News broke last night that the U.S. will impose a 5% tariff on all Mexican imports beginning on June 10 unless Mexico agrees to do more to address illegal immigration problems.

The tariff will increase 5% each month, reaching a maximum of 25% in October. Trump tweeted the 25% level would hold there "until Mexico substantially stops the illegal inflow of aliens coming through its territory."

General Motors (GM) saw its stock price fall over 4% this morning. Most U.S. automakers source many of their vehicles and parts from Mexico, so import tariffs threaten to raise their cost of production and disrupt their supply chains, especially depending on how Mexico's government responds.

The Wall Street Journal provided an excellent summary of various automakers' exposure to Mexico. Cars built in Mexico accounted for about 17% of the combined 2018 sales of GM, Ford, and Fiat Chrysler.

Citing an estimate from research firm LMC Automotive, the Wall Street Journal noted that General Motors has among the highest exposure to Mexico, with roughly 22% of its domestic sales generated from Mexico-built vehicles.

For comparison, approximately 18% of Fiat Chrysler's U.S. sales were imported from Mexico, and only 10% of Ford's domestic revenue is traced to Mexican imports.

So how bad could this news be for GM's outlook, and is it possible that the firm's dividend could eventually be threatened?

Investment banking advisory firm Evercore ISI estimates the initial 5% tariff could reduce annual earnings by up to 10% for GM and Fiat Chrysler.

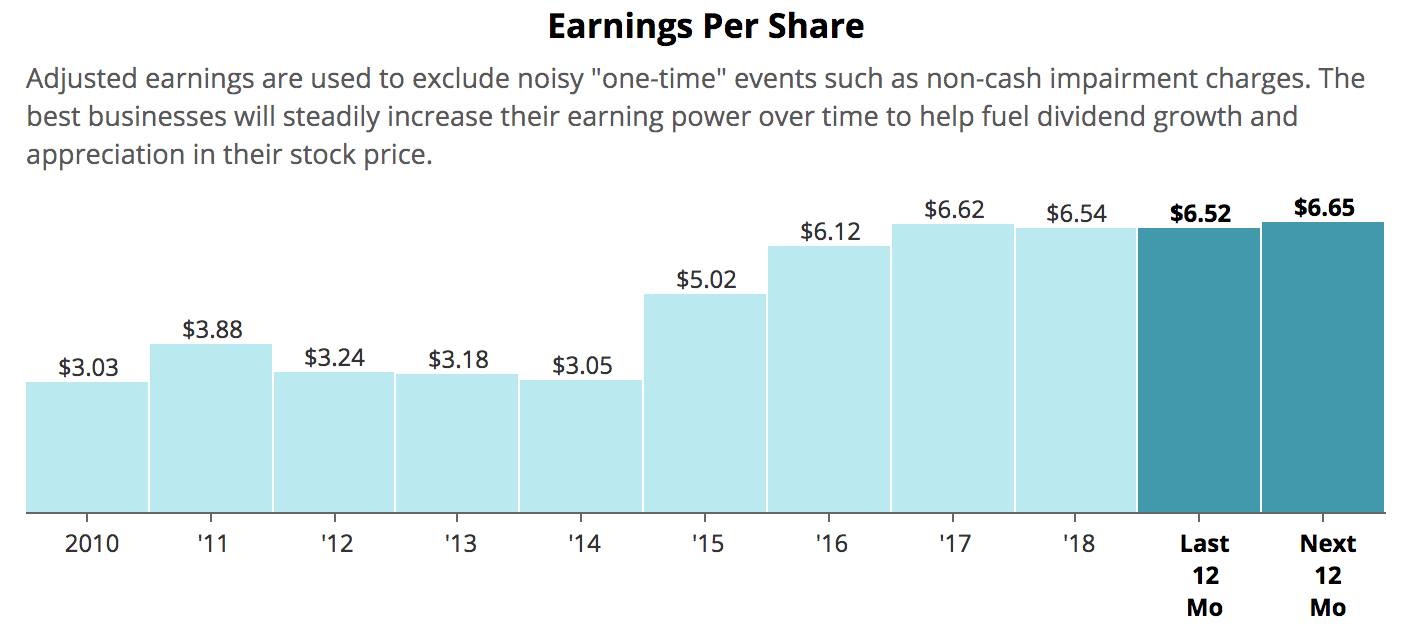

A 10% drop is a big number, but GM's current annual dividend of $1.52 per share would remain very well covered by its earnings over the next year, which were estimated at $6.65 per share prior to this development. The company's earnings would need to fall by nearly 80% to no longer cover the dividend.

Source: Simply Safe Dividends

The story is similar from a cash flow perspective. Last month GM issued 2019 guidance calling for adjusted automotive free cash flow of $4.5 billion to $6.0 billion, well above its estimated dividend payments of $2.5 billion even if a large haircut is applied to profits due to tariff escalations.

GM's vehicle financing business is on pace to add another $1 billion or so to profits this year, though that amount will largely be offset by operating losses in the firm's self-driving vehicle division.

While tariffs are certainly a big deal for automakers' short-term profits, global demand for the vehicles is arguably even more important. The high-ticket price tag of trucks and cars, plus the ability to stretch out the life of most used cars, means demand is sensitive to the financial health of consumers.

In other words, new vehicle sales typically plunge during recessions. Combined with the capital-intensive nature of production factories, profits earned by GM and its rivals can quickly be zapped any given year when industry downturns occur.

Fortunately, GM has done its best to proactively prepare for such a situation. Management has exited or significantly restructured low-return or unprofitable businesses, and in November 2018 the firm announced a new restructuring plan expected to save $6 billion annually by the end of 2020 (at a cash cost of $2 billion).

Most importantly, GM continues to maintain an excellent balance sheet, supporting its ability to continue investing in its future while also maintaining a steady dividend.

At the end of March 2019, GM held $15.8 billion in cash and had access to an additional $16.8 billion via its credit facilities. Standard & Poor's believes that even despite its restructuring costs GM "will avoid borrowing from its main $16.5 billion revolving facility for an extended period because it views that revolver as a backstop in case of unforeseen events, such as a severe industry downturn."

Despite its cyclicality, the company's solid financial health earns it an investment grade BBB credit rating. Based on what we know today, tariff escalations and even an inevitable industry downturn seem unlikely to shake GM's foundation or dividend.

With that said, GM certainly isn't for everyone. The stock price will almost certainly get whacked, likely significantly, whenever the next recession happens. Given the company's cyclicality and need to invest in electric cars and autonomous vehicles, GM's dividend will likely remain frozen as it has since 2016, too.

Besides its high dividend yield (currently about 4.5%), the main appeal of GM is its exposure to self-driving vehicles through GM Cruise, the self-driving vehicle business GM bought in 2016 for $1 billion.

Cruise secured an additional $1.15 billion investment in early May, bringing its valuation to $19 billion. Cruise has not disclosed its ownership structure following this deal, but GM seems likely to own around 60% to 70% of the company based on prior investments by SoftBank ($2.25 billion in May 2018 for a 20% stake) and Honda ($2.75 billion in October 2018 for a 5.7% stake).

While no one knows how driverless cars and ride services will ultimately play out, GM's stake in Cruise was likely valued at around $12 billion in the latest funding round based on our ownership estimation (65% of $19 billion).

That's an especially big number compared to GM's $47 billion market cap (note the company also has $15 billion in net debt). The market appears to be assigning little value to the $6 billion-plus average annual free cash flow that GM's automotive and financial businesses have generated in recent years, perhaps due to fears of an imminent industry downturn.

Regardless, GM seems likely to remain a cash cow over a full industry cycle while continuing to pay dividends and invest in the future, even if tariff wars escalate. The market does not appear to be giving the company much credit for anything more than that.

GM's stock will probably continue requiring patience to own, not to mention a stomach for some volatility. Issues such as tariffs and commodity price fluctuations will come and go, but the company needs to show investors it can manage its business well during the next recession while developing Cruise into a more substantial long-term earnings driver.