equal, this would put the company's payout ratio between 65% and 70% next year.

While that's not necessarily a dangerous level, especially given WPP's improved balance sheet, it is well above management's 50% target. If WPP doesn't return to sustainable growth like the company hopes, or a recession occurs that saps client ad spending, then management could look to reduce the dividend in order to improve the firm's financial flexibility.

Overall, WPP is an interesting turnaround situation. The company has a lot of valuable client relationships and generates good cash flow, but it has not adapted quickly enough in a fast-changing marketing world. WPP's dividend seems unlikely to face an imminent cut, especially as the balance sheet improves following its Kantar sale, but the firm must execute on its restructuring plan.

Given some of the industry's persistent headwinds and the massive size and complexities of WPP, it will likely take a year or two to gauge the success of management's actions. Conservative income investors are likely best off watching from the sidelines until WPP demonstrates that its fundamentals have stabilized and begun to improve.