Reviewing Blackstone's Corporate Conversion and Dividend Policy

Blackstone (BX) announced it will convert from a publicly traded partnership to a corporation on July 1, 2019. Investors cheered the move, sending shares of BX higher by 7.5%.

Let's review Blackstone's rationale for the change and what it could mean for income investors.

Blackstone's Corporate Conversion Blackstone decided to convert from a partnership to a corporation due to tax reform, which reduced the highest corporate tax rate from 35% to 21%. While Blackstone's tax bill will increase due to this change (partnerships pass on their income tax obligations to their owners, but corporations pay income tax), management believes that incremental cost will be more than offset by the benefits of a simpler structure.

As a publicly traded partnership, Blackstone issued a K-1 form each year and generated effectively connected income (ECI), unrelated business taxable income (UBTI), and nonresident state-sourced income. Due to these tax complications, Blackstone's stock was off-limits for many investors.

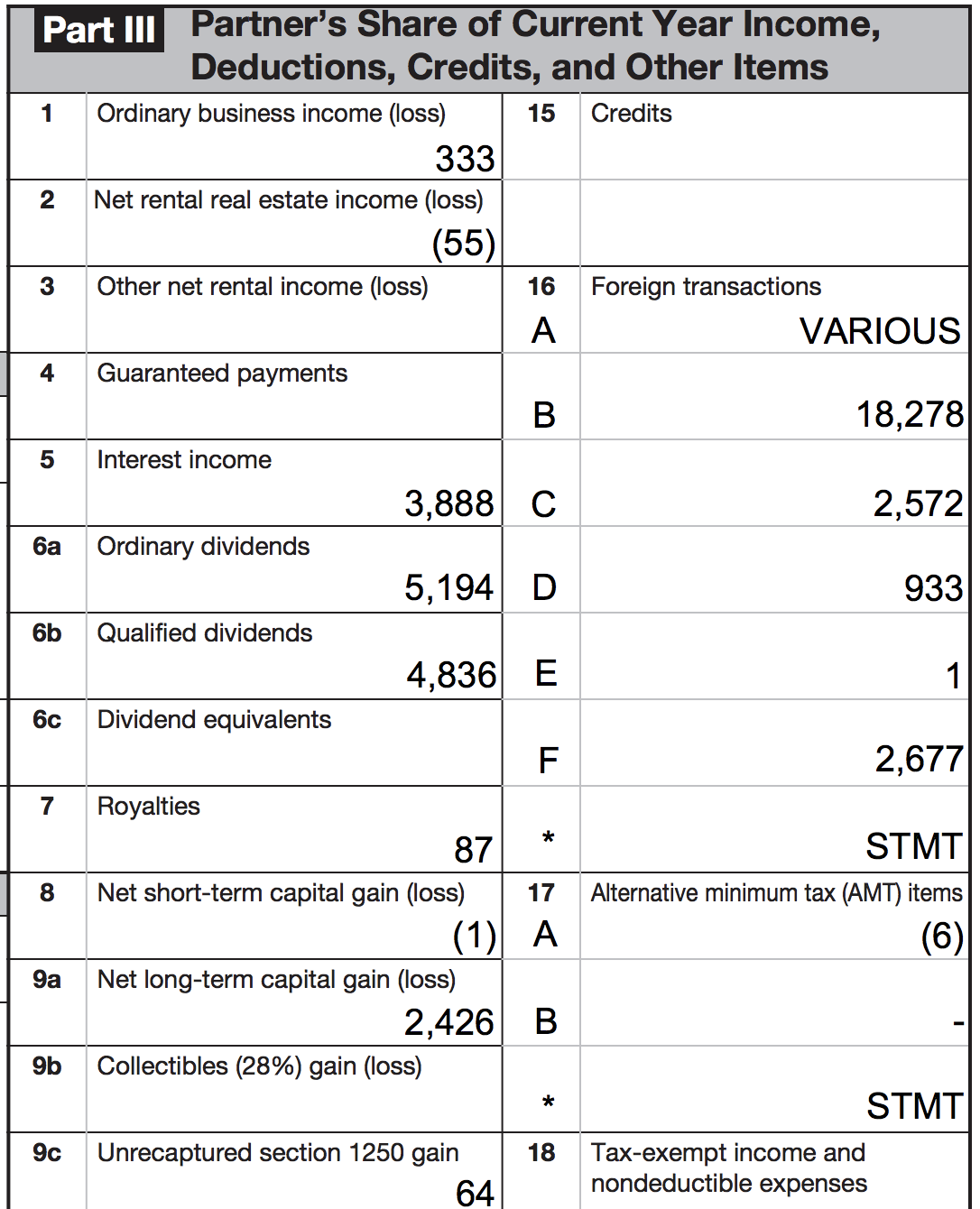

Here's a look at part of a sample K-1 from Blackstone for 2018:

Source: Blackstone

As a corporation, Blackstone will no longer issue a K-1 form, and shareholders will no longer pay taxes Blackstone's underlying income. Investors will instead receive form 1099-DIV, and all dividend payments will be qualified for U.S. tax purposes (taxed at the long-term capital gains rate). Blackstone will therefore become a suitable investment for retirement accounts, too.

While less tax complexity for shareholders is nice, the main reason why management is making this change is to try and increase Blackstone's investor base (and valuation multiple).

"We believe the decision to convert will make it significantly easier for both domestic and international investors to own our stock and should drive greater value for all of our shareholders over time."

– Blackstone CEO Stephen A. Schwarzman

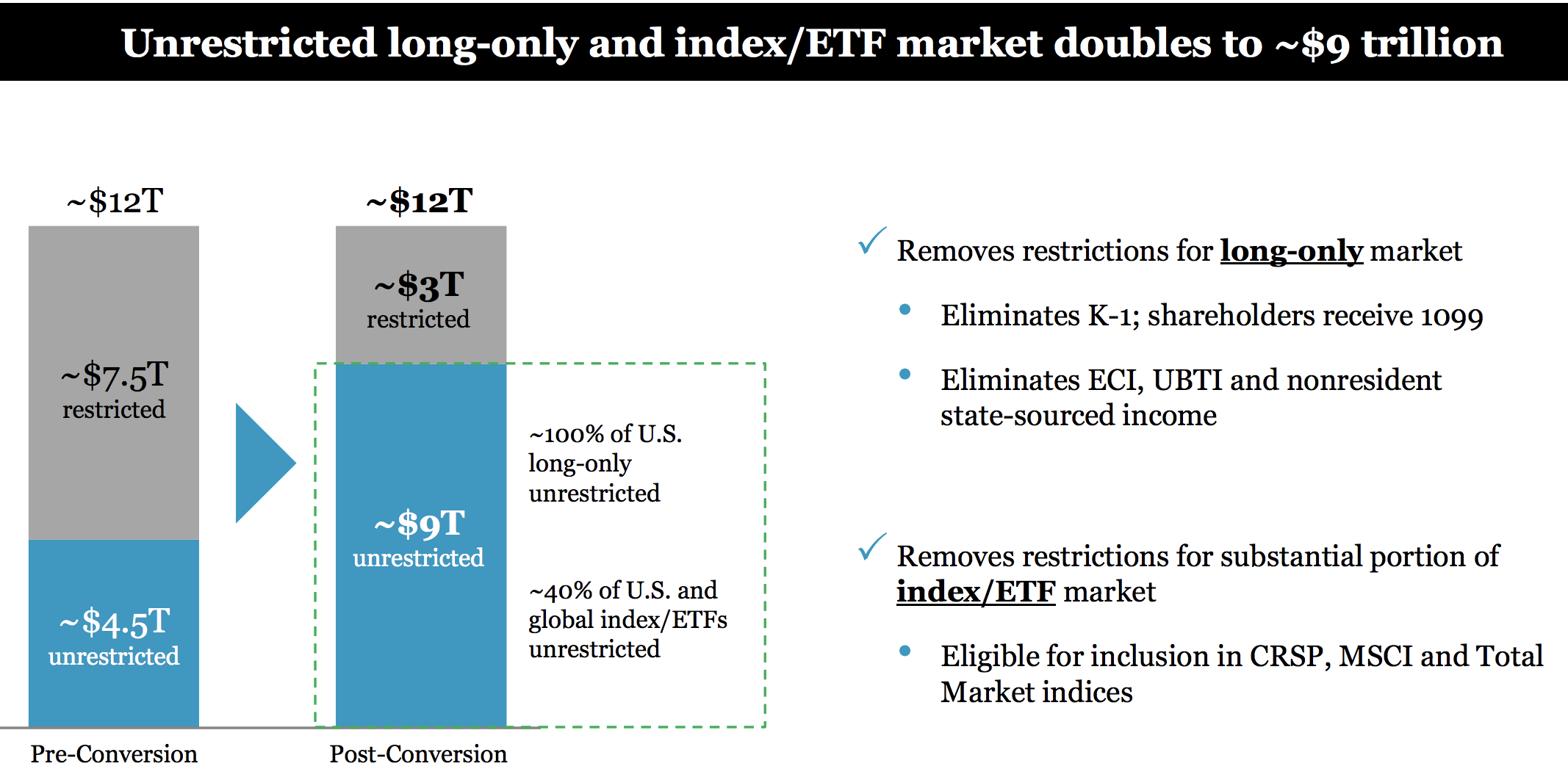

Over 60% of the U.S. long-only and index fund / ETF market is restricted from owning partnerships. Ditching the partnership structure puts Blackstone back in play for these funds, doubling the amount of unrestricted investor capital that could own a stake in the company.

Source: Blackstone Investor Presentation

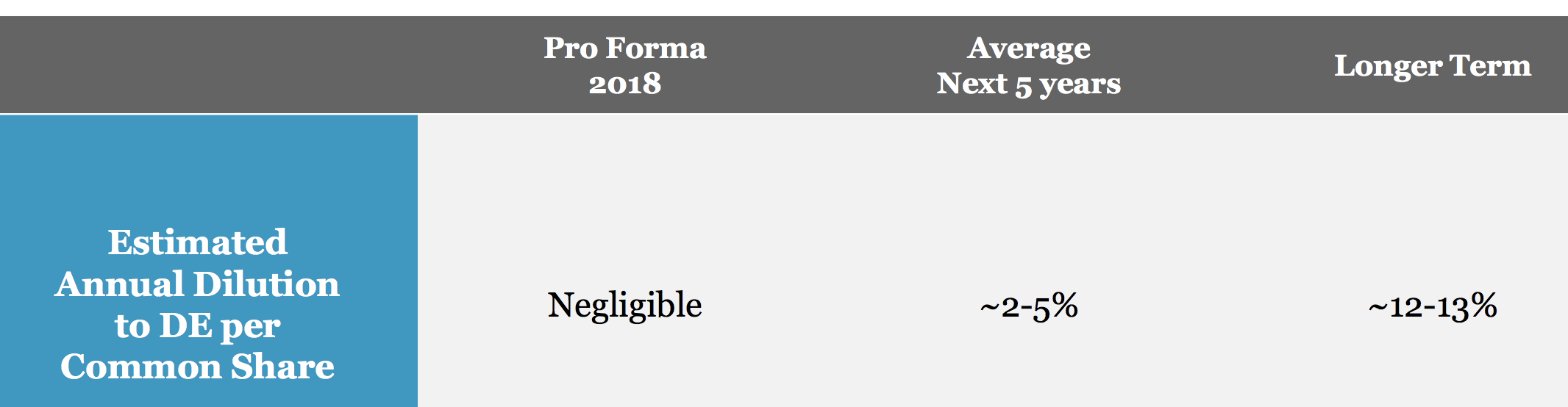

As previously mentioned, Blackstone's tax bill will increase from its corporate conversion, resulting in low- to mid-single digit EPS dilution annually over the next five years and double-digit annual EPS dilution in the long term. However, management believes the broader investor base Blackstone gains is worth the tradeoff.

Source: Blackstone Investor Presentation

What does this change mean for Blackstone's dividend?

The firm's historical intention was to distribute quarterly about 85% of Blackstone's distributable earnings, subject to adjustment by amounts determined by Blackstone's general partner.

The asset management industry is highly cyclical, since base management and performance fees are tied to assets under management, fickle capital gains, and investor sentiment. Blackstone's private equity business is also variable since the profits it can make often depend on the stock market's health (a key exit strategy is to take privately owned firms public, monetizing some of its ownership stake).

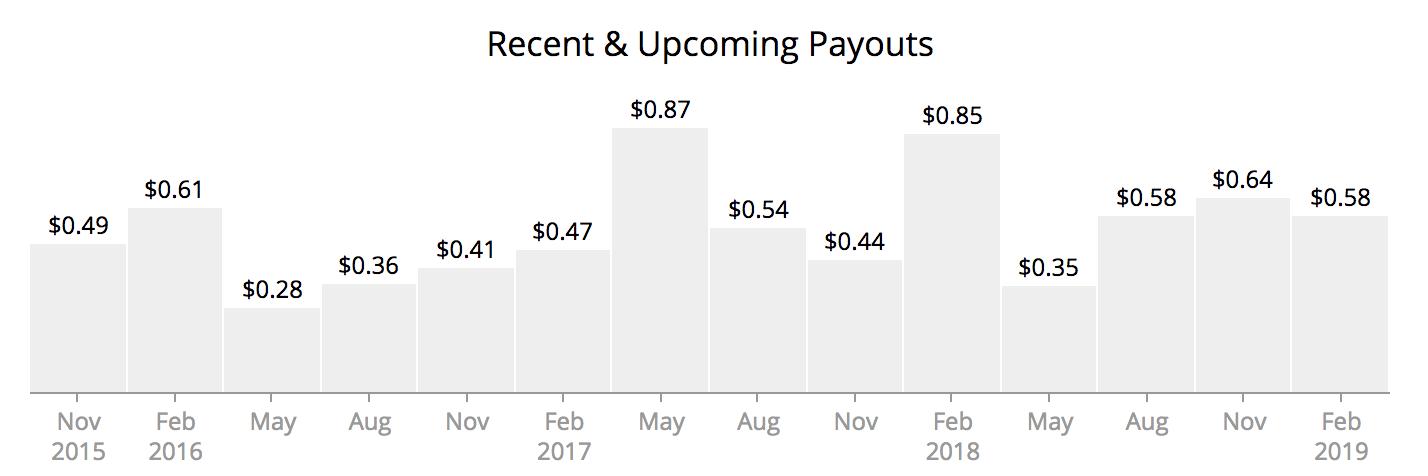

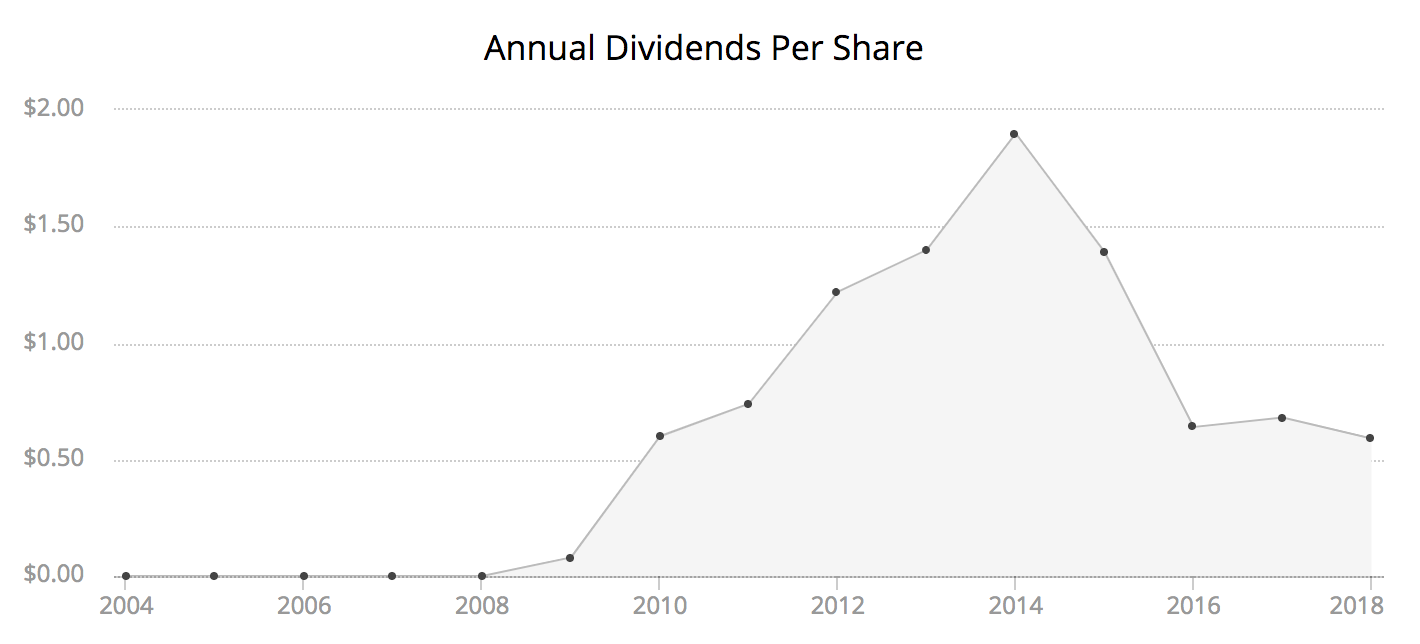

The end result is a volatile payout schedule, where any given quarterly distribution was rather unpredictable.

Blackstone Payment Schedule – Source: Simply Safe Dividends

As a corporation, especially one with a high target payout ratio of 85%, could Blackstone change its dividend policy?

Blackstone's dividend now faces double taxation (taxed at the corporate and individual levels), earnings are expected to be diluted over the next five years from corporate taxes, and the firm has growth ambitions to roughly double its assets under management to $1 trillion by 2026. At first glance, lowering the payout and perhaps moving from a variable to a fixed dividend could make sense.

In fact, Blackstone's peer KKR (KKR) did just that after converting from a partnership to a corporation in July 2018. The firm reduced its dividend by 26%, resulting in a more sustainable payout ratio near 30% and freeing up additional cash for share buybacks.

KKR had previously moved to a fixed dividend in 2015, after having paid variable dividends targeting 75% to 80% of its distributable earnings since going public in 2010. This change reduced KKR's annual dividend by approximately 66%.

KKR Dividend History – Source: Simply Safe Dividends

KKR's management said its fixed dividend was sized "to approximate our recurring quarterly cash flow, which means the quarterly distribution is not at all reliant on our ability to sell any investments over any 90-day period. And most importantly, we believe that this will allow us to retain capital, compound value on the balance sheet, buy back our stock, and increase our earnings power per share."

Basically, KKR believed its variable distribution was not going to ultimately get valued by the market, so that cash was better off being used for other purposes.

"Over time, we think that the market will value what we do with our balance sheet, including repurchasing our own units, more than the variable distributions we've been paying."

– KKR CEO Henry Kravis

Does Blackstone's current dividend policy maximize long-term value for shareholders? Or will the firm need to consider both reducing its payout and moving to a fixed dividend?

For now, management expects to maintain Blackstone's existing dividend policy, high payout ratio and all. Here's what the company's President and COO said:

"We don't have plans to change either our dividend policy or our zero dilution for purchase program at this point which together we think of made for a very shareholder friendly capital return policy.

As you know our business model is such that we can grow as we have had and will do at very high rates without essentially requiring much capital which is pretty extraordinary. And our capital return policy reflects and takes advantage of that to a great benefit for our shareholders.

So, as you note, obviously conversion enables a qualified dividend treatment that creates even more flexibility, but we’re going to maintain the approach."

– Blackstone President and COO Michael Chae

Blackstone CEO Stephen A. Schwarzman added:

"What we've seen from our investors is they like these healthy dividends and we think the market particularly in this more liquid form of C-Corp will react positively. Obviously over time if things are not positively received we can evaluate, but we really like this. We think shareholders like the idea that we’re big returners of capital, and we payout healthy dividends."

Basically, shareholders should expect Blackstone's variable dividend policy to remain intact for the time being. However, if the stock's valuation continues to sit below management's expectations following its corporate conversion, then a future change to the dividend is possible, likely intended to free up more capital for share buybacks.

The good news is that Blackstone's new corporate structure will result in lower personal taxes on dividends for shareholders, potentially softening the hit from any future dividend policy change. It's too soon to worry about such an event, but income-focused investors should monitor the situation going forward.

Blackstone, as the industry's dominant player, represents a potentially solid way for regular investors to gain exposure to investment types and asset classes that are normally out of their reach. These include: venture capital, private equity, hedge funds, and private real estate.

That being said, while Blackstone is among the best-run firms in its industry, the company's complex business model is still prone to wild swings in revenue and earnings. The end result is highly variable dividends that make Blackstone more suitable for risk tolerant investors who don't mind income fluctuations from one quarter to the next.

Finally, current Blackstone unitholders might wonder if there are tax consequences when the partnership converts to a corporation. Blackstone has not clarified this yet, but the conversion likely intends to be a tax-free deal.

Going back to KKR's corporate conversion in 2018, the firm structured its conversion to be a tax-free transaction. Based on tax law, Blackstone's conversion also appears likely to result in tax-free incorporation. However, unitholders should consult with their own tax advisor regarding the tax consequences from the conversion based on their individual circumstances.

"In connection with the Conversion, common and preferred partnership units were automatically converted into shares of Class A common stock and preferred stock, respectively. The Conversion generally was intended to be a tax-free transaction for U.S. federal and state income tax purposes, with unitholders generally taking a carryover tax basis in the shares of Class A common stock (or preferred stock) received in the Conversion." – KKR