Bayer's Dividend Safety Downgraded in Light of Mounting Liabilities

Shares of Bayer (BAYRY) have slumped nearly 50% over the past year. The German manufacturer of chemicals and pharmaceuticals has remained under pressure following its June 2018 acquisition of Monsanto for $63 billion.

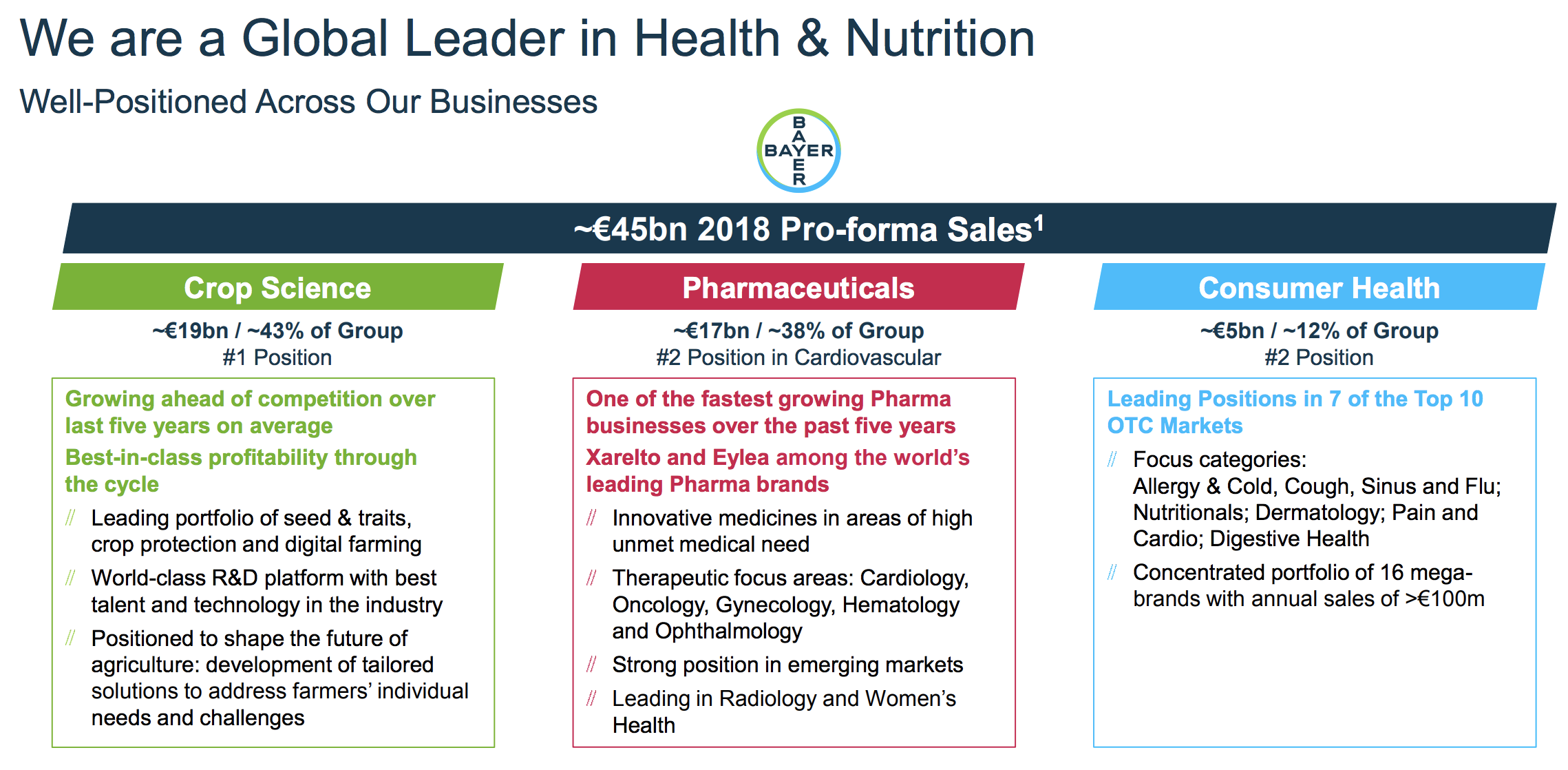

Buying Monsanto made Bayer the world's largest seed and crop-chemical business, according to The Wall Street Journal. The firm's agriculture business shot up from 22% of 2016 company-wide revenue to 43% in 2018.

Citing Morgan Stanley estimates, The Wall Street Journal stated that the combined business would sell roughly 28% of the world's pesticides, about 36% of U.S. corn seeds, and 28% of soybean seeds.

Source: Bayer Investor Presentation

Unfortunately, just months after closing the transaction, problems began to arise with Monsanto's popular weedkiller product Roundup.

Over the last 10 months, three U.S. juries have found the herbicide to cause cancer, including a ruling earlier this week that awarded over $2 billion to a couple who used the product on their property.

Bayer is appealing each of these verdicts and continues to claim Roundup is safe to use. However, investors have grown increasingly concerned about the potential liabilities the firm could incur from Roundup. After all, the company still faces 13,400 total plaintiffs.

In a statement released earlier this week, Bayer said it would fight these rulings, citing the U.S. Environmental Protection Agency's April 2019 reaffirmation that glyphosate-based products such as Roundup can be used safely and are not carcinogenic:

Bayer is disappointed with the jury's decision and will appeal the verdict in this case, which conflicts directly with the U.S. Environmental Protection Agency's interim registration review decision released just last month, the consensus among leading health regulators worldwide that glyphosate-based products can be used safely and that glyphosate is not carcinogenic, and the 40 years of extensive scientific research on which their favorable conclusions are based.

Per Reuters, Bayer hopes to use a "silver bullet defense". Specifically, under "the legal doctrine of preemption, state law claims are barred if they conflict with federal law." In other words, management hopes the EPA's federal ruling will protect the firm from state law claims.

No one knows how this battle will play out, but over $40 billion of market value has already been wiped out from Bayer's stock price decline. Investors are clearly concerned the company will be on the hook for substantial damages, and confidence in management has eroded with its major acquisition going awry.

What does all of this mean for Bayer's dividend safety? Until more is known, given the high stakes of this situation, we are downgrading Bayer's Dividend Safety Score from the low end of our Borderline Safe category to Unsafe. Here's why.

First, the potential liability from Roundup litigation continues to balloon. Bloomberg analysts have increased their estimated settlement value to as much as $10 billion, up from a prior peak of $6 billion.

Meanwhile, credit rating agency Moody's is evaluating scenarios with settlement values ranging from $5.5 billion to $22 billion.

To put these figures in perspective, Bayer expects to generate $3.4 billion to $4.5 billion in 2019 free cash flow. Bayer pays an annual dividend that consumed approximately $2.9 billion this year.

In other words, just $0.5 billion to $1.6 billion of free cash flow is expected to be retained in 2019, an insufficient amount to cover a potentially large settlement while also deleveraging the balance sheet.

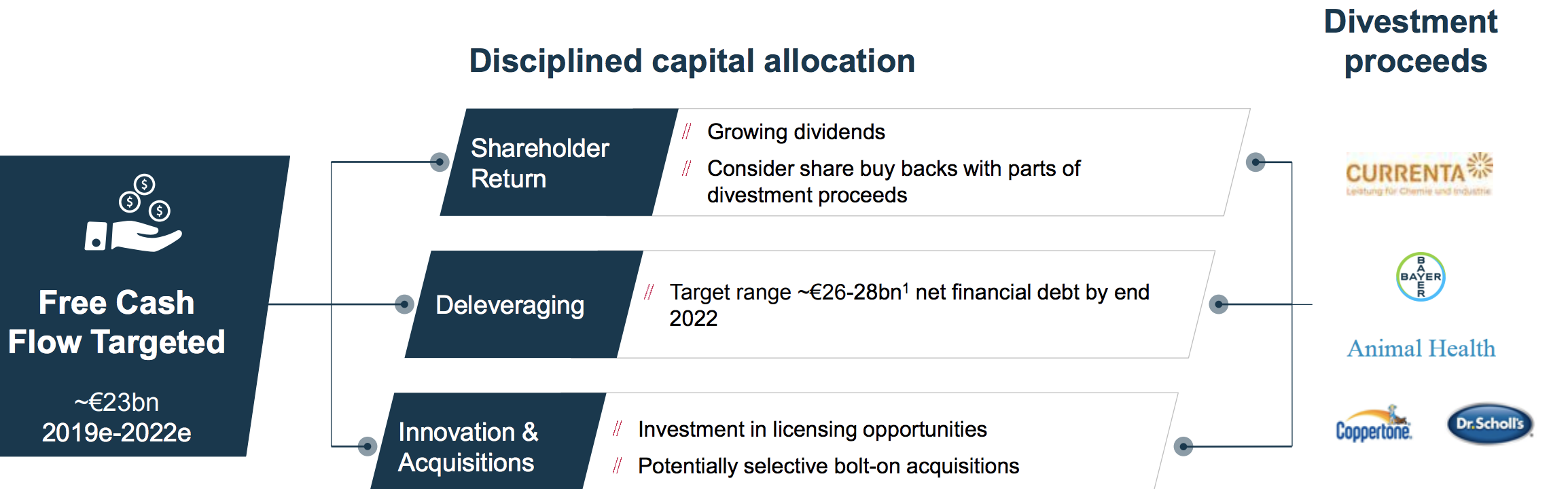

Bayer's net debt load ballooned to $40 billion following its acquisition of Monsanto. Management wants to reduce debt by around $10 billion by the end of 2022, with hopes of eventually improving its credit rating from BBB to A.

From 2019 through 2022, Bayer estimates it could generate $26 billion in free cash flow, with results steadily improving as the combined company realizes merger synergies and expands its business.

Source: Bayer Investor Presentation

However, herbicides, which include Roundup, accounted for 14% of Bayer's first-quarter 2019 revenue. It's hard to say if management's guidance could still be attained if health and safety concerns mount against these products.

Regardless, if the firm delivers on its guidance and its dividend remains frozen during this period, Bayer's dividend would consume roughly $11.6 billion of the $26 billion in free cash flow it generated, leaving close to $15 billion of free cash flow available.

If a Roundup settlement costs the company $10 billion, especially if it needs to be paid out sooner rather than later and asset divestitures take longer than expected, then Bayer could struggle to deleverage as quickly as it hopes to.

Moody's has also said that while Bayer could likely absorb a hypothetical $5.5 billion settlement under its current rating category, a $22 billion payout could affect its rating.

Simply put, this is a tricky situation to analyze, especially as an income investor.

On one hand, it's possible Bayer reaches a reasonable settlement that quickly takes this risk off the table. In that case, the firm's dividend could be maintained, and the company has a better chance of staying on track with its long-term growth and deleveraging plans. The stock's current valuation would look cheap, too.

However, if the situation continues to deteriorate and an even more substantial settlement or drawn-out litigation period begins looking likely, management could opt to reduce or even suspend the dividend in light of this uncertainty in order to conserve cash for a couple of years. That would help the firm more comfortably manage its high debt load and future liabilities.

While Bayer has paid dividends since 1952, the firm has cut its payout in the past. The company's last dividend reduction came in 2002, when it announced a 36% cut due to struggles across its pharmaceuticals business.

Since Bayer only pays a dividend once per year, and its 2019 payout was already made earlier this month (the 2019 dividend was held flat), management may not have to make a call on the firm's dividend until early 2020.

A lot can change between now and then, but based on what we know today, Bayer seems to be a more speculative income stock until its Roundup liabilities become clearer. Until then, the stock will likely remain quite volatile. While a worst-case outcome is very unlikely to doom the company, it would probably spell bad news for shareholders who own the business primarily for its dividend.

Income investors holding shares of Bayer should understand these rather binary risks and uncertainties, making sure they are comfortable with their overall portfolio diversification and position sizes.