Shares of 3M (MMM) have slumped 20% since April 24th, falling to their lowest level since early 2017. The stock's dividend yield now sits at 3.3%, a level not seen other than in 1995 and during the financial crisis.

Source: Simply Safe Dividends

Investors aren't giving 3M much credit for its long-term track record of creating meaningful shareholder value and growing its dividend for 61 consecutive years.

Let's take a closer look at this dividend king to understand why the market is so bearish on the company and if 3M's long-term outlook appears to remain intact.

Why 3M Shares are Under Pressure 3M's slump began on April 25th, when the firm announced disappointing earnings and cut guidance for its fifth consecutive quarter. The company's stock price fell 13% that day, its largest single-day percentage decline since Black Monday in 1987, when the S&P 500 fell over 20%.

A new CEO, Michael Roman, took over in July 2018. He has thus far failed to deliver on analysts expectations even once, causing many investors to question the credibility of the company's long-term guidance.

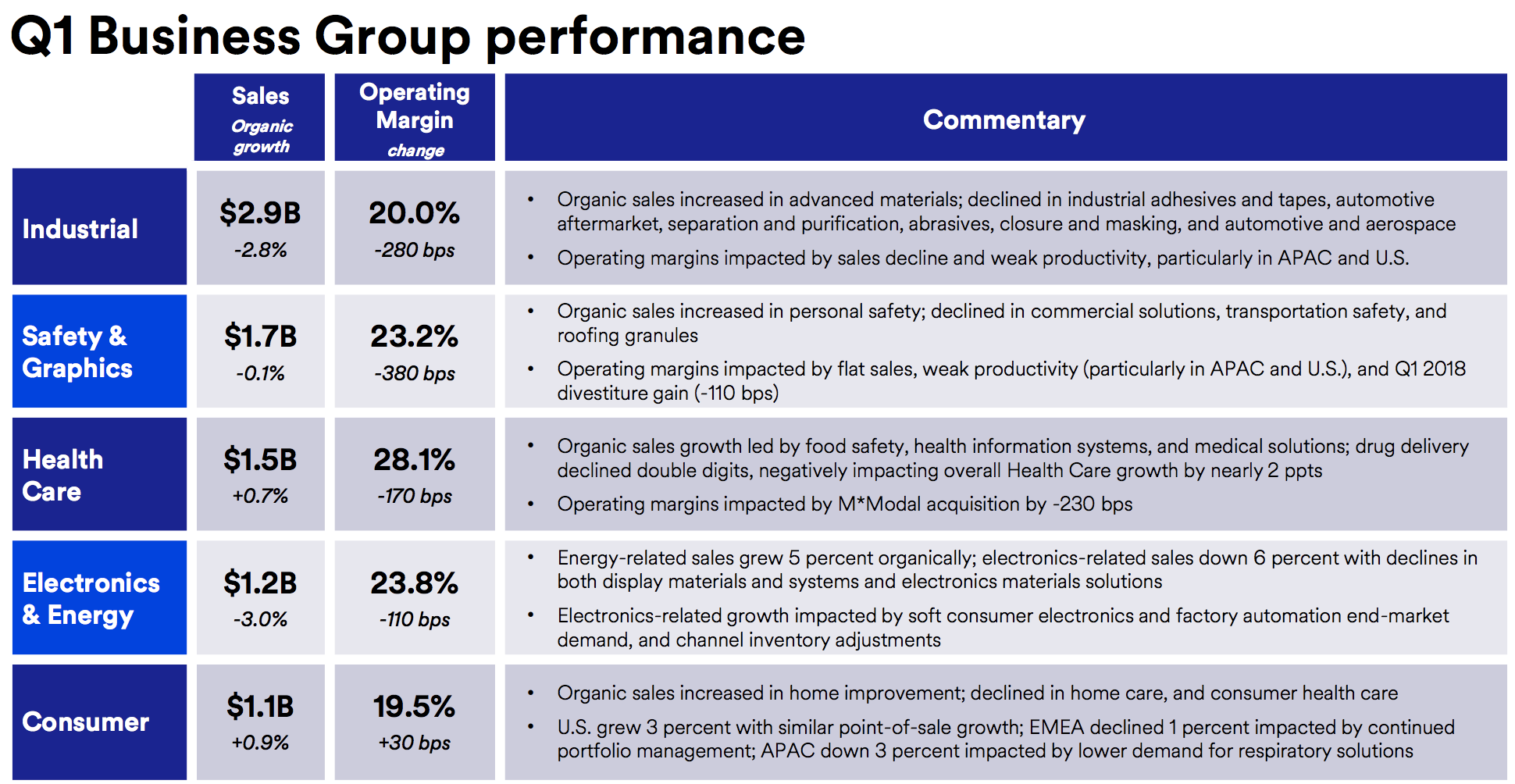

In the first quarter of 2019, 3M missed on both revenue and earnings growth expectations, reporting a 1.1% decline in organic sales and an 11% fall in adjusted EPS compared to the prior year period.

Management blamed a slowdown in certain markets, including China (organic sales down 3.6%), automotive, and electronics. Even in the U.S., where the economy appears to remain on solid ground, the company reported a 0.4% drop in organic sales.

Overall, the company reported first-quarter sales declines in four of its five segments and operating margin declines in three of them.

Source: 3M Earnings Presentation

The major cause of this was weaker sales in industrial products in the U.S. and China, and inventory problems resulting from management's insufficient response to the slowdown, resulting in relatively poor efficiency which CEO Michael Roman readily admitted to analysts during the earnings call:

"The actions we took were not sufficient to offset the broad-based softening we faced in those markets as the quarter progressed."

As a result of this softness, 3M reduced its 2019 organic revenue growth target to -1 to 2%, down from prior expectations for a 2% to 4% increase. Adjusted EPS guidance for the year was also slashed by 12% (flat growth versus 2018).

Besides the company's ongoing failure to meet guidance, two other news items help explain the company's weak share price.

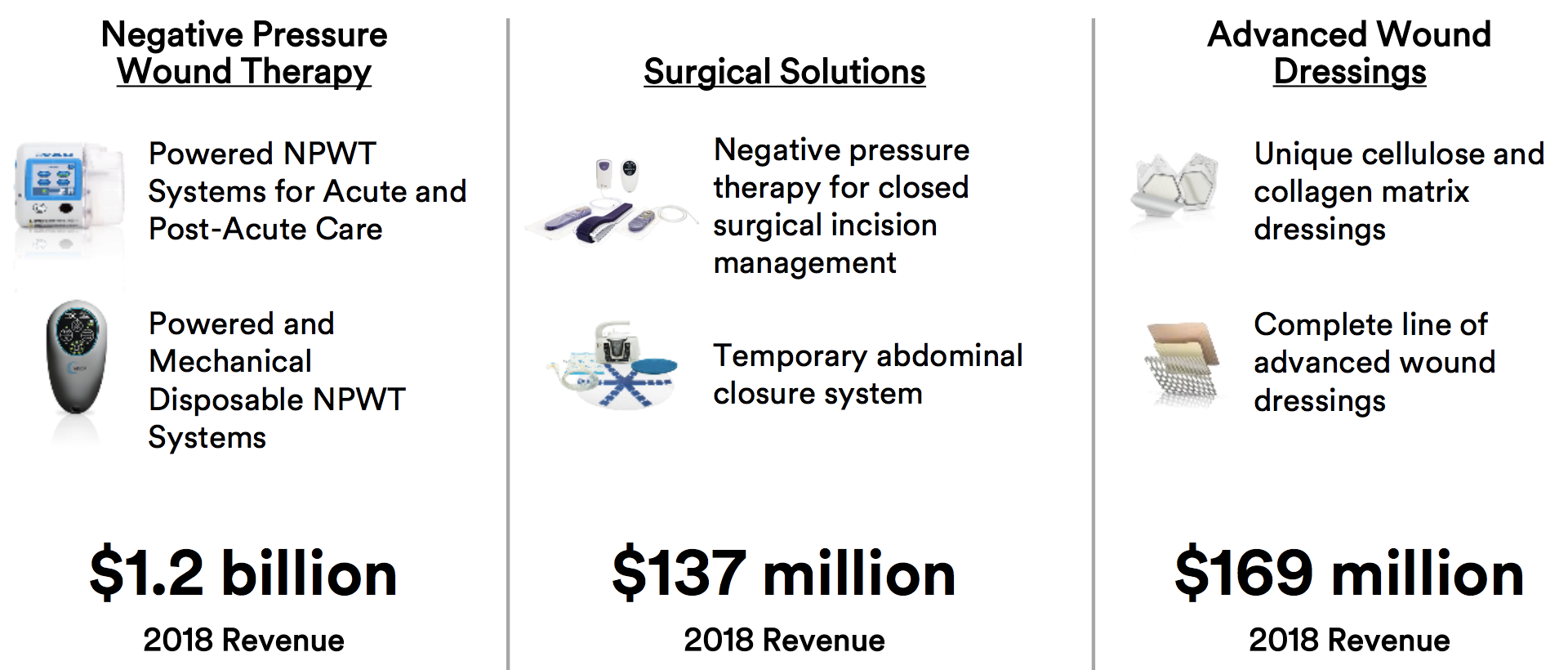

On May 2nd, 3M announced it was buying healthcare company Acelity in a $6.7 billion acquisition, the firm's largest acquisition ever. With investors not sold on the firm's relatively new CEO, plus the unusual growth challenges 3M is trying to address today, the deal's timing comes as somewhat of a surprise.

Acelity's Product Lines – Source: 3M Investor Presentation

Normally 3M's approach to M&A is to make small bolt-on acquisitions, including 12 deals totaling $7.7 billion between 2012 and 2018 (average of $640 million each). Big purchases up the stakes in terms of valuation and operational risks.

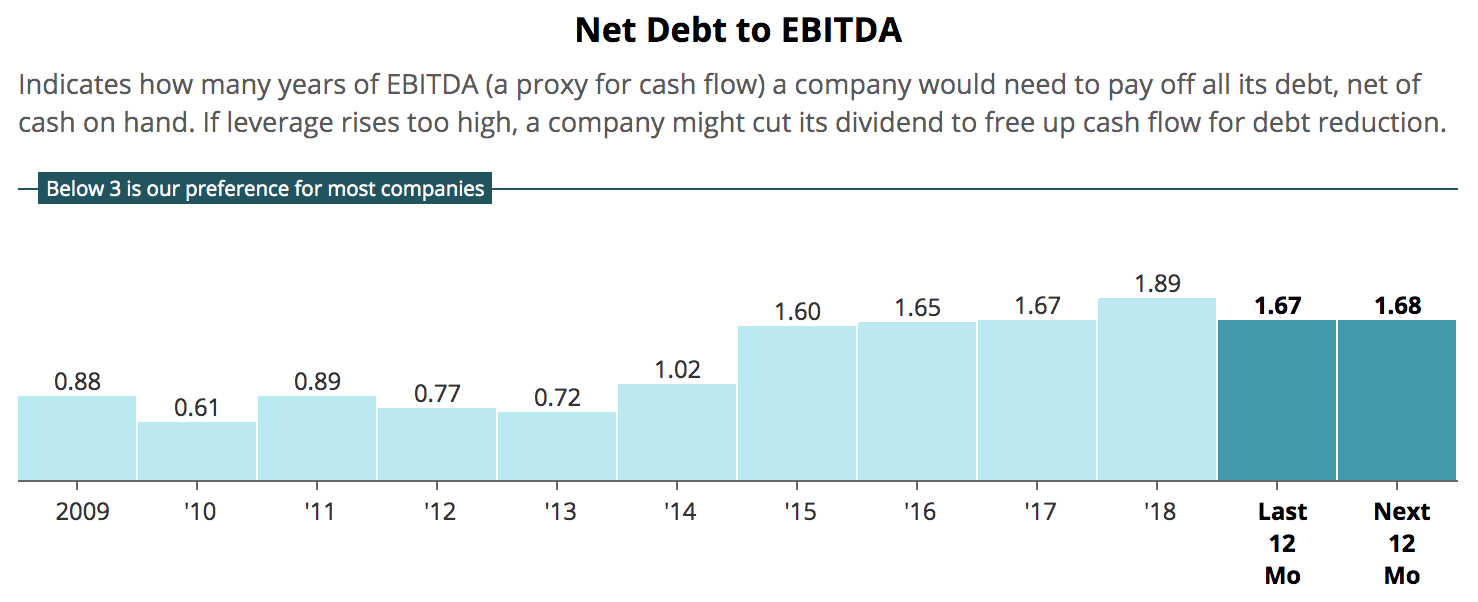

The Acelity acquisition is certainly large for 3M, and management has said it plans to fund the transaction with a combination of cash on the balance sheet ($3.5 billion) and debt. Assuming 3M wants to maintain at least a couple billion dollars of cash on hand, the firm could take on close to $6 billion in debt to close this deal in the second half of 2019.

Given that the company is paying a steep valuation multiple of 15x EBITDA (pre-synergies), 3M's net leverage ratio (net debt / EBITDA) will likely increase from 1.7 to around 2.2, the highest level in a decade, though still a reasonably safe level for most businesses that shouldn't jeopardize 3M's dividend.

Moody's has said that while it considers the extra debt a credit negative event, 3M's A1 credit rating (A+ S&P equivalent) will remain unchanged. The $6.7 billion Acelity acquisition is part of management's five-year capital allocation plan which involves potentially taking on $5 billion to $15 billion in more debt but still maintaining a net leverage ratio of 1.3 to 2.1 in 2023, about in line with the firm's recent ratio.

Source: Simply Safe Dividends

To accommodate this deal more comfortably, management lowered its 2019 share repurchase guidance to $1.0 billion to $1.5 billion, down from its previous $2 billion to $4 billion target. That's a strategic decision based on the extra debt being taken on to finance this acquisition, but it also means that 3M will be less able to take advantage of its beaten-down share price this year.

Besides disappointing earnings and fears over a pricy acquisition, which some see as a knee-jerk reaction by a struggling management team, 3M investors are also worried about escalating trade war fears.

On May 5th President Trump tweeted that China was attempting to walk back some of its earlier trade concessions, so the U.S. would be raising tariffs on $200 billion in imports from 10% to 25% on Friday, May 10th. He also threatened to impose 25% tariffs on $325 billion in additional imports (meaning virtually all Chinese imports into the U.S.) "shortly."

Sure enough, the tariffs went into effect today, and China has said it will retaliate. 3M is the 34th most trade sensitive U.S. company in terms of the percentage of revenue it derives from China (10% in 2018), according to FactSet Research and UBS.

Should the trade war last for an extended period of time, 3M could continue struggling to meet its guidance. Not only could its business in China remain under pressure, but Moody's Analystics estimates that such an event could subtract 1.8 percentage points from U.S. GDP growth.

Basically, 3M's share price has been battered due to a perfect storm of negative factors including a big earnings miss and guidance cut, worries over execution on its largest acquisition ever, and now a potential escalation of the U.S.-China trade conflict.

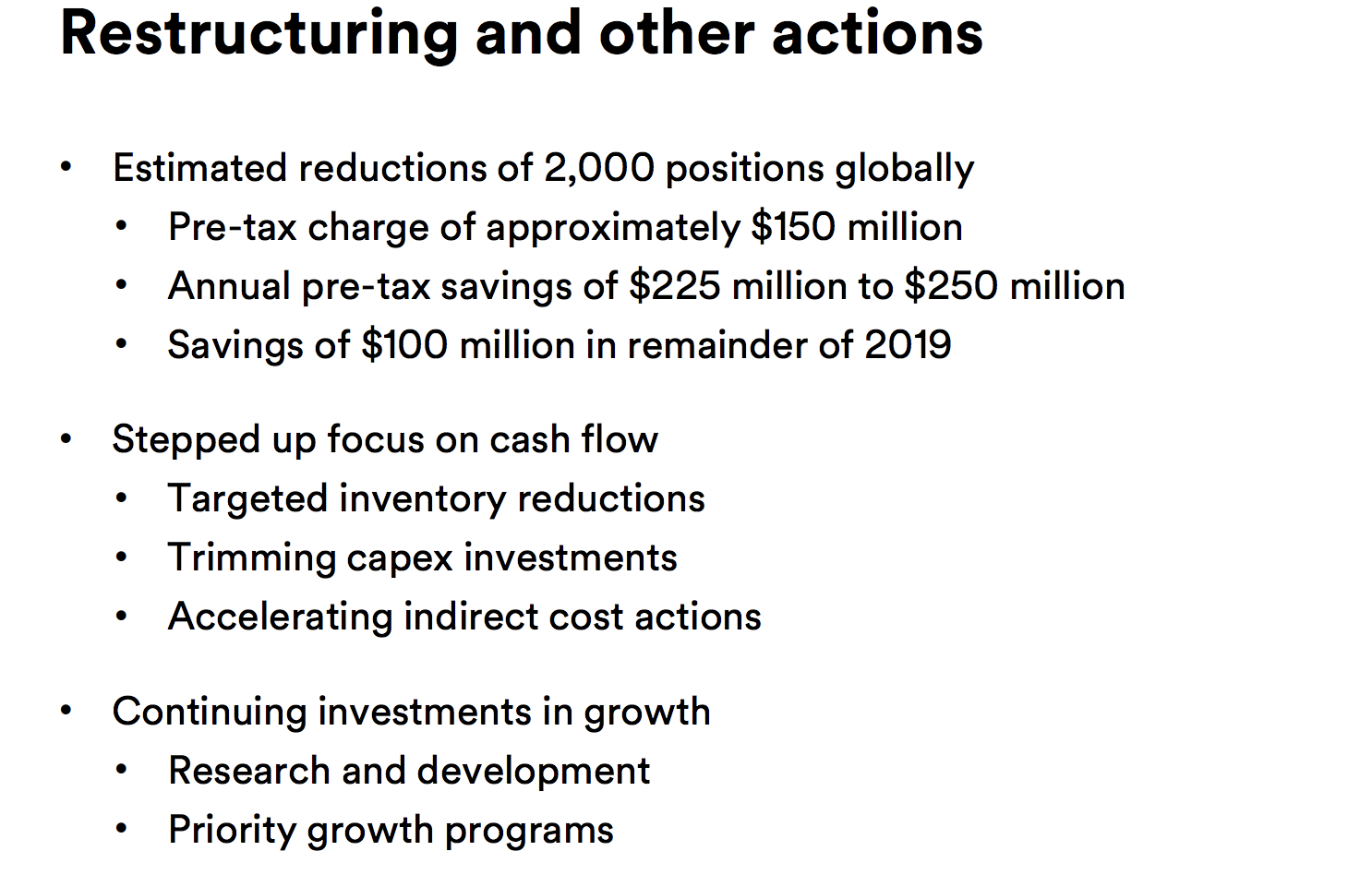

Let's review how management is responding to these events and assess how they could affect 3M's dividend profile and long-term outlook. 3M's Turnaround Plan and Long-term Outlook Management has already announced a new restructuring plan that entails cutting 3M's global workforce by about 2%, as well as new initiatives to improve inventory management and cut capex while still investing heavily into R&D programs.

Source: 3M Earnings Presentation

The firm is also restructuring its five business segments into four, which continues the company's historical precedent of streamlining segments (between 2012 and 2018 3M cut its number of business divisions from 40 to 23 and sold off 10 underperforming business units for $2.1 billion).

Source: 3M Earnings Presentation

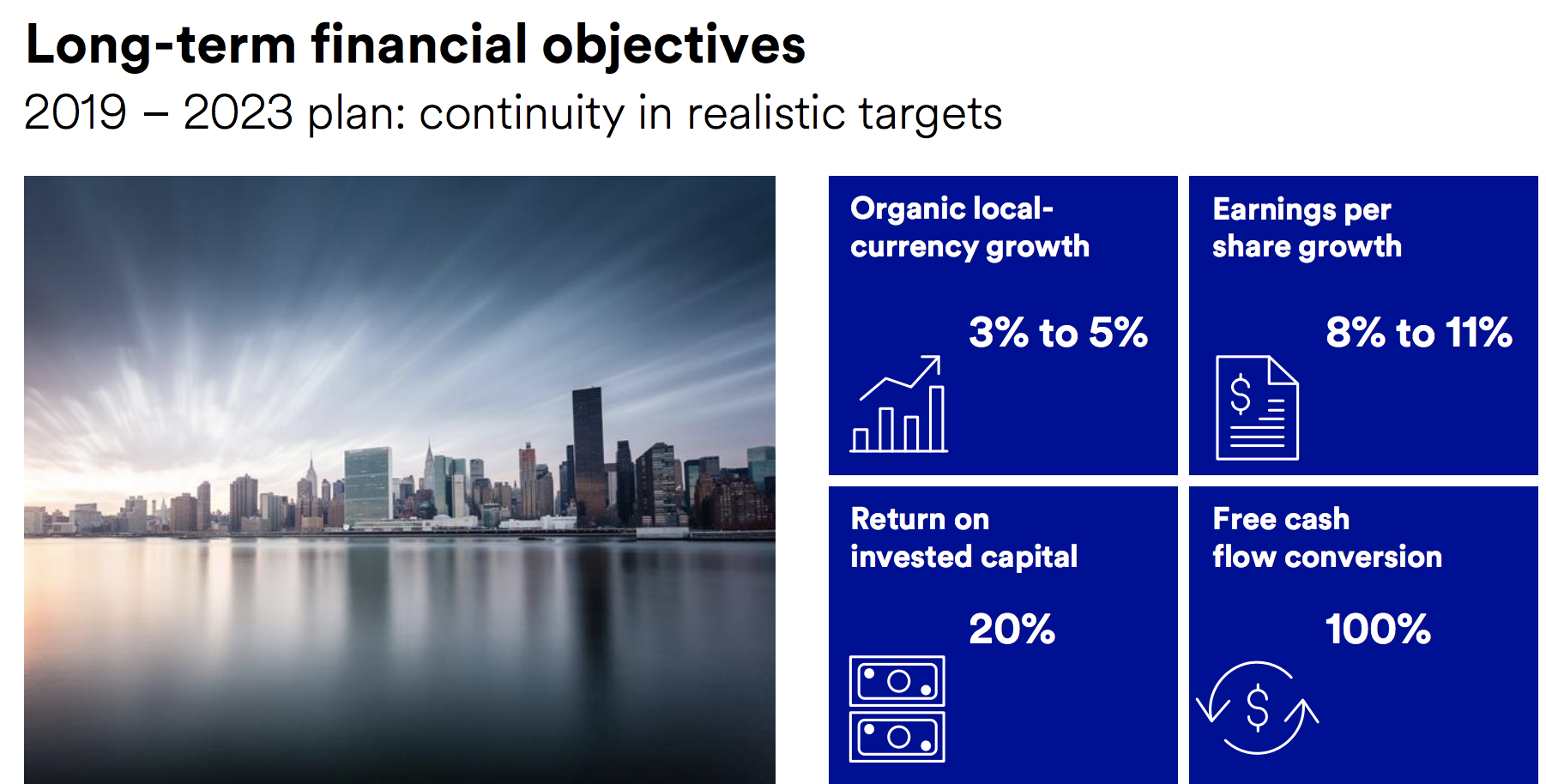

Management hopes this restructuring plan will keep 3M on track to deliver on the five-year growth plan it laid out in November 2018:

Source: 3M Investor Presentation

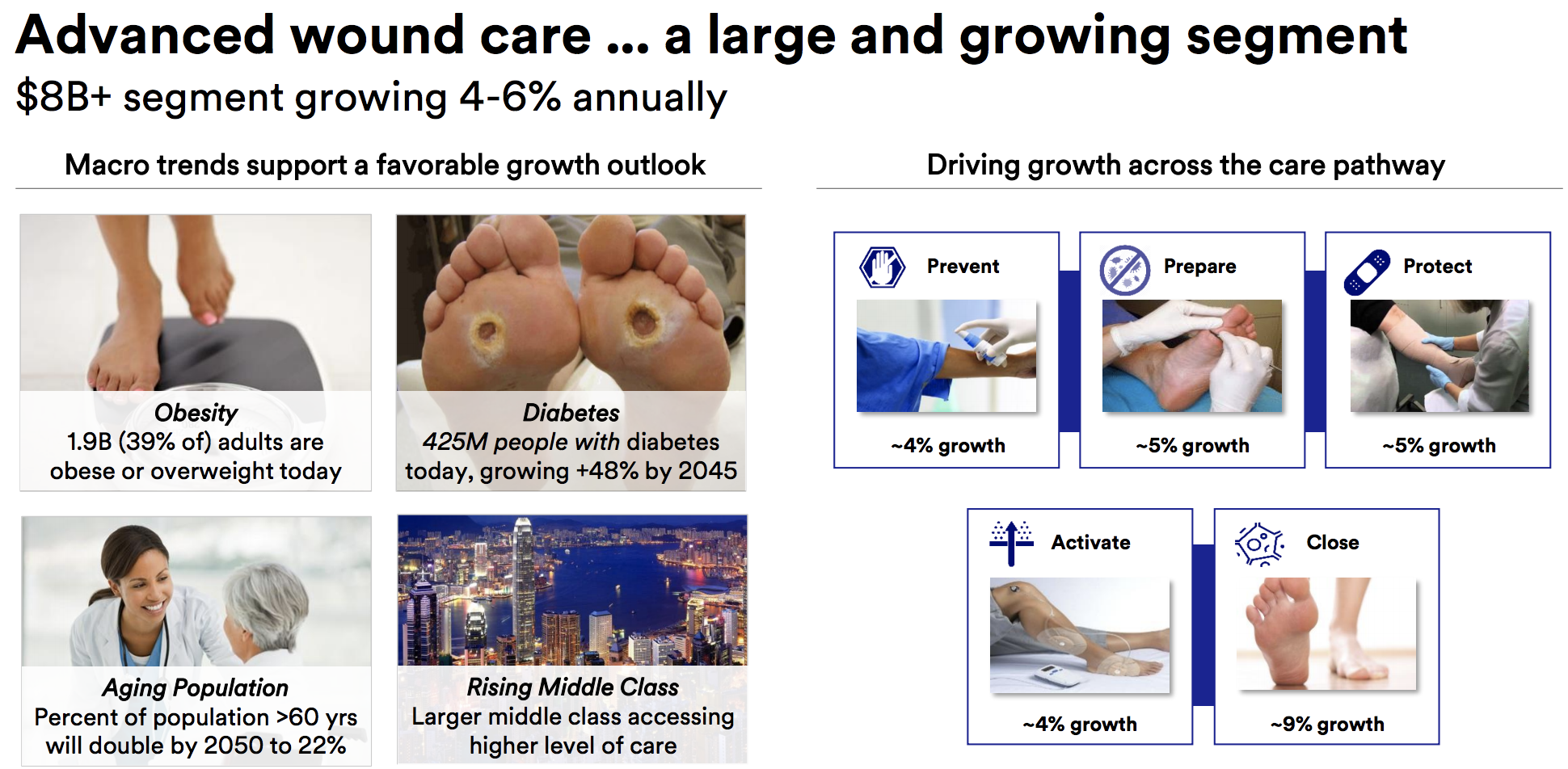

Squeezing benefits out of Acelity is expected to help meet those targets, too. Acelity commands about 70% market share in negative pressure wound care, which is part of an $8 billion global market that's growing about 5% per year.

Source: 3M Investor Presentation

Acelity had $1.5 billion in 2018 sales (about 5% of 3M's total revenue), with 10% revenue growth from continuing operations and 30% adjusted EBITDA margins. Management expects that within three years it will be able to achieve cost synergies alone worth 8% of Acelity's revenue.

Combined with revenue synergies (from using its distribution channel to boost sales), management expects this to be a profitable investment for shareholders. If everything goes as planned, the deal's multiple will fall from 15x EBITDA to 11x, a much more reasonable level.

Regardless, after a string of disappointing quarters, investors are questioning whether or not 3M has lost some of its magic. The firm's conglomerate business structure appears to have slowed management down by a step or two, and the company's plans to get back on track may not be aggressive enough.

On a positive note, 3M's long-term track record suggests the market is probably overreacting to the headwinds the company has encountered. Since 2001, for example, the firm has executed 110,000 efficiency programs that resulted in $17 billion in total cost savings.

The company's CEO, who Wall Street appears to have lost confidence in, has been at 3M for over 30 years, spending most of his time as the chief operating officer overseeing the firm's efficiency programs.

While new CEO transitions can be a time of important changes for conglomerates like 3M, ultimately the company has faced many of them over the past 117 years, including Inge Thulin's (the previous CEO) transition period which also didn't start out smoothly.

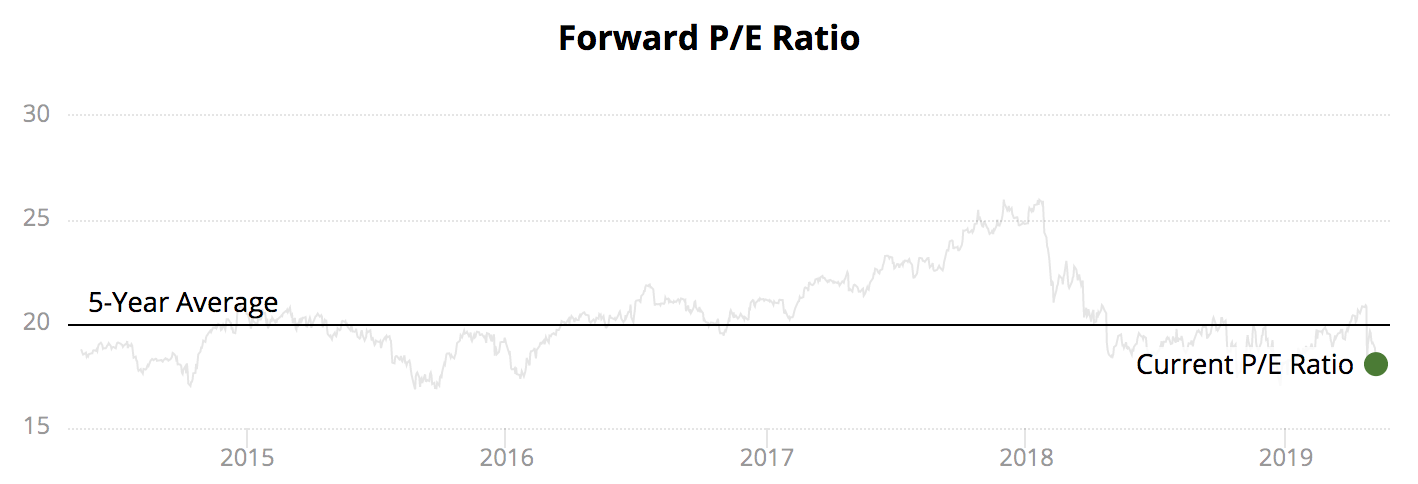

However, until investors are convinced that nothing is permanently broken with 3M's business, the stock could remain rangebound or even continue its decline. The company's shares have long fetched a premium valuation multiple, averaging a forward P/E ratio of 20 over the last five years.

Investors rewarded the company's relatively high margins, excellent free cash flow generation, stable operations, and numerous paths for profitable long-term growth thanks to the large and diverse markets 3M operates in.

While 3M's valuation multiple has contracted in recent weeks, shares continue trading hands at a forward P/E ratio of about 18, above the Industrials sector average of 16.2.

In other words, if investors continue to believe 3M's moat isn't what it used to be, and its earnings could be near a cyclical peak, then there could be some more downside as its multiple reverts to the sector average.

Source: Simply Safe Dividends

We have owned shares of 3M in our Top 20 Dividend Stocks portfolio since July 2015, when our initial purchase was made at $149.33 per share (MMM shares trade at about $176 today). Our position accounts for nearly 4% of our portfolio's total value.

Given the stock's current valuation, along with our rather full weight, I'm not inclined to do anything today. I view 3M's valuation as interesting, but not necessarily exciting yet.

In some ways a company like 3M is tricky to analyze because it does so much. The company markets over 60,000 products spanning numerous industries, and around 60% of its sales are made outside of America.

Taken from our thesis, you can see that 3M's business is incredibly expansive:

Industrial (35% of sales, 27% of income): tape, sealants, abrasives, ceramics, and adhesives for automotive, electronic, energy, food, and construction companies.

Healthcare (19% of sales, 25% of income): infection preventions supplies, drug delivery systems, food safety products, healthcare data systems, dental and orthotic products.

Safety & Graphics (17% of sales, 19% of income): personal protection and fall protection equipment, traffic safety products, commercial graphics equipment, commercial cleaning and safety products.

Electronics & Energy (15% of sales, 17% of income): insulation, splicing and interconnection devices, touch screens, renewable energy components, infrastructure protection equipment.

Consumer Products (14% of sales, 12% of income): post-it notes, tape, sponges, construction & home improvement products, indexing systems, and adhesives.

It's difficult to manage all of these product lines, and many of them are tied to the strength of the global economy. Market conditions are always changing, so management must invest in the right areas and know when to cut back.

3M, like most large industrials experience at some point, is going through another one of its periodic restructurings which are necessary to maximize its long-term performance over time.

In a worst-case scenario, 3M's sprawling empire may finally prove too difficult to manage effectively, and the firm could struggle to identify large enough profitable niches within its various businesses to drive the type of long-term growth management targets.

However, given the pervasiveness of many of the firm's products across so many different end markets, 3M's diversified business still seems likely to at least track global GDP growth over the long term and become a more valuable company.

But squeezing out 200 to 300 basis points of annual margin improvement like management hopes probably wouldn't be possible in such a scenario. As a result, mid-single-digit earnings and dividend growth would be more likely, below the firm's long-term 8% to 11% annual growth target.

Overall, 3M still looks like a business with strong staying power to me. The big question is how fast the company can continue growing. I like buying investments that are beaten down due to transitory factors outside of management's control (e.g. temporary softness in cyclical end markets), but 3M's lackluster performance in recent quarters is unusual.

Management deserves the benefit of the doubt, but investors will want to watch to make sure the company improves its results in the future. Should 3M's valuation multiple continue contracting as investors price the company as more of an "average" industrial going forward or fret about global growth, the stock would look more compelling.

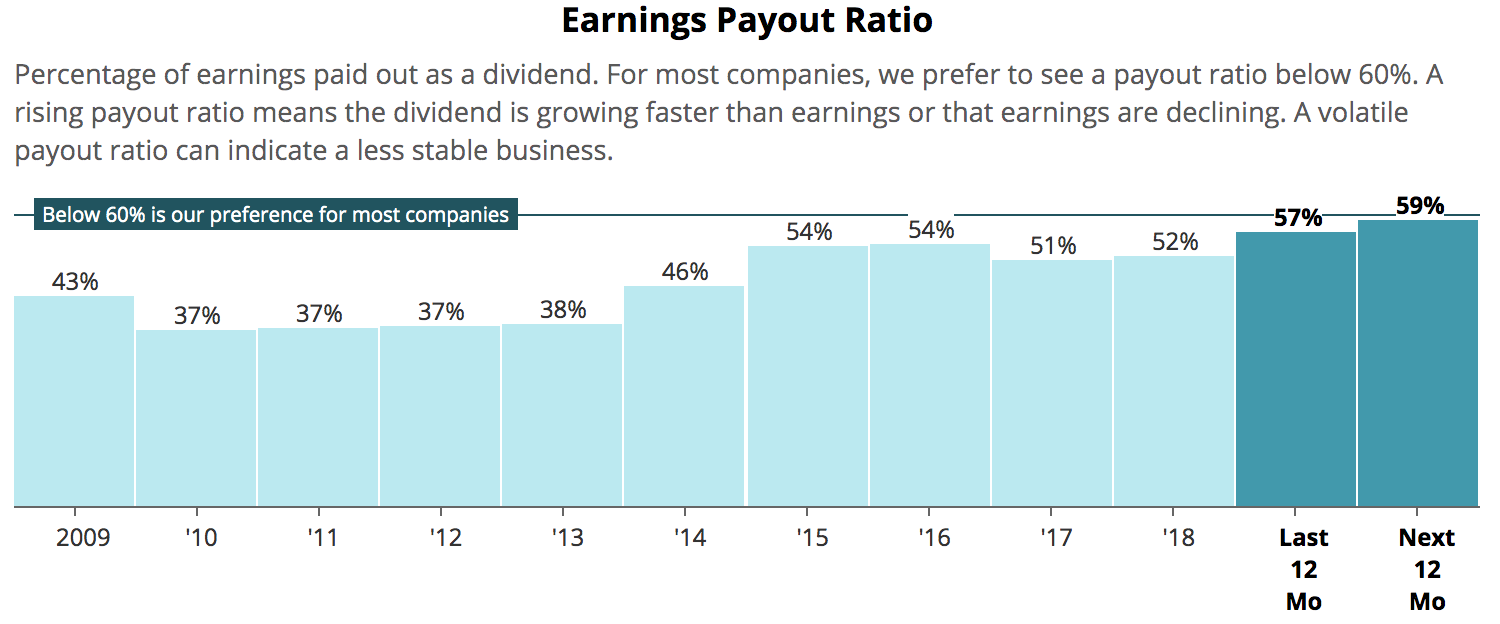

For now, I'm content to continue holding our shares and remain patient. Income investors should also note that 3M's pace of dividend growth could slow over the next year or two to a low single-digit pace as the firm deals with sluggish earnings growth, increased debt from the Acelity acquisition, and a relatively high payout ratio near 60%. This isn't something to worry about as long as management eventually gets the company back on track for stronger long-term growth.

Source: Simply Safe Dividends

Concluding Thoughts Many investors fear that no matter how impressive a company's past track record is, poor management can always run a great business into the ground.

General Electric used to be the most valuable company on the planet and a dividend aristocrat, for example. But poor leadership and destructive capital allocation decisions resulted in three dividend cuts over a decade and wiped out about 90% of GE's peak market cap.

While 3M's five straight quarterly misses and guidance cuts are troubling, it's far too early to declare 3M to be the next victim of its own success. 3M has paid uninterrupted dividends for over a century, raised its dividend for 61 straight years, and maintained an excellent balance sheet, through numerous restructurings and management changes.

CEO Michael Roman's tenure has thus far been disappointing over his first year on the job, but investors need to remember that former CEO Inge Thulin, who oversaw 3M's strong performance over the past decade, also struggled with weak early results that required a restructuring, which ultimately proved successful.

Mr. Roman's track record as COO during 3M's past successful efficiency programs is an indication that he's likely well versed in the competencies the firm needs to return to its historically strong growth rates, which management remains committed to delivering over the next five years.

While 3M will certainly have to execute on its turnaround plan, the company's 117-year track record of successfully adapting to shifting industry conditions and integrating various acquisitions provides some reassurance that this dividend king has what it takes to continue creating value for shareholders over the long term.

Patience will be required, though. Short-term dividend growth could remain slower than usual, and 3M's premium valuation could creep lower as the turnaround drags on or global growth slows. However, these issues don't look like reasons for long-term investors to sell. We will continue to stay the course and monitor management's progress in the quarters and years ahead.