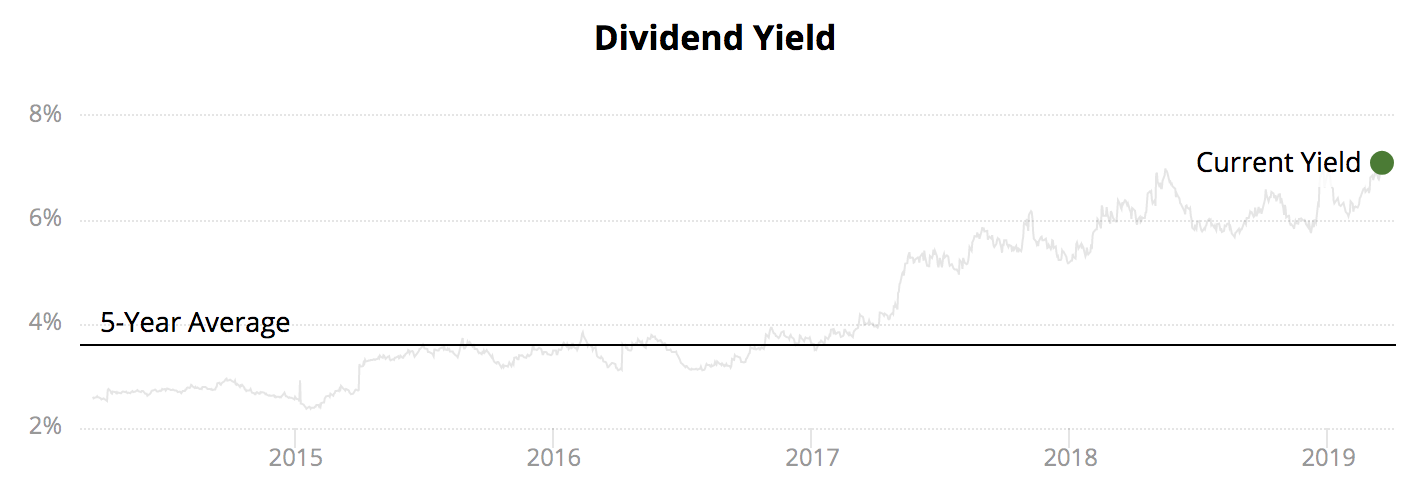

Tanger Factory Outlet Centers' (SKT) dividend yield has soared from 4% in early 2017 to 7% today. Despite the REIT's track record of increasing its dividend each year since becoming a public company in May 1993, some income investors are worried about the payout's safety.

Source: Simply Safe Dividends

Let's take a closer look at Tanger's recent struggles and assess how safe the retail REIT's dividend appears to be going forward.

Tanger's Growth Struggles In business for nearly 40 years, Tanger owns a portfolio of 44 outlet shopping centers located across 22 states. Its properties have over 3,100 stores which are leased to more than 530 different companies. Most of its tenants are higher-end apparel retailers which offer discounted clearance items at Tanger's locations.

Apparel retail is a notoriously challenging industry. Companies must invest heavily in inventory, labor, rent, and advertising, while consumers often have fickle tastes, chasing the latest deal or fashion trend.

The rise of e-commerce and its impact on consumer shopping preferences continues sending ripples through the industry as well. The ability of mall-focused REITs to grow in such an environment has come into question, and Tanger is no exception.

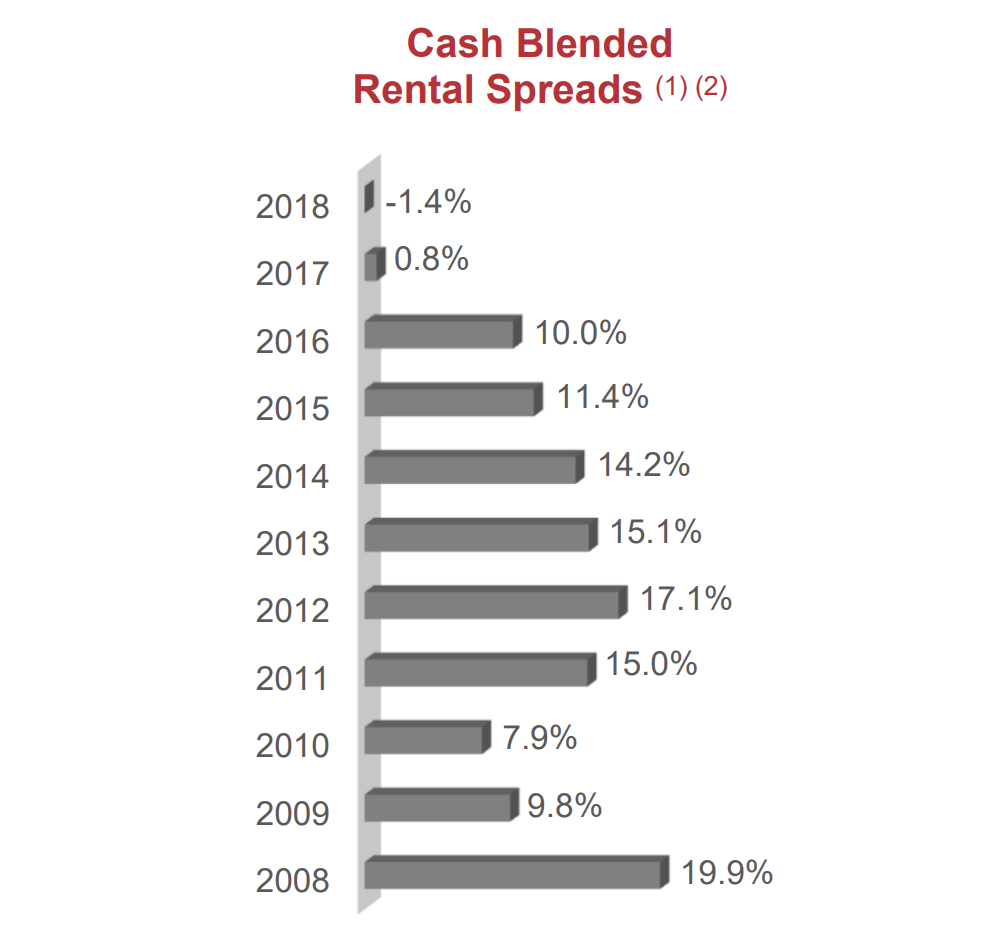

For many years, Tanger enjoyed double-digit growth in rental spreads, which measure the difference between rent per square foot on a new lease compared to the rent that was previously paid for the same space. However, Tanger's rental spread slowed to 0.8% in 2017 and actually turned negative in 2018, indicating its properties were now struggling to exert pricing power.

Source: Tanger Investor Presentation

Similarly, Tanger's occupancy rate had never dipped below 95%, even during the financial crisis. While portfolio occupancy stood at 96.8% at the end of 2018, management expects average occupancy in 2019 to dip as low as 94% for the first time in Tanger's history.

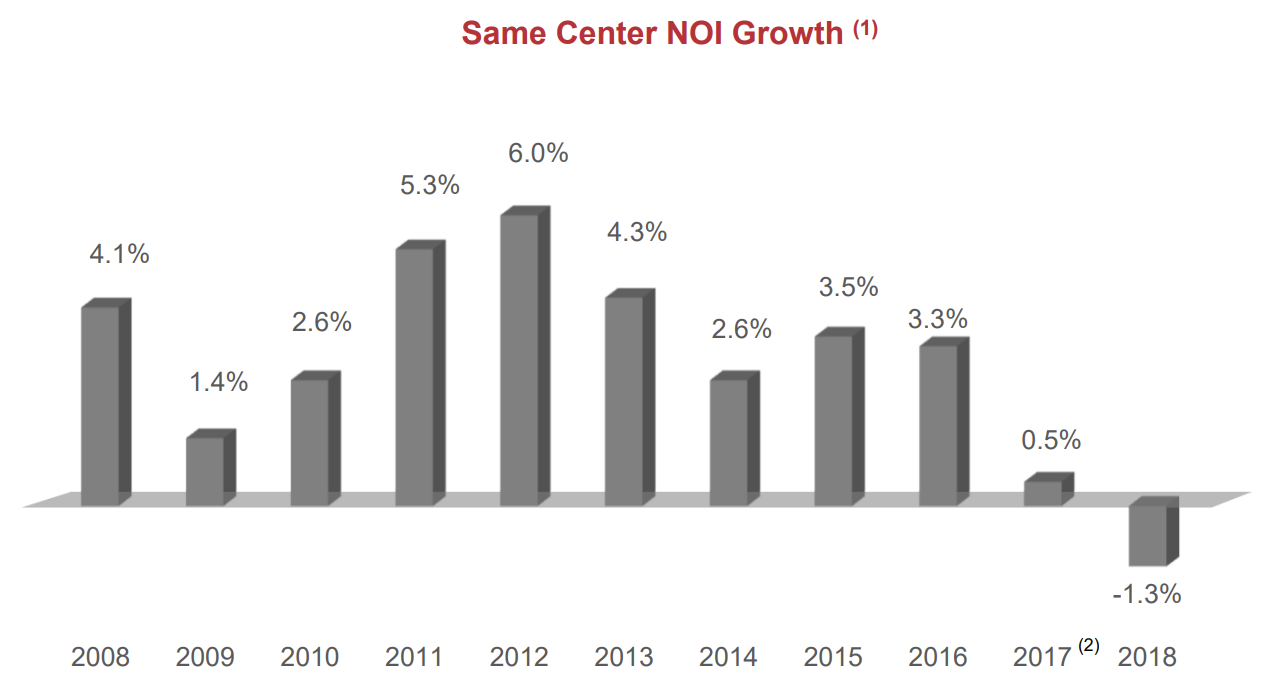

This combination of falling occupancy and weak rental spreads resulted in a 1.3% decline in same-center net operating income (NOI) growth in 2018.

Source: Tanger Investor Presentation

Investors were not expecting this deceleration, which helps explain Tanger's poor stock performance since early 2017. Unfortunately, management doesn't expect improvement anytime soon. Tanger's 2019 guidance calls for same-center NOI to decline between 2% and 2.75%.

Interestingly, Simon Property Group (SPG), another mall REIT, achieved 2.3% NOI growth in 2018. Approximately 79% of its NOI is from U.S. malls and premium outlets (42% of NOI is from its value platform, which primarily consists of Simon's premium outlets). Simon expects these businesses to record 2% same-center NOI growth this year, which isn't very fast but it's significantly better than Tanger's guidance calling for a low single-digit decline.

In 2018 Simon's malls and premium outlets also recorded a 14.3% increase in leasing spreads and 5.3% growth in retail sales per square foot, once again topping Tanger's results by a wide margin.

What explains this variance? Your guess is as good as mine regarding the future of outlet malls. However, given Simon's continued low single-digit NOI growth across its portfolio, this type of bargain shopping seems to remain valued enough by consumers to keep the REIT's profits from quickly eroded.

Instead, Tanger's divergence from Simon appears to be driven by its weaker mix of tenants. Jim Williams, Tanger's CFO, explained on the firm's February 2019 earnings call that over half of the firm's expected NOI decline this year is due to additional retailer bankruptcies, with much of the remainder due to store closures Tanger experienced in 2018 from meaningful tenants such as Toys 'R' Us and Nine West.

"If you look at the midpoint, the decline in NOI is 240 basis points, about 140 basis points of that is from the expectation of the further bankruptcies, potential rent adjustments from 2019 activity. Add to that same-store NOI would be down on about 100 basis points, which factors in all these other things you mentioned, the drag from the 2018 closures and so forth."

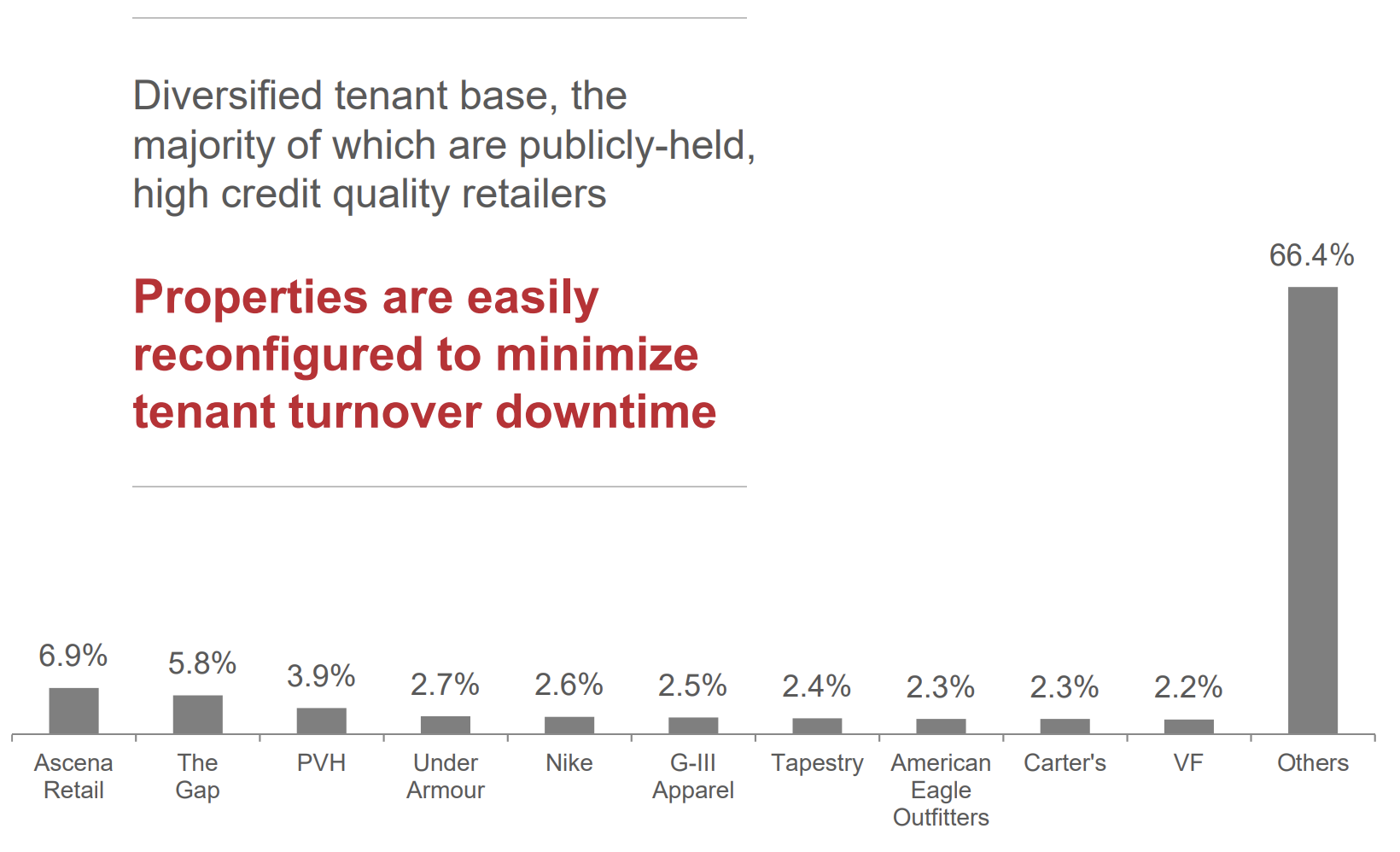

Tanger reported that its top 25 tenants generated 57.6% of its rent in 2018, and its largest tenants are well-known retailers such as The Gap (GPS), Under Armour (UA), and Nike (NKE). However, over 40% of its rent is generated from undisclosed retailers, many of whom are presumably struggling and focused on apparel.

Source: Tanger Investor Presentation

For example, earlier this year Gymboree and Charlotte Russe filed for bankruptcy. Both of these retailers are in Tanger's portfolio, accounting for just over 1% of its total square footage. However, neither of these customers were disclosed in Tanger's annual report, leaving investors to worry about other troubled tenants that could be the next to go belly-up.

Simon Property Group's CEO struck a cautious tone on the company's February 2019 call as well:

"There are some retailers out there that we're nervous about, I mean, so far in the first quarter bankruptcies are trending lower than they were in 2017 and 2018. However, there's some rumored things out there that could ultimately end up being at similar 2017 and 2018 [levels]. 2018, as we said, and as we look and anticipated 2018, we thought it would be less than 2017. We were ended up being right there, but I do think there will be more bankruptcies to come in 2019, and that's why we're relatively conservative as we look at our comp NOI..." – CEO David Simon

Should more tenants close their doors, Tanger's occupancy will dip and its rent spreads will struggle to hold their ground. Even though most of its stores are only 4,000 square feet and thus fairly cheap and easy to refill, it still takes time to bring in replacement tenants.

For now, management is hopeful that the parade of struggling specialty retailers is nearing an end, but only time will tell how structural this challenging environment might be:

"We have fought as other peers in our industry a disproportionately large amount of bankruptcies caused by over-leveraged buyouts of specialty retailers by the private equity industry. That seems to be sorting itself out now. There were two that were announced in the first part of the year, but we’re hopeful that it’s getting towards the end. That’s created an overhang. And as we’ve mentioned, our strategy is to keep the lights on. That space is being refilled." – CEO Steven Tanger

Let's review what these issues could mean for Tanger's dividend safety.

Is Tanger's Dividend Safe? Based on the information we know today, Tanger's dividend appears to remain on stable ground. On its February 2019 earnings call, management even noted that the firm expects to generate substantial cash flow after paying dividends this year, even despite the drop in NOI:

"We expect to generate $100 million in free cash in 2019 after paying of our dividend. Therefore, we feel comfortable in our ability to maintain a strong balance sheet with low leverage and with the safety of our dividend." – CFO Jim Williams

Like many REITs, Tanger reports several different cash flow measures – funds from operations (FFO), adjusted funds from operations (AFFO), and funds available for distribution (FAD). No matter how you slice it, the dividend appears to be reasonably covered in 2019 based on management's guidance:

2019 Estimated FFO Payout Ratio: 61%

2019 Estimated AFFO Payout Ratio: 72%

2019 Estimated FAD Payout Ratio: 63%

Even if you calculate free cash flow the old fashioned way, by taking cash flow from operations and subtracting out all capital expenditures, there appears to be a reasonable margin of safety.

In 2018 Tanger generated $258.3 million of cash flow from operations, similar to its results in 2017 ($253.2 million) and 2016 ($239.3 million). With management expecting FFO per share to decline by about 6% this year, we can assume cash flow from operations will likely fall by a similar amount to reach $242.8 million.

Tanger's capital expenditures totaled $64.3 million in 2018. With no new development projects in progress (an expansion to Nashville is likely several years away), spending will likely remain at a similar level. Management even guided for $36 million to $40 million of recurring capital expenditures this year.

Under these assumptions, Tanger's 2019 free cash flow would total $178.5 million:

2019 Estimated Cash Flow from Operations: $242.8 million

2019 Estimated Capital Expenditures: $64.3 million

2019 Estimated Free Cash Flow: $178.5 million

Tanger's annual dividend costs about $131.2 million, which would result in a 2019 free cash flow payout ratio of 74% and retained cash flow of $47.3 million.

Simply put, if management's 2019 guidance ends up being even close to correct, Tanger's dividend should remain covered by the firm's cash flow.

But what about Tanger's balance sheet? Sometimes companies with sub-100% payout ratios will still cut their dividends if they have too much debt.

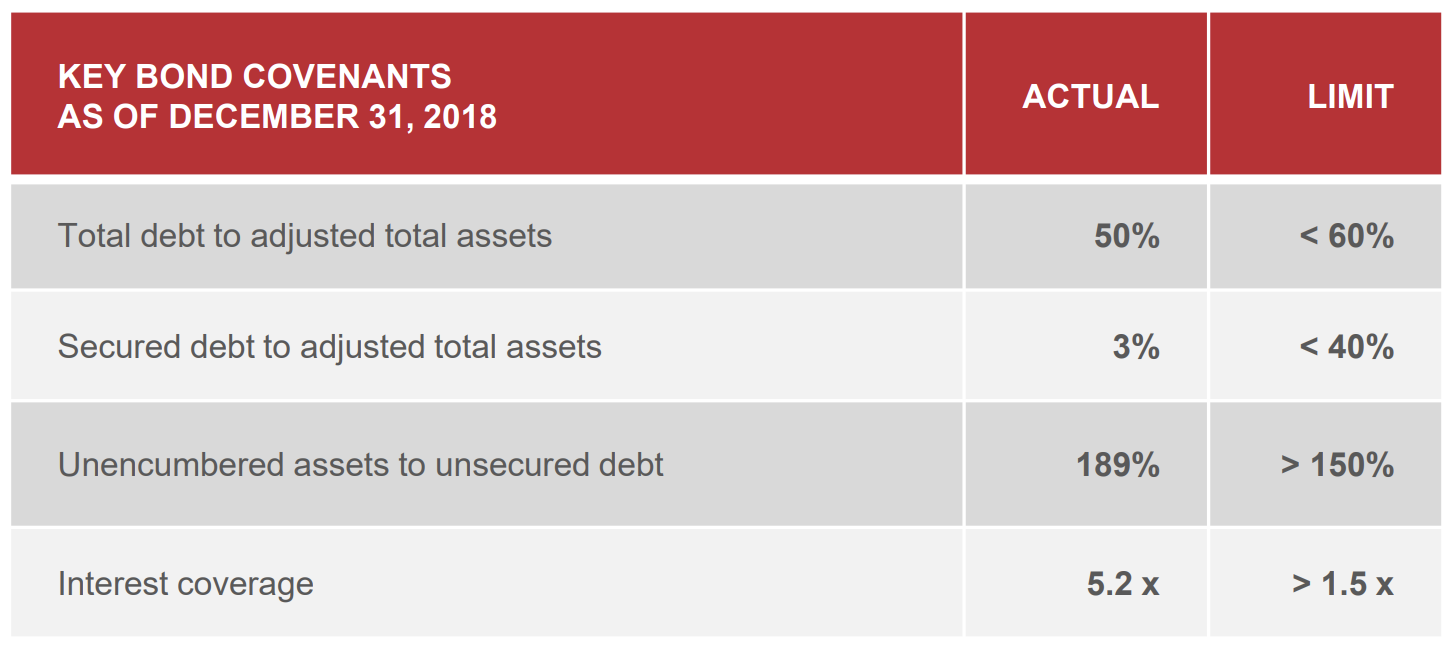

The good news is that Tanger's leverage metrics remain in compliance with its bond covenants.

Source: Tanger Investor Presentation

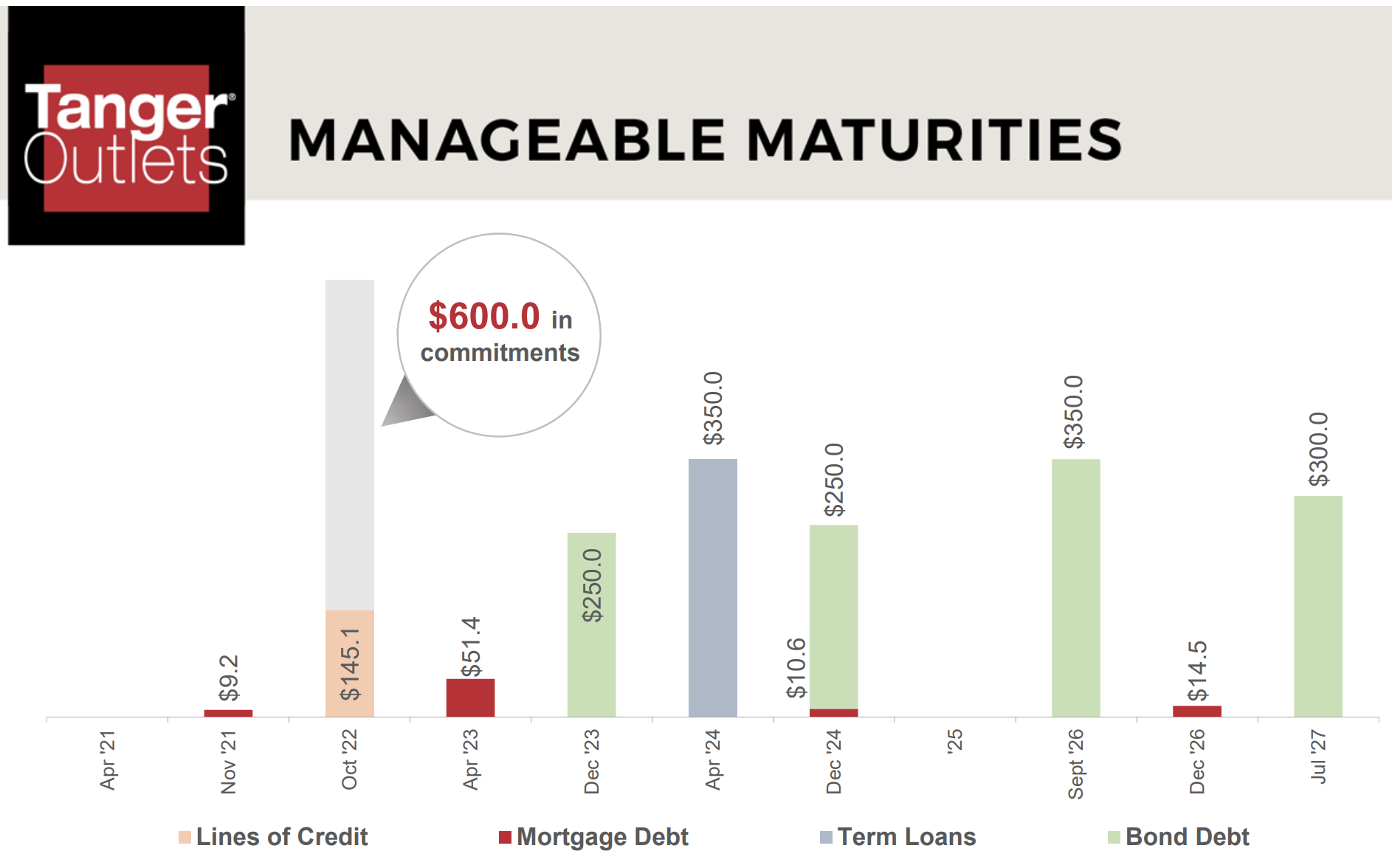

The firm also has no major debt maturities until late 2023, assuming its credit revolver is renewed prior to its October 2022 expiration. In other words, liquidity risk should be minimal for the foreseeable future.

Source: Tanger Investor Presentation

While Tanger maintains a solid investment grade credit rating, on March 12, 2019, Moody's revised Tanger's outlook to negative, writing:

"Today's rating action reflects Tanger's weakening operating performance as it continues to face pressure from recent tenant bankruptcies, store closures, and brand-wide retailer restructurings. Despite the REIT's sufficient liquidity position and coverage ratios, the company's operating results over the last 12 months are not commensurate with a Baa1 stable rated issuer. Management's 2019 guidance for lower occupancy levels and negative same store growth are also important drivers for the negative outlook...

Any positive rating action would require improved operating trends in SS NOI and occupancy levels (at least 95%) with sustainability. Maintenance of its current credit metrics, with net debt to EBITDA below 6.0x and fixed charge coverage greater than 4.0x, would also be needed."

Basically, should Tanger's earnings continue declining, its credit rating will likely be dropped a notch, although it would remain investment grade.

Tanger's net debt to EBITDA ratio stood at 5.9 at the end of 2018, just below the 6.0 level Moody's is watching. As a result, with NOI slipping this year, management will likely need to use the firm's retained cash flow to pay down some of the firm's $1.7 billion of debt.

If EBITDA declines by 6%, matching the expected rate of decline in FFO per share, management would need to reduce debt by about $100 million to maintain its 5.9 leverage ratio. That's the exact amount of excess cash flow Tanger expects to have this year after paying dividends.

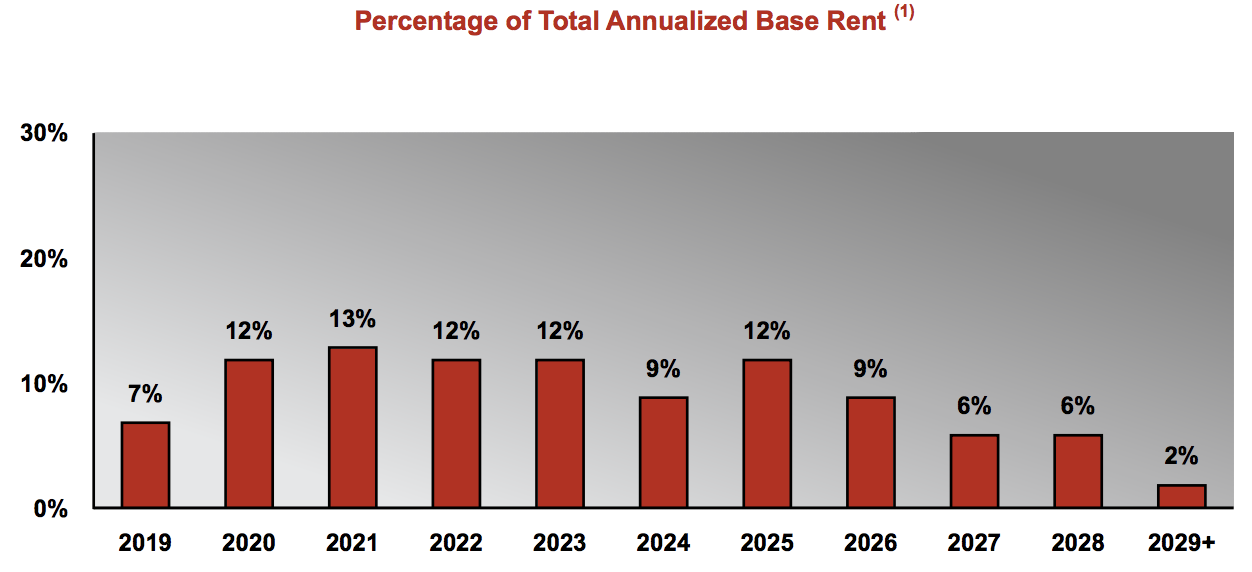

Basically, it's increasingly important that Tanger is not surprised by additional retailer bankruptcies, and the firm also needs to demonstrate it can renew its expiring leases at stable or higher rent rates (lease expiration schedule is below), proving its outlet-focused business model remains attractive.

Source: Tanger Investor Presentation

For now, management can continue paying the dividend. Tanger even raised its payout by 1.4% in February 2019. However, investors should not expect any meaningful growth during this turnaround. And if the environment for Tanger's apparel-focused retailers does take another leg down, then the firm's Dividend Safety Score would very likely be downgraded to a "Borderline Safe" rating.

Closing Thoughts on Tanger Tanger's high yield and long track record of paying growing dividends each year understandably has the stock on many income investors' radars. However, in many ways the stock looks cheap for a reason.

Tanger's operating results have significantly deteriorated in recent years, driven largely by its exposure to troubled apparel retailers. While Tanger's dividend still appears reasonably safe based on the information we know today, investors considering the stock need to closely monitor the health of Tanger's tenants going forward.

While additional retailer bankruptcies are already baked into management's 2019 guidance, it's hard to say whether this headwind is cyclical (a few over-leveraged and poorly managed apparel retailers) or secular (e-commerce and shifting consumer shopping preferences reducing the appeal of outlets). Only time will tell.

Given these uncertainties and Tanger's weak growth profile for the foreseeable future, shareholders should make sure they remain comfortable with the size of their positions. Our personal preference is to invest in other companies with clearer paths to long-term dividend growth and equally strong or better financial health. Apparel retailers generally do not fit this mold, and Tanger's recent results demonstrate its relatively high dependency on this dynamic industry.