ONEOK: Uninterrupted Dividends Since 1989 and a High Yield

Founded in 1906, ONEOK (OKE) is a leading U.S. midstream service provider focused on natural gas liquids (NGL) such as butane, ethane, propane, and pentane. These liquids are generated when natural gas (methane) is produced.

NGLs are used as feedstocks for petrochemical plants (to produce plastics, rubber, etc.), burned for heating homes and cooking, and blended into vehicle fuel. Many NGLs are also exported to higher-cost markets in Europe, China, and India.

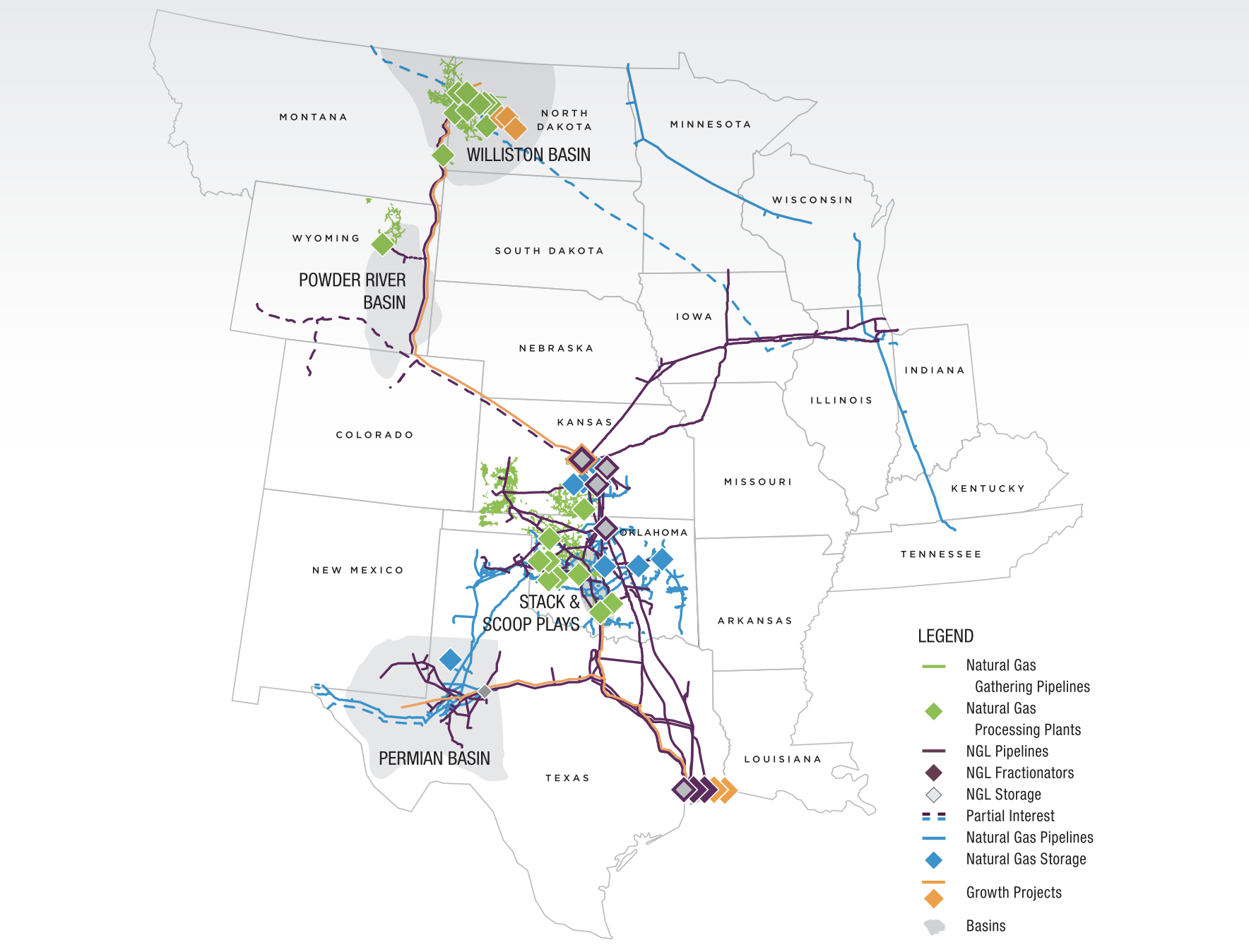

With a network of pipelines, processing plants, fractionators, and storage facilities, ONEOK connects growing NGL and natural gas supply with key market centers.

The firm's infrastructure connects to some of the nation's largest and fastest-growing shale formations, including the Permian basin in Texas and the Bakken formation in North Dakota.

Source: ONEOK Fact Sheet

ONEOK has three business segments:

Natural Gas Liquids (60% of EBITDA): ONEOK owns an integrated NGL pipeline system from North Dakota through the Mid-Continent to the Gulf Coast, linking key NGL market centers along the way. The firm provides fee-based services (gathering, fractionation, transportation, marketing, storage) to natural gas processors and customers.

Natural Gas Gathering & Processing (25% of EBITDA): provides gathering, compression, treating, and processing services to producers.

Natural Gas Pipelines (15% of EBITDA): provides natural gas transportation and storage services and direct connectivity to end-use markets (gas distribution companies, utilities, industrial firms, etc.).

Approximately 85% of ONEOK's earnings are fee-based and many of its customers and suppliers are subject to long-term contracts, reducing its sensitivity to volatile natural gas prices.

ONEOK has paid uninterrupted dividends since 1989 and increased its payout each year since 2003.

Business Analysis

The midstream industry has several attractive qualities. Pipelines are expensive and time-consuming to construct, with a single mile of new pipeline costing over $7 million per mile to build in recent years. This creates high barriers to entry, especially since various regulators usually have to sign off on new construction.

Simply put, few companies have the capital and industry connections (e.g. oil & gas producers, regulators) to build and operate integrated pipeline systems.

Only so many pipelines, fractionators, and storage facilities are needed within a particular geographic area as well, often resulting in a consolidated market. ONOEK's NGL network is particularly impressive as it connects to about 90% of pipeline-connected natural gas processing plants located in its core Mid-Continent region, providing customers with essential services and optionality.

Pipelines also have few viable substitutes given their safety and cost-efficiency compared to alternative modes of transportation such as rail and truck. Geographical constraints (many shale formations are in hard-to-access areas) often reinforce these advantages.

Furthermore, NGL and natural gas infrastructure enjoys relatively stable demand patterns since many of their end-use products are non-discretionary in nature. Homes need to be heated, vehicles need fuel, and petrochemicals are found in virtually every sector of the economy.

Importantly, most midstream service providers maintain tollbooth-like business models, which generate the bulk of their earnings from fee-based, long-term contracts. This minimizes their exposure to volatile commodity prices.

In a way, the midstream industry is similar to the utility sector in that it provides an essential service for energy firms, is capital intensive, and has solid earnings visibility, resulting in a stable cash flow stream that can support generous dividend payments.

ONEOK has taken a number of steps in recent years to reduce the risk profile of its business. For example, only about 15% of the company's cash flow is subject to commodity prices or volumes on its systems today, down from 34% in 2014.

The company's leverage ratio improved as well, falling from about 6x in 2014 to around 4.5x in 2019. Management expects leverage to drop to 4x by the end of 2020 with an aspirational goal of reaching 3.5x in the long term.

As a result, ONEOK earns a BBB investment-grade credit rating from Standard & Poor's, helping to ensure it maintains access to affordable debt financing for its future growth projects.

This deal doubled ONEOK's distributable cash flow and reduced its cost of funding by eliminating its incentive distribution rights.

Combined with improving coverage of the firm's dividend, a moderating growth-capital budget, and several key projects coming online, management expects ONEOK to have a self-funding business model going forward.

In other words, future growth projects can be funded using only the firm's retained cash flow after paying dividends and modest amounts of debt. With no equity issuances needed, ONEOK's expansion opportunities have no dependence on the firm's fickle stock price, reducing risk.

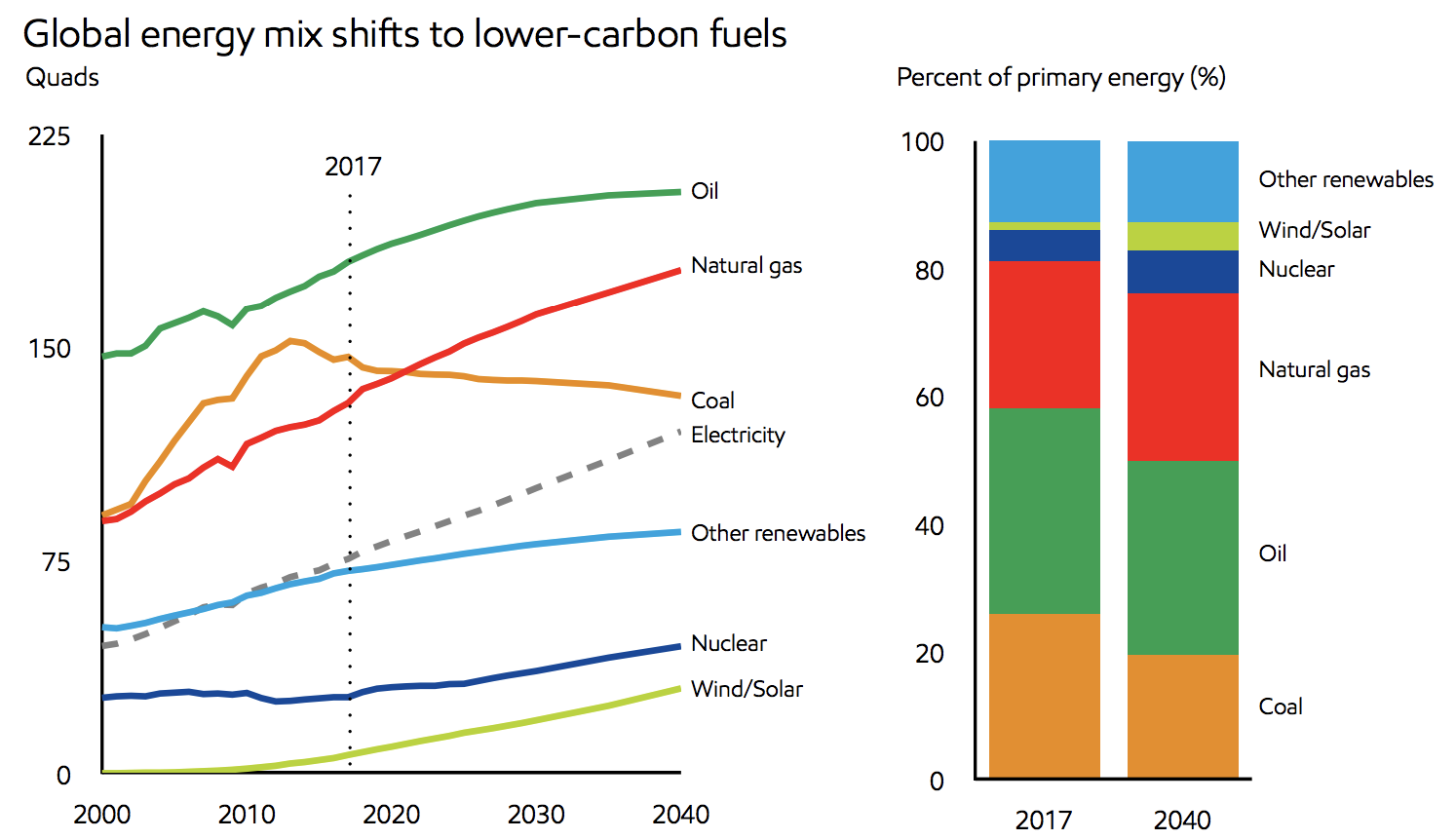

Looking ahead, ONEOK expects its integrated midstream infrastructure to continue benefiting from America's growing supply of NGLs and natural gas in the core shale basins it serves.

In the last decade, America has increased its natural gas production by more than 60%, according to the Wall Street Journal. The production boom in gas has resulted in strong output growth of NGLs, too.

Most industry outlooks, including Exxon Mobil's, expect the boom in natural gas to continue as lower-carbon fuels grow in demand. America's low-cost gas production compared to Europe and Asia is expected to continue fueling strong export demand for NGLs and liquefied natural gas as well.

Source: Exxon Mobil Energy Outlook

With domestic production investments expected to continue, exports rising, and more takeaway capacity needed in many of its service territories, ONEOK has focused the most of its growth spending on NGLs and gas gathering and processing projects.

However, the company faces several risks.

Key Risks

Like most other midstream companies, ONEOK faces risk from project cost overruns and delays. Fortunately, the firm has completed most of its key expansion projects and now appears to be focused on smaller, less costly, and less risky growth opportunities.

While this is a positive for the firm's risk profile and dividend coverage, a lack of major expansion projects also means that ONEOK's cash flow and dividend growth rate will slow in the future, likely to a low- to mid-single digit pace.

Management has so far met the firm's five-year guidance issued in 2017 calling for 9% to 11% annual dividend increases, but income investors should not extrapolate this type of payout growth beyond 2020.

Finally, it's worth repeating that approximately 15% of ONEOK's cash flow are not fee-based. A prolonged downturn in NGL and natural gas prices would hurt the firm's commodity revenue and while potentially reducing drilling activity and slowing production growth in the firm's key shale regions.

Low gas prices and weaker volumes could lead to excess capacity in some of ONEOK's markets and financially strain certain customers. Fortunately, the company's customers are primarily major oil & gas producers and leading petrochemical firms with healthy credit.

ONEOK's improved balance sheet, self-funding business model, reasonable payout ratio (management targets annual dividend coverage of at least 1.2x), and moderating growth spending help mitigate many of these concerns as well.

However, the evolution of energy markets (demand for fossil fuels, rise of renewables, etc.) should continue to be monitored given its potential to reduce the long-term need for new midstream infrastructure, which would weigh on the industry's growth outlook.

Closing Thoughts on ONEOK

ONEOK is one of the largest NGL-focused midstream companies in the country. Despite some earlier struggles with a relatively high mix of commodity-sensitive cash flow and elevated debt levels, management has managed an impressive turnaround, and all while maintaining a stable and rising dividend.

With its much stronger balance sheet, self-funding business model, and healthy long-term growth runway, ONEOK could be a decent choice for high-yield income growth investors who are comfortable with the industry's risk profile, and who want exposure to America's ongoing natural gas production boom.

.png)