VEREIT (VER) offers a high dividend yield near 6.5%, making the REIT potentially attractive for many income investors.

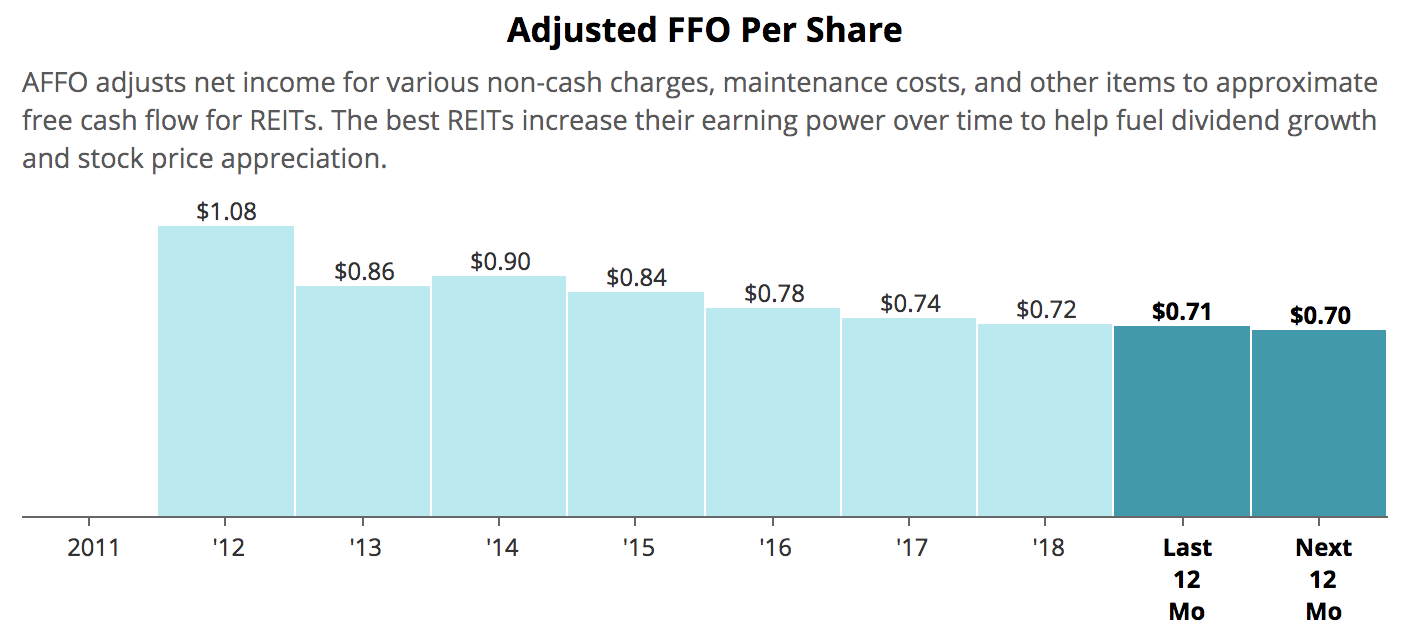

However, with VEREIT's dividend frozen since 2015 and its adjusted funds from operations (AFFO) per share expected to decline for a fifth straight year in 2019, how safe is VEREIT's dividend?

Let's take a closer look at the business and its long-term dividend safety profile.

Business Overview VEREIT incorporated in 2010 and owns a diversified portfolio of approximately 4,000 single-tenant commercial properties subject to long-term net leases. The REIT serves retail (42% of rent), restaurant (21%), office (19%), and industrial (18%) markets across America.

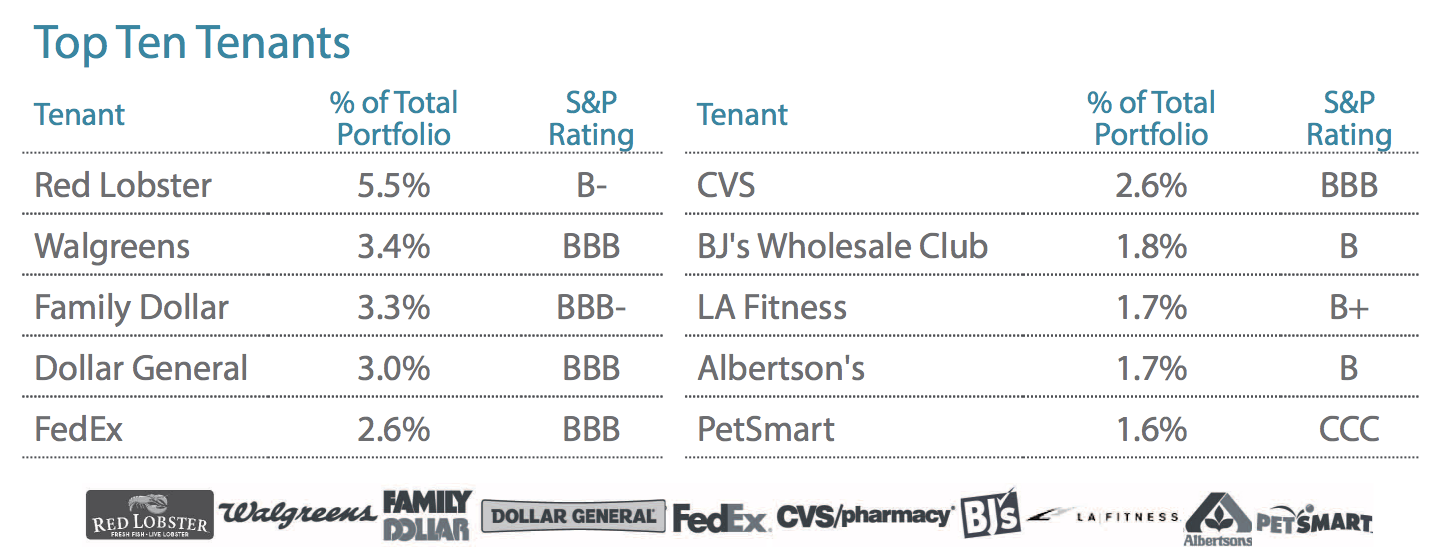

VEREIT does business with 661 tenants operating across 42 industries. Its top 10 tenants account for 27.2% of annual rent, and no single tenant exceeds 6% of rent. Approximately 42% of its tenants have investment grade credit ratings.

Source: VEREIT Fact Sheet

At first glance, VEREIT's business appears to have several favorable qualities, including nice tenant and industry diversification. However, the company has a checkered past it is still trying to overcome.

VEREIT's 2014 Accounting Scandal and Turnaround Plan In October 2014, VEREIT announced an accounting scandal in which its management team intentionally overstated the REIT's quarterly AFFO by 5% to 9% earlier that year. VEREIT's audit committee stated that the company's 2013 annual report and quarterly reports through the first half of 2014 should no longer be relied upon. The company's CFO was ultimately convicted of securities fraud.

In December 2014 the firm agreed to suspend its dividend until it delivered accurate financial statements and related compliance certificates. The new dividend was reinstated in mid-2015 at a rate "in line with its industry peers," resulting in a 45% cut compared to the firm's prior payout.

VEREIT's stock price lost nearly 40% from late October 2014 through December 2014 and remains about 30% below its pre-scandal price today, demonstrating the lack of confidence investors continue to have in the business.

The company responded by terminating executives believed to be responsible for the accounting fraud. A new CEO who specialized in turnarounds was brought in, several board members were replaced, and in July 2015 the company changed its name from American Realty Capital Properties to VEREIT in an effort to reset its image.

In August 2015 the new management team announced a business plan focused on asset divestitures and deleveraging. Since initiating the plan, VEREIT disposed of $3.7 billion of properties (over 15% of its real estate assets) and reduced its net debt to EBITDA leverage ratio from 7.5 to about 6.0 today. The company's credit rating was also upgraded back to investment grade.

With management executing on their turnaround plan and apparently reducing VEREIT's risk profile, let's take a closer look at the REIT's dividend.

VEREIT's Dividend Safety Profile Looking purely at financials, VEREIT's dividend safety appears reasonable for a REIT. The company's AFFO payout ratio sits just below 80%, which provides some cushion in the event that cash flow declines. Management's 2015 decision to cut the dividend nearly in half has made the current payout look more sustainable.

Source: Simply Safe Dividends

Leverage is another critical factor. Thanks to nearly $4 billion of asset disposals since 2015, VEREIT reduced its net debt from approximately $10 billion in 2014 to $6 billion today. As a result, the company's leverage ratio improved to a much more reasonable level, and VEREIT's credit rating was upgraded to investment grade in 2017.

For comparison, high-quality retail REITs Realty Income (O) and National Retail (O) have more conservative leverage ratios near 5.0 and 4.5, respectively. However, VEREIT's leverage is no longer alarmingly high.

Source: Simply Safe Dividends

So if VEREIT's payout ratio and leverage profile look reasonable, why doesn't the firm have a high Dividend Safety Score? Our scoring system takes a conservative, long-term approach to assessing dividend risk, and VEREIT's business still faces a few important uncertainties.

First, investors should note that the company faces future liabilities related to its accounting scandal. Specifically, VEREIT was hit with 14 lawsuits from individual groups of shareholders (known as opt out shareholders), as well as a class action suit.

The company has settled all but one of the opt out cases and still has to resolve the class action suit. Thus far VEREIT has paid $233.5 million to settle claims with shareholders owning 33.5% of the REIT's common stock.

It's hard to say what VEREIT's remaining legal liability could be. If a proportionate settlement is required for all remaining shareholders representing the other 66.5% of the company, the liability would top $400 million. The next trial is scheduled for September 9, 2019, so investors may have to grapple with this uncertainty for a number of months.

To understand the magnitude of this risk, consider that VEREIT's common dividend consumed $546 million of cash flow last year, compared to $711 million of adjusted funds from operations. In other words, about $165 million of cash flow is retained after paying dividends, an amount which could be much less than the legal settlement the company reaches to resolve the class action lawsuit.

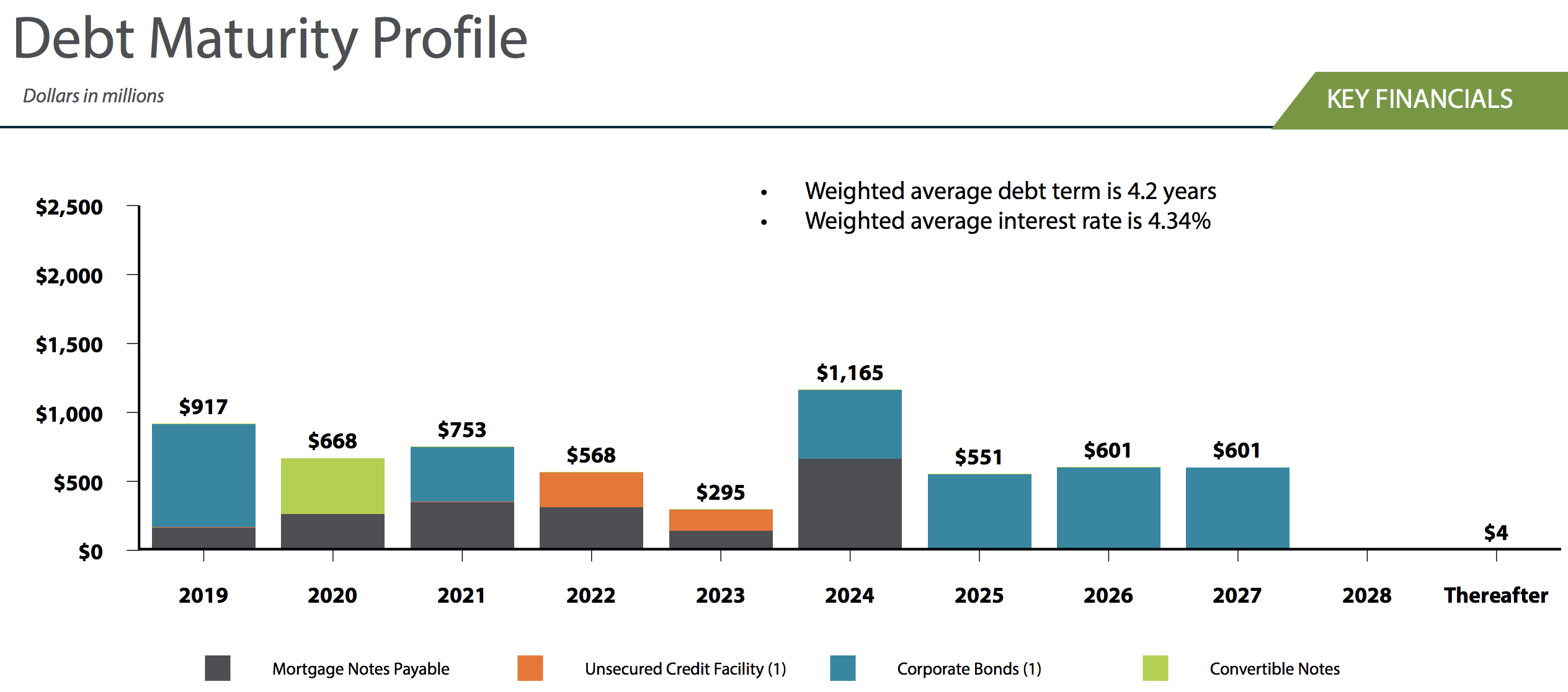

Further complicating the picture is VEREIT's debt maturity schedule. As seen below, the company has over $500 million of debt maturing each year from 2019 through 2022. The company does have access to a $2 billion credit revolver and could presumably dispose of more properties if needed, but VEREIT's dependence on favorable credit market conditions looks somewhat elevated compared to other REITs.

Source: VEREIT Investor Presentation

Another potential issue with VEREIT's dividend safety profile is the REIT's relatively young age. The company has only been in business for less than a decade, so we don't know how it would have performed during the last recession.

However, some the industries it depends on most for its cash flow are cyclical, including its three largest exposures:

Casual Dining Restaurants: 12.8% of annual rent

Manufacturing: 10.1%

Quick Service Restaurants: 8.7%

Meanwhile, approximately 58% of its tenants either have sub-investment grade credit ratings or are non-rated. While that's not necessarily a problem if management was selective and disciplined growing the REIT's portfolio, that may not be the case here.

Shortly after taking over as CEO after the accounting scandal broke, Glenn Rufrano remarked on an earnings call that VEREIT "was built through a rapid succession of large portfolio deals and company acquisitions." That's one of the reasons why he saw a need to sell off so many assets.

The former management team's poor ethics and apparent desire to grow at any cost, even by fudging the numbers, understandably causes some investors to question the underlying quality of VEREIT's real estate portfolio and tenant base.

Should a meaningful number of the company's tenants struggle or even go bankrupt during the next recession, VEREIT could have a difficult time maintaining its investment grade credit rating. That's especially true if the firm's remaining legal settlements end up being larger than expected.

Looking ahead, management expects AFFO per share to decline slightly in 2019 for the fifth straight year, driven again by asset sales. Same-store rental growth is expected to range from 0.3% to 1%. However, at the midpoint that expected pace of growth is only about half of larger REIT Realty Income's guidance for the same metric, perhaps raising some more questions about the quality of VEREIT's tenants.

Source: Simply Safe Dividends

Closing Thoughts on VEREIT Overall, VEREIT has several appealing qualities. The firm's cash flow is generated under long-term contracts with a weighted average remaining lease term of 8.9 years. Occupancy is expected to remain strong at 98% this year with same-store rent growing, albeit slightly. Over 40% of its rent is from investment-grade rated tenants. And a new management team is working hard to cull non-core assets, improve the firm's financial flexibility, and ultimately restore its image with investors.

However, despite an improved balance sheet and payout ratio compared to five years ago, VEREIT's investment case still has some hair which makes the stock appear to be a less appropriate choice for conservative investors.

Most notably is the REIT's disappointing history. Members of the original management team engaged in criminal activities, resulting in hundreds of millions of dollars of legal costs, a 45% dividend cut in 2015, a real estate portfolio of questionable quality, five consecutive years of falling AFFO per share, and the loss of investor confidence which has yet to be restored.

The current dividend, which has been frozen since 2015, looks sustainable at least over the short term, but that could change during a recession. After all, many of VEREIT's tenants appear sensitive to an economic downturn, and the company still faces a large legal settlement, likely later this year. Combined with VEREIT's higher leverage and shorter operating history compared to other blue-chip REITs, risk averse income investors may be better served looking at other dividend stocks.

VEREIT's Dividend Safety Score could improve once the firm settles its final lawsuits and returns to profitable growth, hopefully improving its balance sheet further. Until then, investors considering the stock should remain aware of these uncertainties and size their positions accordingly, if at all.