Phillips 66 (PSX)

Phillips 66’s (PSX) roots go back all the way to 1875, though it only became a standalone public company when it was spun off from ConocoPhillips in 2012. The firm is the nation’s second largest independent refiner with 13 refineries in the U.S. and in Europe. However, Phillips 66 is also a highly diversified petrochemical company and operates through four interconnected business segments:

- Refining (38% of 2017 adjusted segment profit): refines crude oil into gasoline, diesel, and jet fuel via its global refineries which have a combined capacity of 2.1 million barrels per day of product.

- Marketing & Specialties (23% of 2017 adjusted segment profit): sells refined products (gasoline, diesel fuel, etc.) through its 7,550 Phillips 66, Conoco, and 76 branded gas stations in 48 U.S. states, and 1,324 JET and COOP stations in Europe.

- Chemicals (23% of 2017 adjusted segment profit): a 50% stake in Chevron Phillips Chemical Company LLC (CPChem), whose 30 global facilities and two R&D centers produce specialty petrochemicals that serve the solvents, catalysts, drilling chemicals, and mining chemicals industries.

- Midstream (15% of 2017 adjusted segment profit): gathers, processes, transports, and markets natural gas, and transports, fractionates and markets natural gas liquids in the U.S. This segment has a 50% stake in general partnership of DCP Midstream Partners (DCP), and a 55% stake in Phillips 66 Midstream Partners (PSXP), whose infrastructure services Phillips 66’s oil transportation and storage needs.

Business Analysis

The refining industry isn't one that's usually well suited to dividend growth stocks. After all it is:

- Highly capital intensive

- Demands substantial maintenance costs (over $1 billion annually on average)

- Very cyclical with profits tied to volatile commodity prices

However, some companies are better positioned to prosper in this complex, but economically critical, industry. That's why Warren Buffett, whose Berkshire Hathaway owned about 17% of the company's stock at the end of 2017, has said that "Phillips 66 is a great company with a diversified downstream portfolio and a strong management team."

Now it's true that Berkshire recently sold $3.3 billion of its stock in Phillips 66 back to the company in order to lower that position to just under 10%. However, as Buffett explained, this was to "eliminate the regulatory requirements that come with ownership levels above 10%. We remain one of Phillips 66's largest shareholders and plan to continue to hold the stock for the long term."

Why does Buffett like Phillips 66 so much to the point where it's his largest energy investment? The answer lies in the company's highly diversified business model, which helps to smooth out volatile cash flow and earnings from the refinery business.

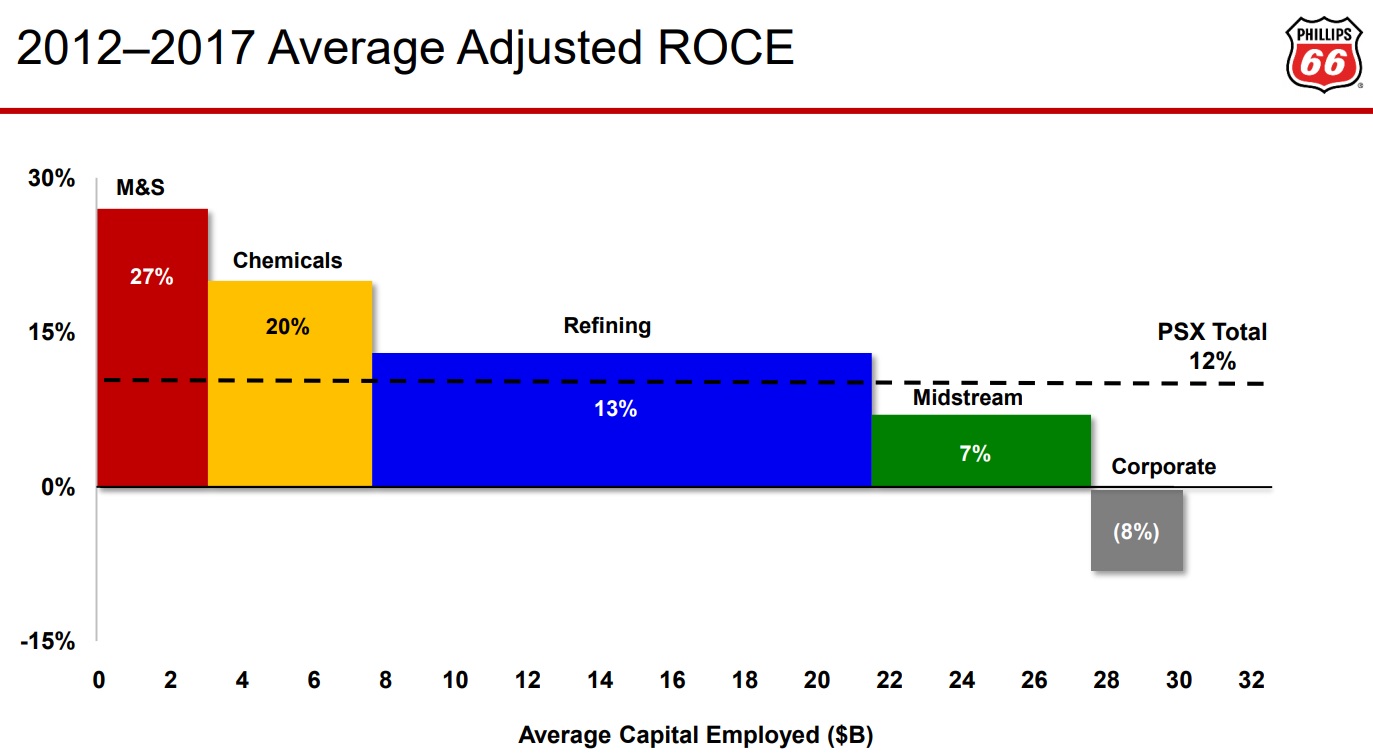

For example, over the past five years Phillips 66 has been able to achieve good returns on capital employed (ROCE) of 13% on its refining business. However, the company's ROCE on its chemicals and marketing businesses are far higher.

Meanwhile, while the midstream (energy storage, processing, and transportation), business is less profitable, it's also highly stable. That's because it's underpinned by long-term, fixed-fee contracts that are relatively insensitive to commodity prices.

These non-refining businesses provide much more predictable returns on capital and cash flow each year, providing the company with greater flexibility throughout the unpredictable refining cycles.

For example, over the past five years Phillips 66 has been able to achieve good returns on capital employed (ROCE) of 13% on its refining business. However, the company's ROCE on its chemicals and marketing businesses are far higher.

Meanwhile, while the midstream (energy storage, processing, and transportation), business is less profitable, it's also highly stable. That's because it's underpinned by long-term, fixed-fee contracts that are relatively insensitive to commodity prices.

These non-refining businesses provide much more predictable returns on capital and cash flow each year, providing the company with greater flexibility throughout the unpredictable refining cycles.

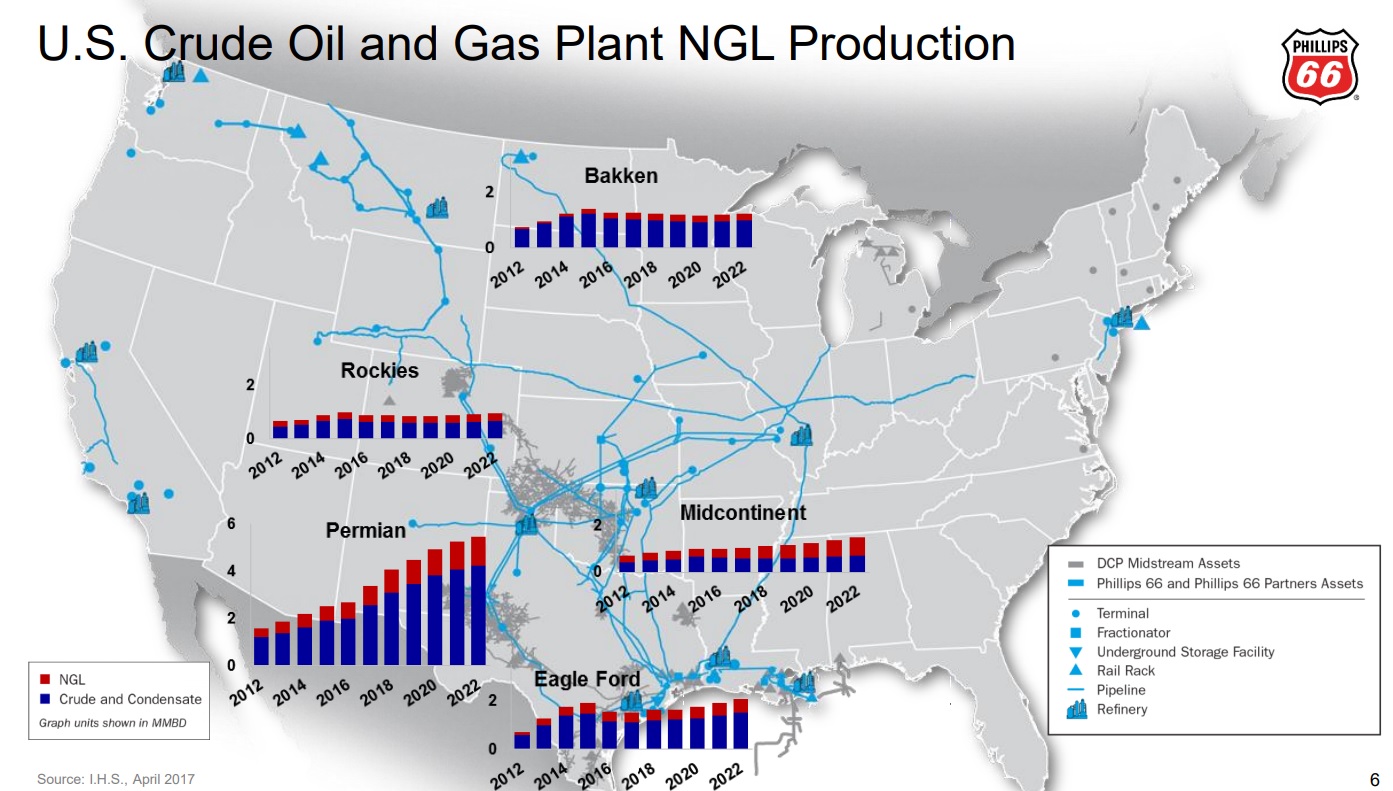

With that said, the refining business still generates the most profits of any segment Phillips 66 has. Fortunately, Phillips 66 enjoys some key advantages in this industry, including a very diversified network of refineries that can source low-cost oil from some of America's cheapest and fastest growing shale oil formations (and also Canada's booming oil production).

The company's Midwest refineries are well connected to strong shale regions in the Bakken, Rockies, and Midcontinent. Meanwhile, Phillips 66's Gulf Coast refineries are prone to benefit from strong production growth in Texas' Permian basin and Eagle Ford shale formations, while also providing the business with easy access to export markets.

In recent years, Phillips 66's refineries have used their geographical advantage to steadily increase their utilization rates, meaning running near capacity. In fact, in the third and fourth quarters of 2017, the company's refining utilization rates hit 98% and 100%, respectively.

Due to high fixed maintenance costs required in this industry, maintaining high utilization is a key way to boost profitability. As importantly, management, overseen by CEO Greg Garland (a 31-year industry veteran and former President of CPChem), has maintained a near-perfect safety record.

Due to high fixed maintenance costs required in this industry, maintaining high utilization is a key way to boost profitability. As importantly, management, overseen by CEO Greg Garland (a 31-year industry veteran and former President of CPChem), has maintained a near-perfect safety record.

Despite its strengths, Phillips 66 is well aware that the volatile nature of its refining business is still a liability, especially to its goal of raising its dividend every year in a sustainable fashion. Thus the company has a plan to greatly diversify its business towards faster growing and more stable cash flow sources.

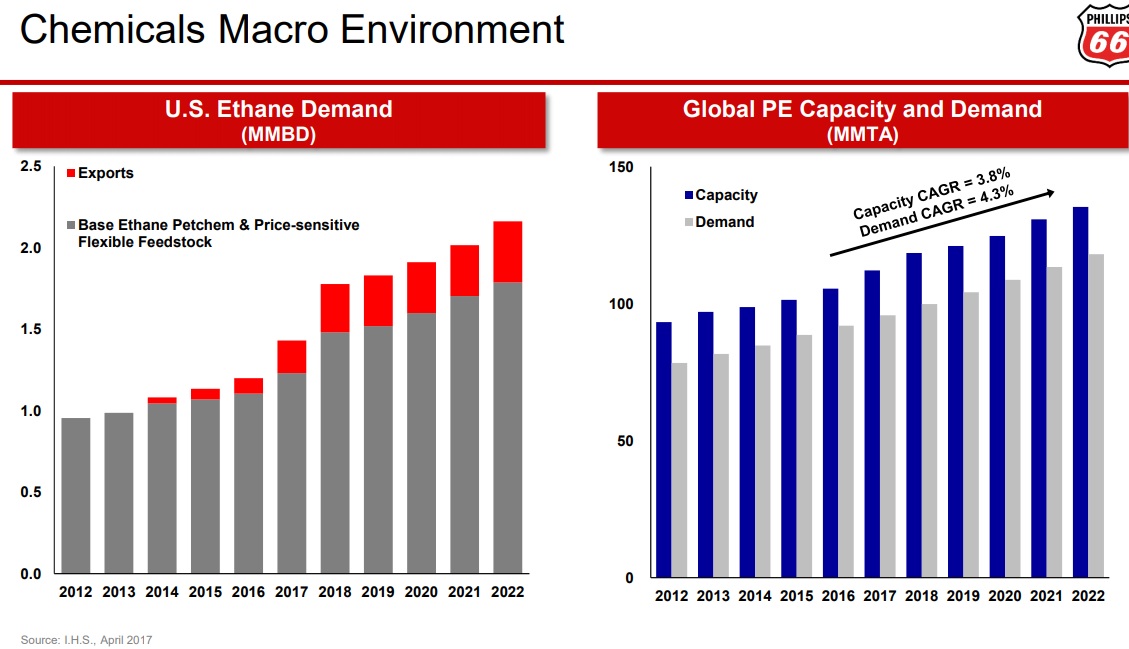

Specifically, management is most focused on growing the company's petrochemicals and midstream businesses. Phillips 66 has a 50/50 joint venture with Chevron (CVX) called CPchem. This business takes natural gas liquids (NGLs) and petroleum and turns them into highly sought after and profitable petrochemicals such as ethylene (used in plastics).

Thanks to the U.S. energy boom, especially growth in natural gas production, NGL production is soaring. In fact, it's expected to increase 51% by 2023. This has resulted in U.S. NGL prices being the second lowest in the world, behind only producers in the Middle East, where CPchem has 20% of its petrochemical capacity.

Thanks to the U.S. energy boom, especially growth in natural gas production, NGL production is soaring. In fact, it's expected to increase 51% by 2023. This has resulted in U.S. NGL prices being the second lowest in the world, behind only producers in the Middle East, where CPchem has 20% of its petrochemical capacity.

Thanks to lower input prices, the U.S. petrochemical industry is thriving, especially on the Gulf Coast where the industry is pouring over $85 billion into expanding capacity, including for exports. Fast-growing emerging markets such as China and India are causing demands for petrochemicals to soar, and the U.S. has a major cost advantage that Phillips 66 plans to take full advantage of.

And at the end of 2017, CPchem put two new chemical plants into operation in Texas, with a third facility going online in the first quarter of 2018. These three new plants will increase the company's petrochemical capacity by about 33% and should help drive strong profit growth in 2018 and 2019.

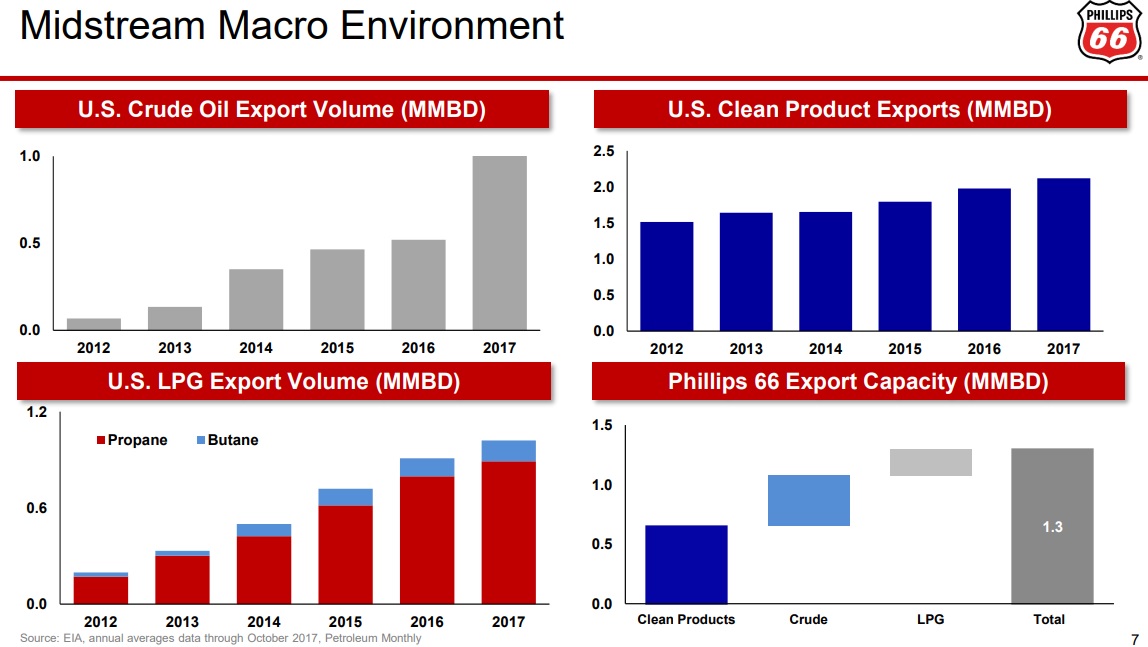

But it's not just refined petroleum and petrochemical products that the U.S. is exporting. American petroleum exports ( crude oil, ethanol, gasoline, petroleum coke, liquefied natural gas or LNG) more than doubled from 2011 to 2017 to reach 6.3 million barrels per day (bpd) and averaged 7.2 million bpd in the fourth quarter of 2017.

What's especially impressive is that in 2005 the U.S. was importing a total of 12.5 million bpd of oil and oil products, a figure that has dropped to 3.2 million bpd by 2017. In fact, in 2017 the U.S. exported an average of 1.1 million bpd of oil, and the International Energy Agency expects that figure to rise to 5 million bpd by 2023.

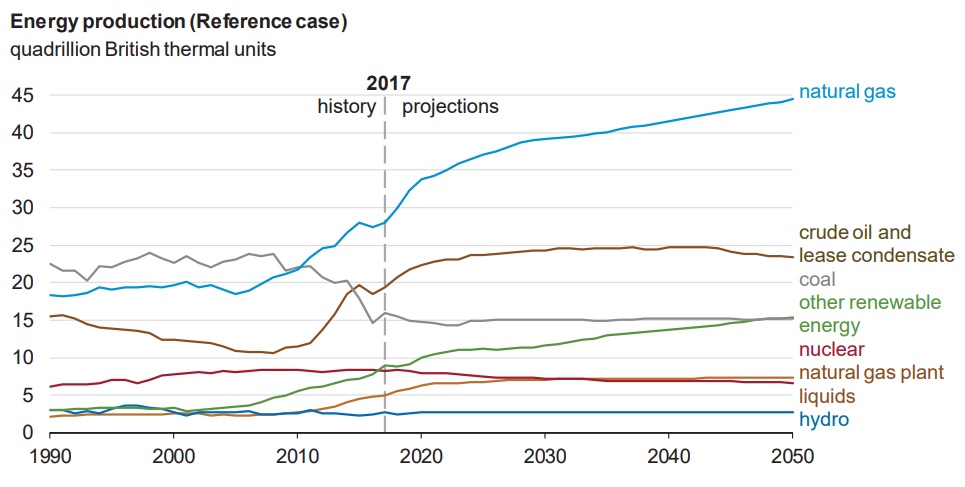

According to the U.S. Energy Information Administration or EIA, U.S. oil and oil condensate production is set to rise about 30% in the coming years and then remain stable at those levels through 2040. Meanwhile, U.S. gas and NGL production (input for petrochemicals) is set to boom through at least 2050.

The substantial production growth expected over the coming decades is needed to meet the enormous energy needs of emerging markets, especially Asia. That's where a growing population and even faster growing middle class is expected to create insatiable demand for oil, liquified natural gas, liquid petroleum gas, and petrochemicals. This secular trend has just started but already U.S. energy exports are rising fast.

Phillips 66 has been aggressively investing in its exported capacity, at all levels. That includes recently completing a 50% expansion of export capacity at its Beaumont Terminal in Texas. This increases its export capacity to 600,000 bpd, and the company plans to increase that a further 44% to 865,000 bpd. Meanwhile, an extra 3.5 million barrels of storage capacity are under construction at that facility to increase its capacity to 14.6 million barrels by the end of 2018.

To help provide the necessary infrastructure for all this energy production growth, which analyst firm IHS estimates will require up to $900 billion in additional midstream infrastructure by 2040, Phillips 66 has two master limited Partnerships, or MLPs.

These are DCP Midstream (DCM), which Phillips owns as a 50/50 joint venture with Enbridge (ENB), and Phillips 66 Partners (PSXP). DCP Midstream is specialized for NGL processing, storage, and transportation, while Phillips 66 Partners is designed to fund the company's aggressive midstream expansion plans.

These are DCP Midstream (DCM), which Phillips owns as a 50/50 joint venture with Enbridge (ENB), and Phillips 66 Partners (PSXP). DCP Midstream is specialized for NGL processing, storage, and transportation, while Phillips 66 Partners is designed to fund the company's aggressive midstream expansion plans.

Here's how it works. Phillips 66 Partners raises external capital from investors, (debt and equity) and then buys Phillip's midstream infrastructure, including $2.4 billion worth in 2017. Phillips 66 owns 55% of its MLP's limited units, plus its lucrative incentive distribution rights, or IDRs.

The assets it sells to the MLP have long-term fixed-fee contracts in place, which generate stable distributable cash flow (a rough equivalent of free cash flow for MLPs) and allow the MLP to raise its payout quickly (31% annually since its IPO). Phillips 66, thanks to its 55% stake in the MLP and its IDRs, ends up obtaining nearly 75% of the Phillip 66 Partners' total cash flow. All while recouping the construction costs of the midstream assets in a tax-efficient manner.

DCP Midstream has the same business model, acting as an external growth capital fundraiser to help drive the company's expansion in petrochemical exports via its midstream NGL business.

Of course, a strong long-term growth runway is useless to income investors if a company isn't both shareholder friendly and has access to enough low-cost capital to actually execute on its growth projects. Fortunately, that's not the case with Phillips 66.

The company currently has nearly $8 billion in liquidity (cash plus remaining borrowing power on revolving credit facilities). In addition, its MLPs have about $1.1 billion in liquidity, meaning that Phillips 66's total access to low-cost growth capital stands at approximately $9 billion. For context, across its entire family of MLPs and subsidiaries, the company expects to invest $3.2 billion in total capex in 2018.

As importantly for dividend investors, Phillips 66 has been very generous when it comes to sharing profits and cash flow.

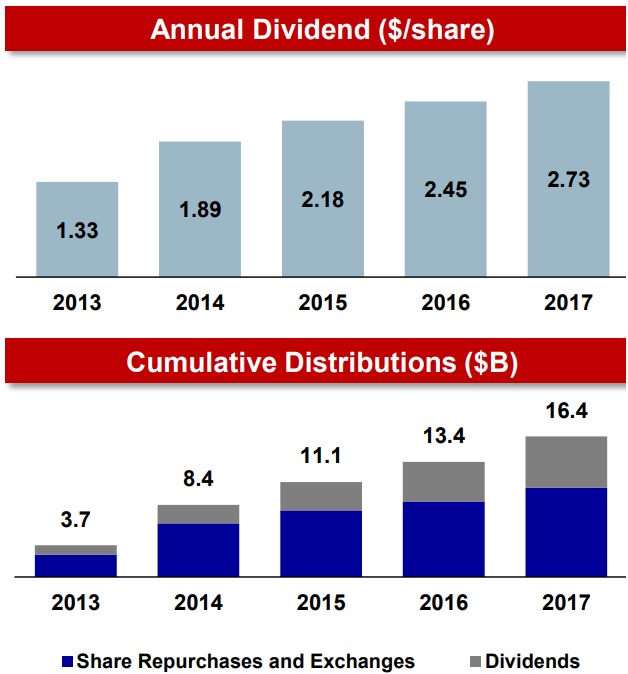

Since its IPO, Phillips 66 has been very generous with returning cash to shareholders in the form of buybacks and dividends. In fact, over the past five years, about 40% of profits have been returned in these two forms, with 60% of profits being used to fund future growth. For 2018 and 2019, management expects the total payout ratio (buybacks + dividends) to be about 50% of earnings.

In late 2017, the company authorized an additional $3 billion in share buybacks, bringing the total authorization since its IPO to $12 billion. Management expects to repurchase about $2 billion of shares in 2018. The firm's large amount of buybacks has helped Phillips 66 reduce its share count by 20% since its IPO, which has helped fuel 29% annualized dividend growth since 2012.

The combination of Phillips 66's excellent capital allocation skills and strong liquidity, combined with America's ongoing energy boom, seems likely to drive at least mid-single-digit annual earnings growth over the years ahead, although the path almost certainly won't be linear.

Key Risks

While Phillips 66 is one of America's top refining companies, that doesn't mean that its business model will allow for impressive dividend growth rates over time.

That's largely because refining is a highly cyclical business driven by what's called "the crack spread." The crack spread is the difference between what a refiner pays for oil (its primary input cost) and the selling price of refined products, which is usually indexed off Brent crude prices (the world oil standard).

There are actually several crack spreads, because refiners like Phillips source their oil (including different grades) from various regions. For most of 2017, the average crack spread the company enjoyed was a healthy $12 to $18 per barrel. However, then Hurricane Harvey hit the U.S. Gulf Coast where most of U.S. refining and export capacity is located.

This caused the average U.S. refining crack spread to jump to $35 per barrel for a brief time, helping to boost the refiner's profitability immensely. However, as that hurricane damage gets repaired, the crack spread is steadily falling and won't provide a source of windfall profits going forward. In fact, by the end of the year the crack spread was down to $14 per barrel, about average for the majority of the year.

To give you a sense of how volatile refining profits can be, take a look at the last three years of adjusted profits from this segment:

- 2015: $2.5 billion

- 2016: $277 million

- 2017: $1.1 billion

Phillips 66 also got lucky that most of its capacity was unaffected by the storm. All energy companies can occasionally experience industrial accidents, or weather-related events that can knock out capacity and lower cash flow temporarily.

The refining crack spread is hardly the only way that Phillips 66's cash flow is sensitive to commodity prices. At the end of the day, practically every aspect of the company's business involves selling commodity products, which means that its earnings can swing wildly based on numerous important energy prices including: petrochemical prices, natural gas prices, NGL prices, and of course the various forms of crack spreads it deals with.

It's also worth mentioning that much of the company's future growth is dependent on strong growth in U.S. energy exports, which themselves face several risks. In the short term, a potential trade war with China might lower demand for exports of oil and petrochemicals.

In fact, CNBC has reported that 40% of the 106 goods China is threatening with 25% retaliatory tariffs are plastics, petrochemicals, petroleum products, and specialty chemicals.

According to Alex Lidback, VP for chemicals at Wood Mackenzie, "It's a concern without a doubt because the U.S. has a good cost position, they're adding capacity and the Chinese market is very short of polyethylene as a whole, so they need the imports to meet their demand growth."

Now a trade war may or may not happen (and seems unlikely to affect Phillips 66's long-term earnings power), but the point is that unexpected geopolitical events can periodically invert an investment thesis.

Now a trade war may or may not happen (and seems unlikely to affect Phillips 66's long-term earnings power), but the point is that unexpected geopolitical events can periodically invert an investment thesis.

Another potential risk is that global energy demand falls short of the rosy projections of various analysts, including the EIA. For example, analyst firm McKinsey has done an extensive report on the future of the global energy industry out to 2050.

While they are highly bullish overall (they forecast that 74% of global energy will still come from fossil fuels by 2050 compared to 82% today), even they say that global oil demand might peak as early as 2030.

Even if nothing happens to overturn the strong growth prospects of the U.S. energy industry, Phillips 66 still faces high execution risk on its growth projects, especially the midstream business.

For example, Phillips 66 Partners owns 40% of the Bayou Bridge pipeline project which was scheduled to begin construction in the first half of 2018. The permits were all obtained, but in February 2018 a Louisiana Judge revoked the permit over worries over environmental damage.

That ruling was overturned by the Fifth Circuit Appeals Court, but the point is that midstream projects often face numerous legal challenges. Some of these can drag on for years, resulting in large cost overruns and cash flow targets falling short of management projections.

Finally, Phillips 66 is counting on its MLP, Phillips 66 Partners, to be the major funding vehicle for its midstream ambitions. However, whether or not the MLP can actually obtain enough growth capital to buy all of its sponsor's assets is largely dependent on fickle equity markets.

That's because Phillips 66 Partners has chosen to grow its distribution at a very fast rate, expecting this to result in a strong unit price and thus create low costs of equity. As a result, the MLP is only retaining about 10% of its cash flow to fund growth. The rest of the growth capex funding is coming from debt and equity issuances.

Such a business model can be challenged if the MLP's unit price were to fall low enough for long enough, making it impractical to issue new units. The MLP industry has been hammered in recent years by a perfect storm of negative factors including:

- The worst oil crash in over 50 years

- Interest rates rising off their lowest levels in history (making high-yield stocks less attractive)

- The broader market correction

- An unfavorable regulatory change by the Federal Energy Regulatory Commission

Phillips 66 has yet to announce to what extent this regulatory rule change will affect its MLP. Even if there is no material impact (as is the case with most MLPs), the point is that Phillips 66 Partners' growth potential, and by extension part of Phillips 66's, is somewhat at the mercy of equity markets, which could hurt the company's ability to live up to its full growth potential.

Closing Thoughts on Phillips 66

Phillips 66 is undoubtedly one of the best run and highest-quality petrochemical companies in America, if not the world. The firm's segment diversification, efficient operations, essential energy products, and exposure to numerous long-term growth catalysts make it an interesting choice for anyone looking for a good income growth stock in this space.

That being said, investors looking at Phillips 66 need to realize the complex and cyclical nature of its business model. The company is very capital intensive, highly sensitive to commodity prices, and somewhat exposed to fluctuations in equity markets, making it at least a medium risk stock. As a result, its payout growth may prove to be far slower and more volatile than in the recent past.

In other words, Phillips 66 isn't necessarily a good fit for very conservative income investors. The stock should probably only be owned by investors who are comfortable with the volatile nature of the firm's cash flow and earnings, and even then only as part of a well-diversified portfolio.