Founded in 1927, W.W. Grainger (GWW) is North America’s largest business-to-business distributor of maintenance, repair, and operating (MRO) supplies. The company is essentially a middleman and distributes industrial products that help businesses keep their operations running and their people safe.

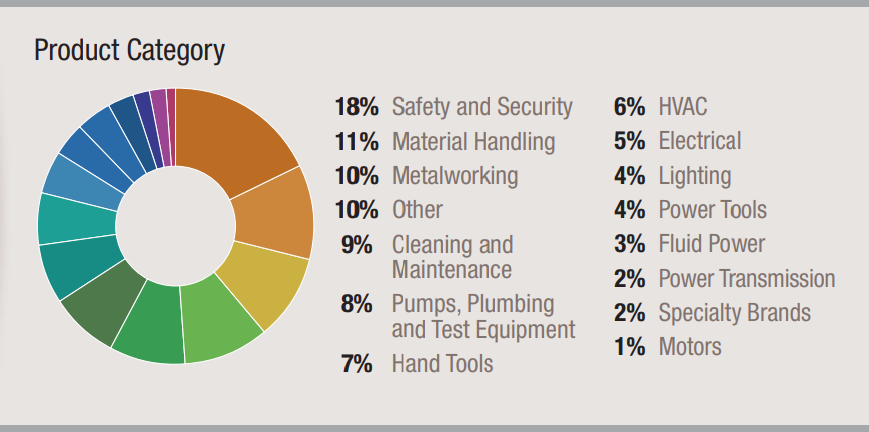

Grainger's 5,200 global suppliers provide the company with about 1.7 million products (material handling equipment, safety and security supplies, lighting and electrical products, power tools, pumps and plumbing supplies, cleaning and maintenance supplies, building and home inspection supplies, vehicle and fleet components, etc.), as well as inventory management systems.

Source: 2018 Grainger Fact Sheet

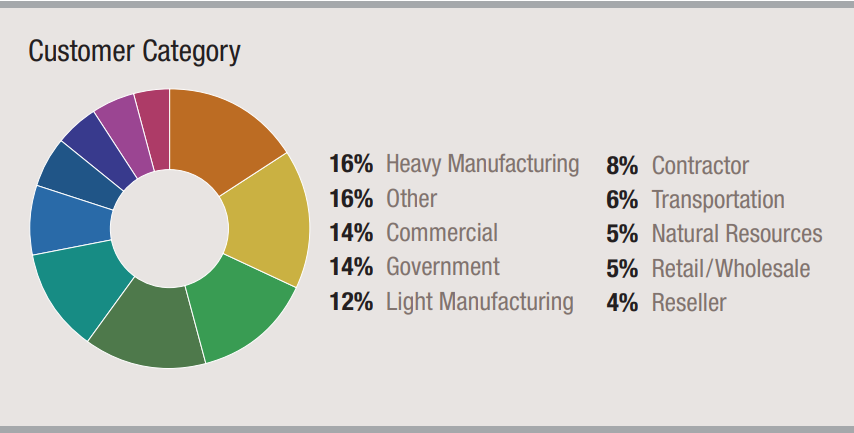

Grainger serves more than 3 million business, government, and institutional customers around the world. As you can see, the company's customer base is highly diversified and represents a collection of industries including commercial, government, healthcare, and manufacturing.

Source: 2018 Grainger Fact Sheet

Grainger operates both through online channels (60% of 2017 sales, up from 15% in 2009), as well as 500 global physical stores as of the end of 2017. The average customer invoice for Grainger’s products is about $300, and customers place orders over the phone, at local branches, online, and using mobile devices. Over 70% of the company’s sales are made to large customers.

Business Analysis

Grainger is a dividend aristocrat and has increased its payout each year since 1971. The company's success over the past decades has largely been driven by Grainger's large network effects and substantial economies of scale.

Specifically, the company’s massive supply chain and large global distribution network allowed it to become a “one-stop shop” that customers, both large and small, could depend on for reliable, just-in-time delivery of critical components needed to operate their businesses.

With the largest network of distribution centers and store branches in the country, Grainger is strategically positioned with localized inventory that is close to its most important customers.

Being in close proximity to customers helps Grainger deliver products to them very quickly, offer a high quality of service, and keep costs low. Competitors would need to acquire properties in the same service area to compete with Grainger, but they wouldn’t have the established book of business to cover all of their costs.

The mature state of the MRO market makes it very difficult for new players to crack into a geography already covered by a capable distributor to gain scale, somewhat limiting competition.

Grainger’s scale and inventory assortment are also advantages, especially in the large customer market which generates the bulk of the firm's business.

As the biggest player in North America, Grainger has somewhat better purchasing power than local or regional distributors. This allows it to offer very competitive pricing for its products, which are generally undifferentiated from one distributor to the next.

Importantly, Grainger’s size also enables it to afford an extremely broad selection of merchandise, making it a one-stop shop for large accounts that are constantly looking to save money by consolidating suppliers.

Grainger’s U.S. catalog offering has grown more than quadrupled from 82,000 SKUs in 2005 to 365,000 SKUs in the latest edition. Impressively, the time a product is in stock has remained at nearly 100% while increasing the product line substantially. With thousands of suppliers, this is no small feat.

Simply put, Grainger has historically enjoyed a wide moat, which allowed it operate a business model driven by high markups and volume discounts for its largest and most important customers. This helped the company enjoy consistent growth, big margins, and high returns on shareholder capital.

However, in recent years the ground has shifted under Grainger and the entire MRO industry. Historically, Grainger issued massive product catalogs to purchasing managers and relied on a steady flow of foot traffic and phone calls to its brick-and-mortar branches.

Source: Grainger Fact Book

While Grainger has invested in its online platform since the mid-1990s, the rapid shift online has still forced Grainger to adapt. For example, the company's sales made over the phone in the U.S. declined from 44% of revenue in 2012 to just 22% in 2017.

Stepping even further back, the distribution industry has been evolving for quite some time.

In fact, distributors’ share of U.S. GDP has fallen from 20% in 1995 to 14% by 2010, according to the Industrial Supply Magazine.

The magazine article goes on to state that “new, lower-cost models of distribution, retail entities entering into the traditional distribution chain, and e-commerce entities including Amazon, Google, and eBay are slowly eating away at the established model of business.”

Most notably, Amazon (AMZN) threw its hat into the industrial distribution ring in 2012 when it introduced Amazon Supply, which directly targeted the $377 billion MRO market in which Grainger operates in.

Amazon doubled down on its efforts to become a large-scale business supplier in 2015 by rebranding Amazon Supply into Amazon Business. Amazon Business sells hundreds of millions of products to businesses and generated sales of more than $1 billion in its first year.

An Amazon executive called Amazon Business a “top priority” for the company and identified only Grainger and Staples as its main competitors.

The executive also noted that Amazon has been “pleasantly surprised” by the response from large customers (Amazon Business originally focused on small and medium sized businesses) and is using custom pricing to differentiate versus Grainger’s less transparent pricing.

For many years, Grainger was able to substantially mark up the prices on inventory it acquired from its thousands of products manufacturers, enjoying fat margins and dependable profit growth.

The company’s large customers could receive nice discounts on the list prices in Grainger’s product catalogues, but it was still difficult to determine what a “fair” price was.

Amazon is looking to change all of that, bringing low-cost inventory from thousands of business supply vendors online, where pricing is transparent and comparison shopping is easy.

With industrial distribution rapidly migrating online (remember, Grainger’s e-commerce sales as a percentage of total revenue are up from 15% in 2009 to 60% in 2017), pricing games can no longer be played so easily.

That’s because, as Amazon founder and CEO Jeff Bezos likes to say, “your margin is our opportunity.”

Grainger’s CEO D.G. Macpherson has made it very clear that the rise of e-commerce and Amazon have begun to alter the way the company has to do business:

“We’ve had a very high-list, less-discount model. Large customers particularly valued getting discounts off of lists. We will continue to have that model, but our list prices are too high right now, so we’ve moderated some of those. The idea is that we have to be able to acquire customers through the Grainger brand, and you can’t keep digital marketing if the price you feature is always higher than everyone else…As product and price transparency has become more prevalent, it’s become a source of contention with customers and we don’t need that.” - D.G. Macpherson

Not surprisingly, Grainger's sales and earnings growth have been hurt in recent years. The company's operating margin has also fallen from 13.7% in 2013 to 11.1% in 2017.

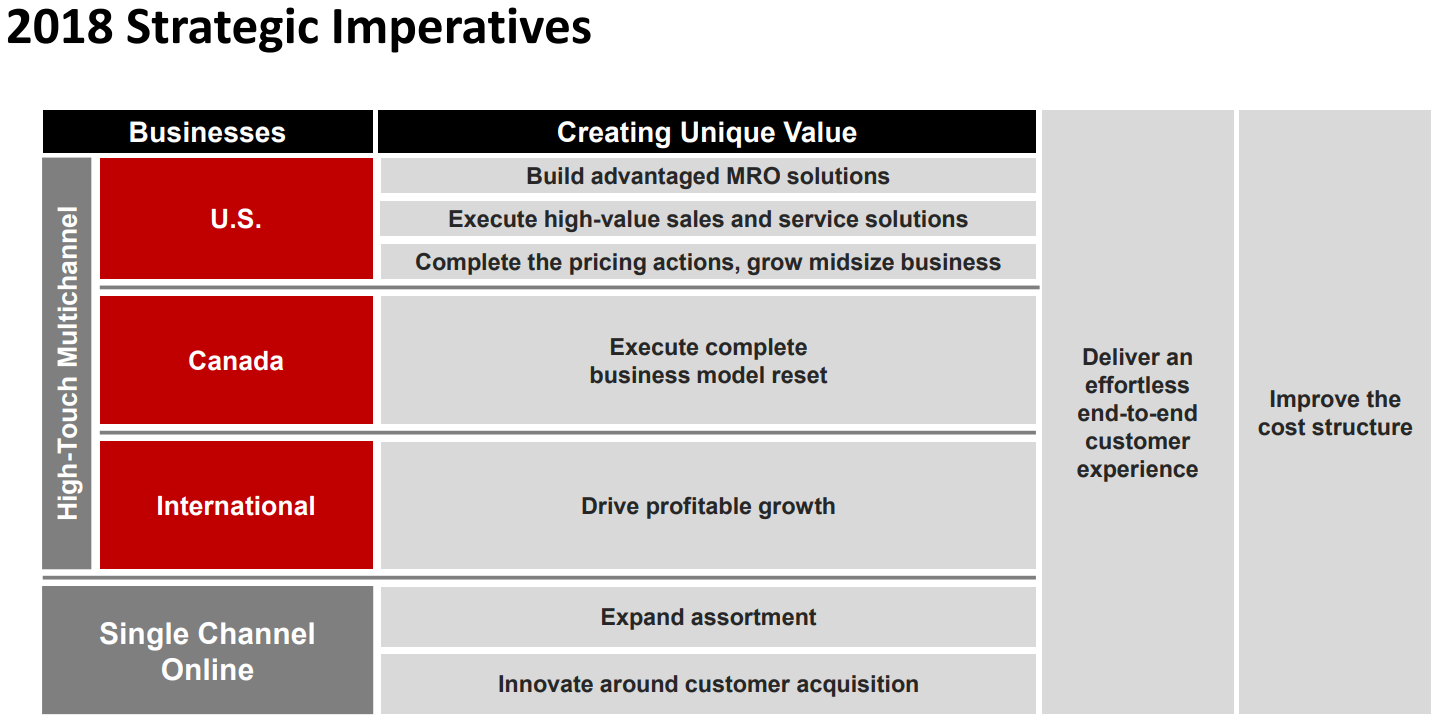

Fortunately, Grainger has a long-term plan for competing with Amazon, one that it believes can return the company to profitable long-term growth.

Source: Grainger Investor Presentation

Specifically, Grainger is moving towards a more transparent pricing model, with less emphasis on large-scale markups and preferential discounts for large customer contracts.

In essence, Grainger is now attempting to more directly compete on price with Amazon and its other rivals to protect its market share. Prior to the firm's recent pricing actions, Grainger estimated that 40% of its U.S. business was at less competitive prices.

Grainger decided to reduce its prices by up to 25% (including more competitive pricing on all of its 1.5 million online SKUs in the U.S.) to help retain its customers and drive better volume growth. While management had planned on gradually phasing in these price cuts through 2018, the company decided to pull forward almost all of those cuts into 2017, which weighed on the stock's performance.

While these price reductions were painful in the short term, they should help Grainger achieve its goal of winning market share. For example, after reducing its prices, U.S. volume grew 7% in 2017 and is expected to expand at a similar pace in 2018 and 2019.

Source: Grainger Investor Presentation

Besides implementing more competitive prices, Grainger is investing heavily into digital initiatives to keep its business relevant and growing. One example is Gamut, a website launched in 2017 to provide the best produce search experience in the industry. Grainger also maintains the industry's largest website and is North America's 10th largest e-commerce seller today, per Internet Retailer.

Of course, winning market share is easy if you just cut prices. So Grainger’s turnaround plan is also focused on leveraging its fast-growing e-commerce platform into one that better communicates with customers in real time and attempts to build a stickier ecosystem through a greater emphasis on services, especially supply chain management.

In fact, Grainger employs thousands of sales people and account managers who work directly with customers to help them place their orders and run their businesses more efficiently. It’s common for Grainger employees to visit customer sites several times per week to help them lower their costs and automate inventory orders from Grainger when their supplies get low.

Ryan Merkel, a William Blair analyst, also noted, “For a professional, a Caterpillar procurement manager, he cares about technical support, too much inventory, the line being down, the safety of his people. He values the ability to call the call center or have a Grainger person show up two to three times a week.”

Large customers, Grainger's core business, also tend to have more complex purchasing needs than small businesses, making Grainger’s high level of customer service more valuable and perhaps even more important than some of the prices it charges for various products. Grainger’s purchasing and inventory management systems are directly integrated with many large customers as well, increasing the stickiness of its relationships.

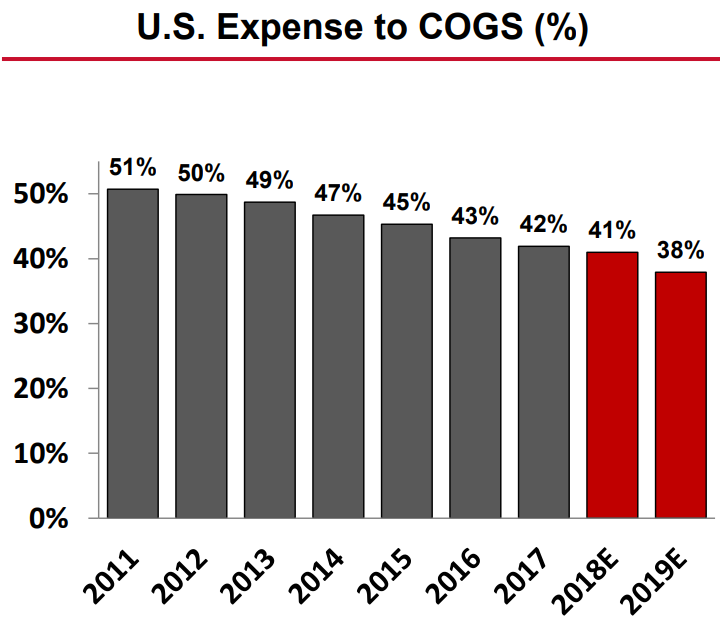

Meanwhile, in order to offset the margin compression that comes with lower prices, Grainger plans to take a combined $150 million to $200 million of cost out of the business in 2018 and 2019 (around 1.5% to 2% of sales). As you can see, Grainger has been improving its cost structure for many years by instilling a continuous improvement mindset to its culture.

Source: Grainger Investor Presentation

Cost savings from management's latest plan will come from supply chain improvements, contact center consolidation (reflecting less need to field sales calls), sales efficiencies, and efforts to return its business in Canada to profitability by shutting down physical store locations.

These actions all seem very reasonable since Grainger expects 80% of sales to come from its e-commerce platform by 2022, meaning that its brick-and-mortar outlets represent high overhead, low-hanging fruit when it comes to being able to maximize its sales at the lowest possible cost.

Combined with greater automation in its distribution centers and larger economies of scale in its supply chain (maximize cost savings with suppliers), Grainger thinks that it can achieve much better margins by 2019, including:

15% to 16% operating margins in the U.S., while achieving 8% to 9% volume growth

2% to 4% operating margin in its Canadian business (which is currently losing money)

8% to 10% operating margins in all other business units

Company-wide operating margins of 12% to 13% ( up from 11.1% in 2017)

Management expects mid-single-digit sales growth over the next several years to help the company hit its margin goals. Besides price-driven volume growth, Grainger is also banking on growing more with small and mid-sized businesses, which together account for more than 65% of the market. Grainger has done very well serving large, complex customers, but its presence with smaller customers has been more limited.

The company's single channel online businesses, MonotaRO in Japan and Zoro in the U.S., do a nice job of fitting the needs of smaller businesses given their simple customer experience and broad assortment of products across all categories.

Grainger's single channel online businesses have grown by 27% annually over the past three years and generate high returns on invested capital since they require little data entry work and are primarily shipped from distribution centers to bypass the branch network. These businesses will likely become an increasingly important earnings driver as digital growth accelerates.

If Grainger can execute on this turnaround plan, then it will mean not only faster top line growth, but also far better profitability than it enjoys today.

However, such a plan requires shareholders to be patient, as short-term sales and earnings growth could be more volatile than usual as the company adjusts.

Key Risks

While Grainger has a few things in its favor that should help it compete with major rivals such as Fastenal (FAST), Home Depot (HD), and Amazon, including a greater emphasis on higher-margin private label brands (22% of 2017 U.S. sales), investors must not underestimate the potential for ongoing margin compression.

Amazon Business is an especially key threat that is attempting to dominate the business-to-business (B2B) industry with a focus on rock bottom prices and supreme customer service (automated order flows, free shipping, and real-time order tracking).

As previously mentioned, Amazon specifically called out Grainger as one of its biggest rivals, has said that the B2B industry is a “top priority,” “must win” industry and is aiming to become the “preferred marketplace for all professional, business, and institutional customers worldwide.”

Unlike some other MRO companies, such as Fastenal, which focus on more premium, custom-built products, Grainger’s business is far more general and arguably commoditized, meaning that it could end up trapped in a race to the bottom on price with Amazon, especially given its focus on large accounts.

In other words, there is risk that Grainger's profitability peaked in 2013, and the company's best days could be behind it.

While increased competitive pressures are arguably the biggest threat to Grainger’s long-term earnings power, investors considering the stock should also remain aware that the company’s short-term results are sensitive to the industrial economy, which has struggled in recent years.

From low oil prices, to slower growth in China, to the strong U.S. dollar, numerous headwinds have impacted ordering trends and resulted in modest pricing pressure at many of Grainger’s customers. When growth is low, price competition can become fiercer between distributors as they look to protect market share and take out costs.

However, such macro factors shouldn't pose a threat to Grainger's long-term earnings power. At the end of the day, Grainger's impressive breadth of products, strong reputation, gradually expanding distribution network, and future acquisitions should help it continue growing.

While the overall health of the economy will dictate the pace and timing of growth, Grainger’s large and fragmented markets seem to offer plenty of opportunities. The real issue to monitor is where the company's long-term margins head.

Closing Thoughts on W.W. Grainger

While W.W. Grainger may never again be able to enjoy the kind of high margins it once did, its disciplined management team, strong balance sheet, and industry-leading customer network and relationships should allow the company to continue achieving steady, if slower, dividend growth in the coming years.

At the end of the day, Amazon is unlikely to be an existential threat to Grainger’s business, especially given the sheer size and fragmentation of the MRO market. However, increased price transparency and the continued rise of the online world could make Grainger more of a commodity company over the coming years.

Therefore, investors considering the stock may be best off waiting for shares of Grainger to offer a relatively high dividend yield compared to the past, or consider looking elsewhere for companies with stronger long-term dividend growth potential.