Enbridge's Largest Project Further Delayed But Dividend Safety Profile Remains Unchanged

Enbridge (ENB) investors have had a rough few years, with shares of North America's largest pipeline operator losing more than 20% since early 2015, including dividends.

Unfortunately, investors received more bad news earlier this month. On June 3, the Minnesota Court of Appeals overturned approval for an important part of the firm's Line 3 Replacement Project, which was expected to account for about 50% of Enbridge's growth spending over the next few years.

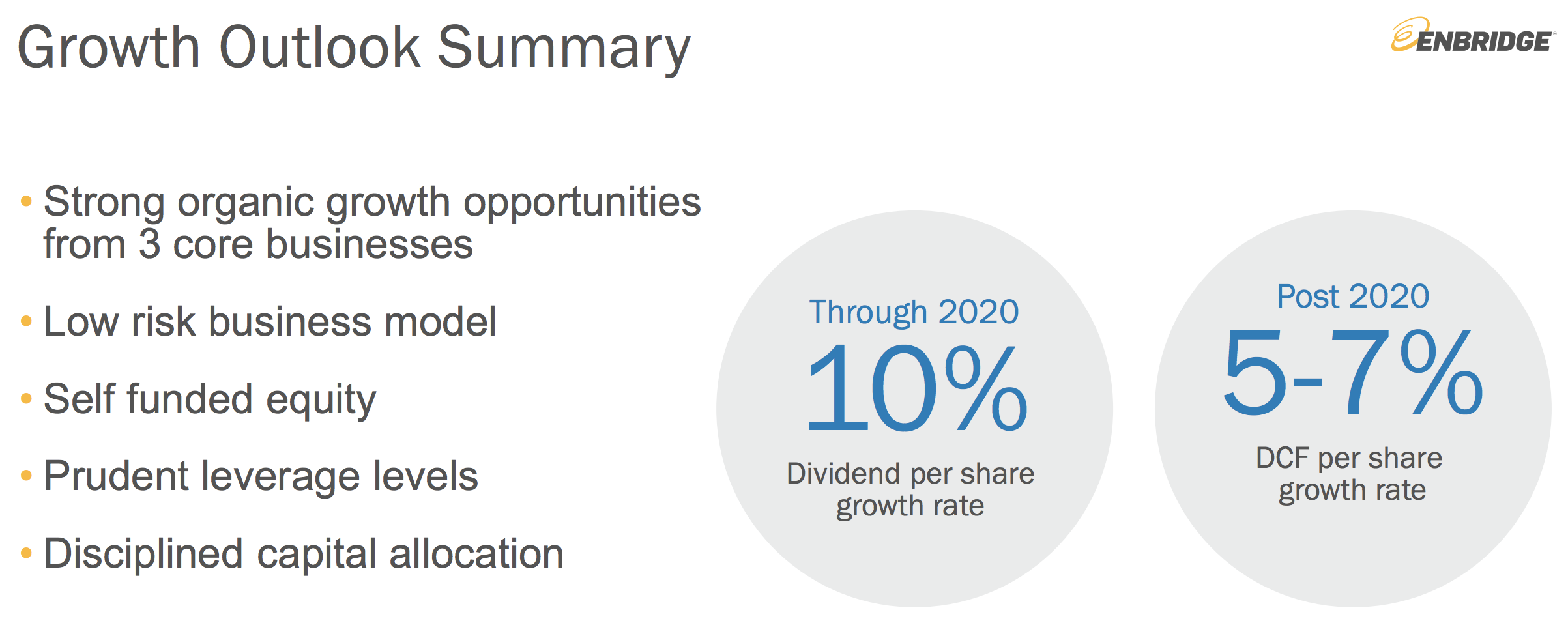

The court's decision comes after Enrbidge already announced a 1-year delay on the $6.8 billion project that was at the core of its plan to grow its dividend 10% in 2020 and self-fund long-term cash flow growth of 5% to 7% per year.

Shares of Enbridge have slumped nearly 7% since that ruling, while most midstream stocks and MLPs have recorded gains and the S&P 500 has increased about 5%.

With Enbridge's dividend yield exceeding 6%, well above its 5-year average yield of 4%, let's review what this latest setback could mean for the company's dividend safety and growth profile.

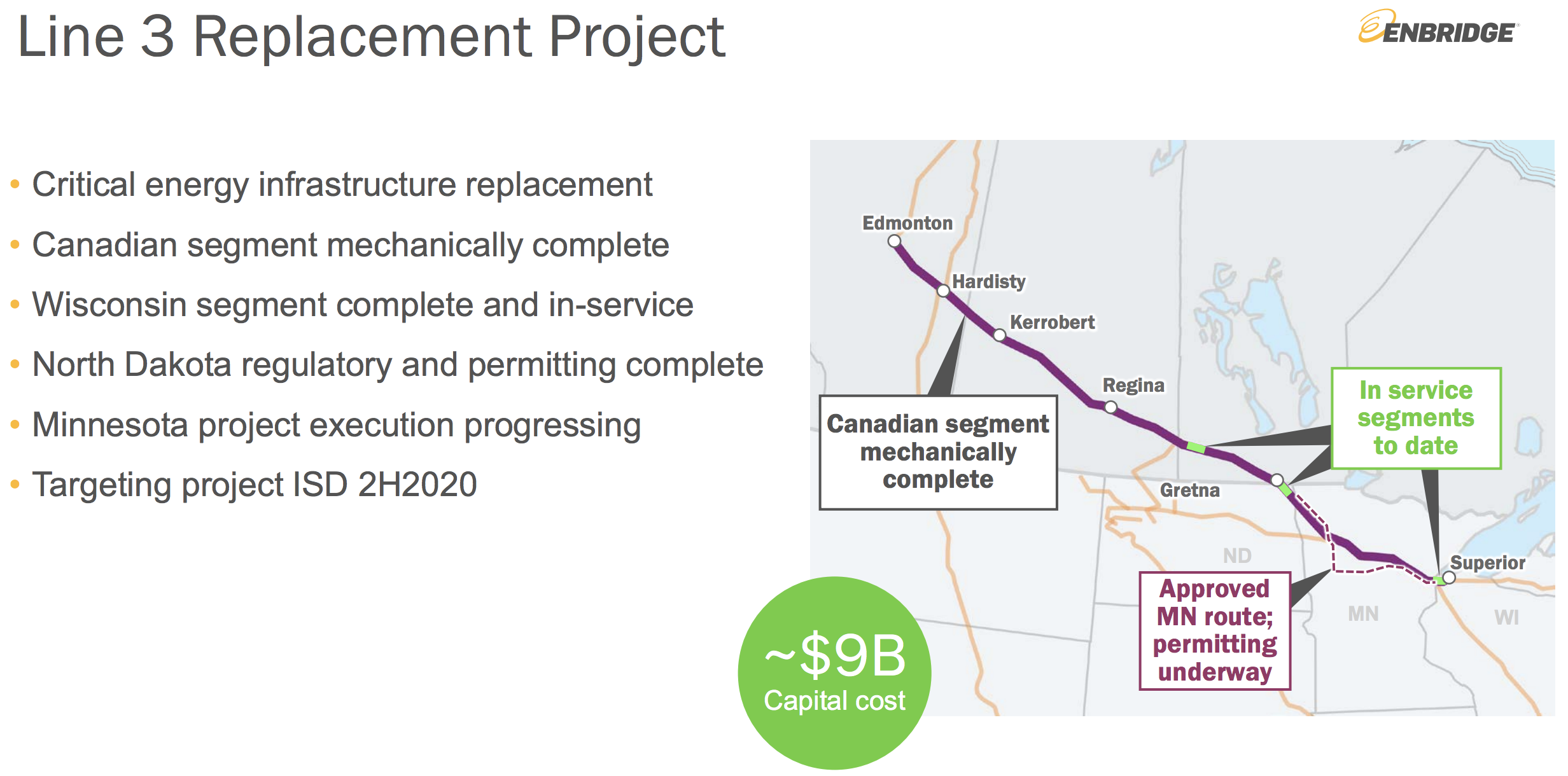

Line 3 is Crucial to Enbridge's Long-Term Growth Plans Line 3 is an oil pipeline that originally had 760,000 barrels per day of capacity, connecting crude from Canada to pipelines that head to the U.S. Gulf Coast. However, due to aging, Line 3 has carried steadily less crude from Alberta, Canada, through Minnesota since the 1960s.

Source: Enbridge Investor Presentation – Figures in CAD

The replacement project Enbridge started in 2017 would allow the firm to double the pipeline's current oil capacity back to its original 760,000 barrels per day amount.

Which is why Enbridge has spent the last five years running a complex regulatory gauntlet of local, state, and Federal regulators and endless legal challenges by environmentalists.

Source: Enbridge Investor Presentation

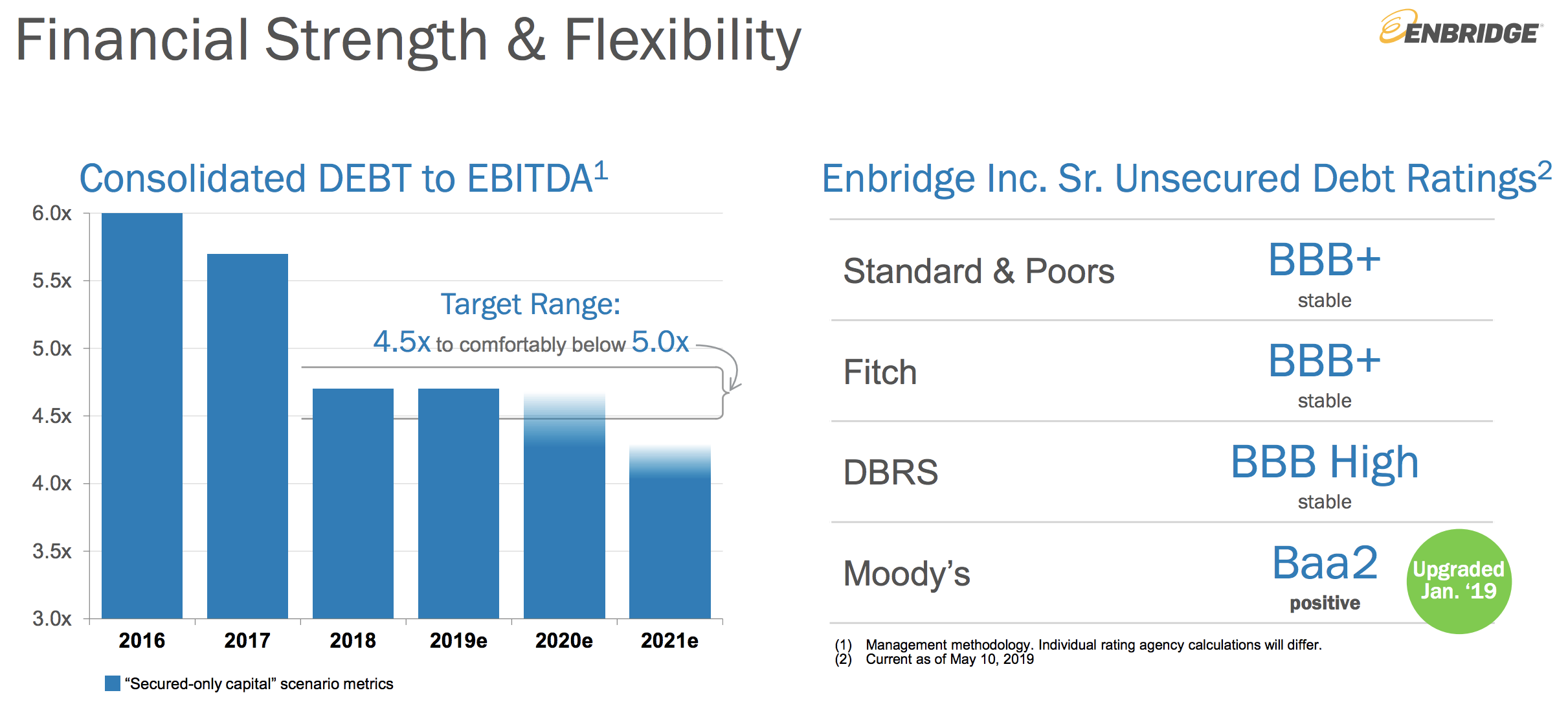

Completing its current growth backlog has been at the heart of Enbridge's efforts to deleverage its balance sheet, including achieving a debt/EBITDA ratio of about 4.5 or less by the end of next year (down from 6.0 in 2016).

Source: Enbridge Investor Presentation

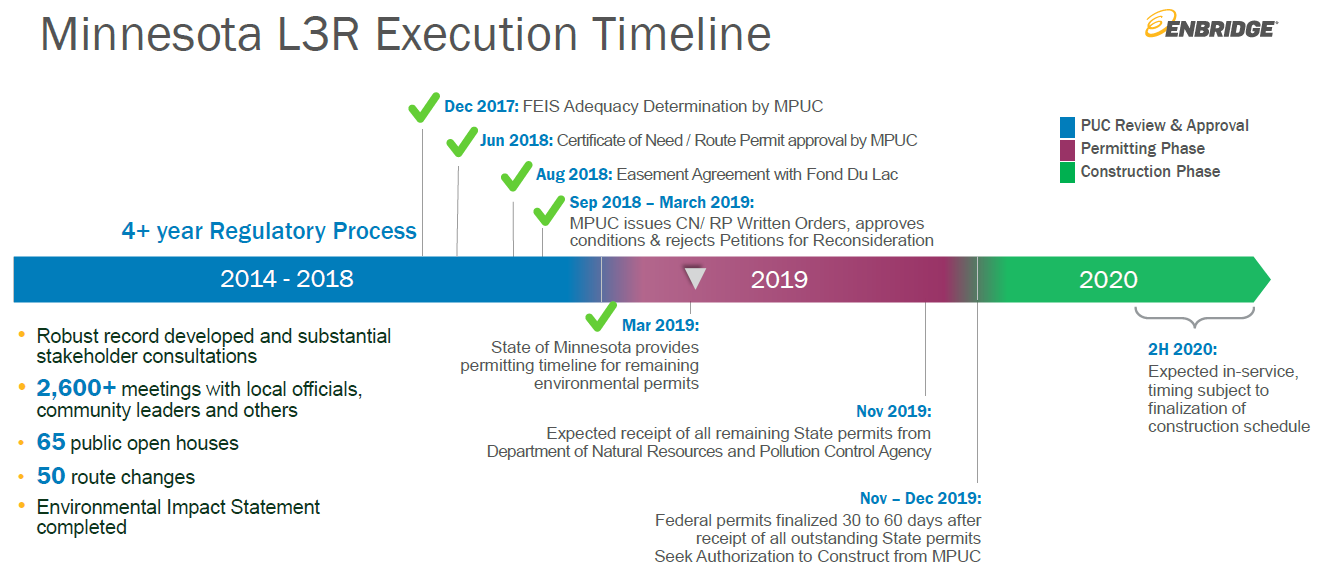

However, without Line 3 being completed on the current timetable (originally scheduled to be finished by the end of 2019, then pushed back to the second half of 2020 by management in March 2019), the firm's deleveraging goal will become difficult to achieve.

The company's current guidance calling for a final 10% dividend hike in 2020, with 5% to 7% annual dividend growth thereafter, would also become more challenging to meet.

Source: Enbridge Investor Presentation

The Minnesota Public Utility Commission, or PUC, previously granted permission to not only construct a more controversial section of the Line 3 pipeline, but unanimously agreed that were was a pressing need for the project.

However, several environmental groups, as well as three Native American tribes who own land the project is scheduled to be built on, sued to overturn the PUC's ruling. On June 3, the Minnesota Court of Appeals ruled that the 3,000-page environmental impact study the company had submitted to the PUC was insufficient, especially the review's treatment of a future potential oil spill near Lake Superior.

Enbridge has the ability to appeal the decision to Minnesota's Supreme court, which has the right to not hear the case. Management has not yet indicated whether or not it plans to take that route. Here's what the firm stated in its latest investor presentation published on June 5:

"Enbridge is currently in the process of a detailed analysis of the court’s decision and will consult with the Minnesota Public Utilities Commission (MPUC) and other state agencies about next steps. At this time, and until we have further clarity and alignment on the next steps for the regulatory, permitting and legal process, Enbridge is not in a position to assess the implications to the project’s previously guided in-service date window of 2H20."

Prior to this news, management's last update on Line 3 was that the previously expected delay in state permits would delay Federal permits and cause the project to be completed by the second half of 2020, a year later than expected.

That delay wasn't expected to affect 2019 guidance but would impact 2020, though management didn't offer specifics of when construction for this final segment of the project would begin.

Investors may fear that this latest blow to Line 3 may cause the project to be canceled entirely because it calls into question the pipeline's route and certificate of need.

In such an event, Line 3 would join the ranks of other major pipelines that have been torpedoed by various courts, including Kinder Morgan's Trans Mountain pipeline, TC Energy's Keystone XL pipeline, and Enbridge's abandoned Northern Gateway project.

However, as frustrating as yet another delay may be for shareholders, Enbridge's ability to deliver safe and moderately growing dividends likely hasn't been impaired by this most recent court action.

Line 3's Setback Doesn't Alter Enbridge's Dividend Safety But Could Reduce Size of Future Dividend Increases Headlines surroundingcourt rulings like this can sound far scarier than they are in reality. For example, as Minnesota Public Radio explains, the court's ruling wasn't entirely terrible news for Enbridge:

"The court also upheld the majority of the more than 3,000-page environmental impact statement. It also rejected most of the arguments made by pipeline opponents, including their contention that the study didn't sufficiently take into account the climate impacts of the pipeline, and didn't adequately analyze impacts on tribal cultural resources... Supporters of the project say they're heartened that the court upheld the majority of the environmental study's findings." – Minnesota Public Radio

The key fact supporting Enbridge's ability to eventually complete Line 3 is that the Minnesota Court of Appeals rejected the main arguments opponents of the pipeline were hoping would invalidate the entire environmental impact study.

As Kevin Pranis, marketing manager for the Laborers International Union of North America (which is helping build the pipeline), explained:

"While no one likes further uncertainty, what's important is the court reaffirmed on numerous counts that the [Public Utilities] Commission acted correctly... They rejected unanimously nearly all the arguments that were made against it." – Kevin Pranis

However, the ruling does mean that the environmental review will need to be amended, with a more aggressive plan for dealing with any future oil spills. And as Minnesota Public Radio notes, this will take at least six months but possibly longer (as many legal and regulatory requirements do):

"An addition to the regulatory process could take another six months or longer. And the company still needs several state and federal permits before it can break ground on the project in Minnesota." – Minnesota Public Radio

So Line 3's completion is now likely delayed by at least half a year and possibly much longer, pushing the project's timetable into 2021. The good news is that it now appears as if the Court of Appeals thinks Enbridge only needs to check a few more boxes before the PUC's previous approval of this section of the pipeline can be legally valid.

In other words, the project is far from dead, and Enbridge's long-term dividend growth story should have no trouble continuing, even if the magnitude of its dividend increases in 2020 and 2021 is less than management originally hoped.

Of course, that assumes this is the final setback the company will face over Line 3, which isn't guaranteed. The same groups who filed this claim are now considering filing an appeal over the rejection of most of their major claims (specifically regarding climate change). Joe Plumer, an attorney for some of the affected Native American tribes, put it bluntly, "The fight to stop Line 3 is far from over."

Opponents of Line 3 will attempt to appeal the rejection of most of their claims to the state Supreme Court, in an attempt to completely invalidate the company's environmental impact study, and thus force the project to begin its permitting process from scratch (in Minnesota).

However, as we discussed in March, even if the worst-case scenario played out and Enbridge was forced to cancel Line 3 entirely, the firm's dividend would likely remain secure.

No matter what happens with this large project, the company should continue to enjoy a predictable business model based on long-term, volume committed, and contracted cash flow in regulated industries.

With 98% of EBITDA generated from take or pay, fixed fee, and/or regulated activities, plus 93% of cash flow from investment grade counterparties (including regulated utilities), Enbridge is able to deliver steady cash flow to support its dividend no matter what oil prices or the economy is doing.

Source: Enbridge Investor Presentation

Importantly, management also targets a conservative 60% to 65% payout ratio as part of the firm's self-funding business model. As a result, Enbridge's growth potential and financing needs have no exposure to volatile equity markets.

While the outlook for 2020 has become fuzzier, on June 5 management reaffirmed expectations for Enbridge to have self-funded growth opportunities of $3.8 billion to $4.6 billion per year beyond 2020.

Source: Enbridge Investor Presentation – Figures in CAD

Over half (about $2.6 billion) of this self-funding capability was previously expected to come from Enbridge's retained cash flow after paying dividends and covering its maintenance capital needs. The remainder represents the firm's debt capacity.

With a BBB+ credit rating from Standard & Poor's (tied for the highest in the industry), Enbridge enjoys relatively low borrowing costs that should allow the firm to comfortably use debt to augment its retained cash flow.

In other words, even if the Line 3 Replacement Project was scrapped, Enbridge appears to have plenty of financial firepower to continue paying its dividend without jeopardizing the firm's ability to invest in other growth opportunities, assuming it continued to have access to credit markets.

The majority of Line 3's replacement costs have also yet to be incurred, so it seems unlikely Enbridge is in a position where it could be exposed to a huge loss from capital it has already spent that will no longer earn a return.

It's worth noting that the firm has faced similar challenges in the past, too. In the mid-2000s, for example, Enbridge had lined up a $6.1 billion project to build a pipeline from Alberta's oilpatch to a port in British Columbia.

Known as the Northern Gateway pipeline, this project was postponed numerous times before ultimately being scrapped due to a change in federal regulations that killed the market opportunity.

As of December 2018, Enbridge said it was still out around $300 million in lost costs for the canceled project. However, this event did not stop the company from continuing to reward shareholders with predictable dividend growth each year, even with a business model that was not self-funded during that time.

While the latest Line 3 setback is certainly frustrating for long-suffering shareholders and creates some additional uncertainty, Enbridge's dividend appears to remain safe, and the firm's long-term outlook looks mostly intact.

The company's dividend could experience a slower pace of growth these next few years, but the stock's 6% yield helps provide some compensation for investors who are willing to remain patient.

Concluding Thoughts It can certainly be frustrating when important pipeline projects face setbacks like this. Execution on ambitious growth backlogs is usually among the biggest medium-term risks to midstream firms like Enbridge, and as we've seen, there are often a number of uncontrollable factors at play.

However, it's important to remember that Enbridge has been around since 1949 and has an impressive long-term track record of creating value for shareholders. Occasional project setbacks are par for the course and baked into the industry's risk profile.

Even if Enbridge is ultimately forced to abandon the Line 3 Replacement Project, the firm's solid financial health, stable cash flow profile, and self-funded business model mean that its dividend would likely remain safe and merely grow at a slightly slower rate than expected.

Fortunately, the actual ruling by the Minnesota Court of Appeals doesn't appear to make a total project cancellation likely. Instead, the final completion date is likely postponed by another six to 18 months. As always, we will continue monitoring the situation and provide an update if any new material developments occur.