Why Newell Brands Looks Like a Risky Dividend Stock

Newell Brands (NWL) has had an "Unsafe" Dividend Safety Score for more than a year. Meanwhile, the company's stock price has fallen about 40% over the past year and is down 70% from its mid-2017 high. That's sent NWL's dividend yield soaring to its highest levels since the Financial Crisis when the company had to cut its dividend severely.

Source: Simply Safe Dividends

Unfortunately, Newell shareholders could be in for another dividend cut if business conditions don't turn around soon. Let's take a look at why the company is struggling and should be avoided by conservative income investors.

Newell Brands is Struggling with a Difficult Turnaround

Newell manufactures an eclectic assortment of consumer goods, including household products, cookware, baby gear, health products, candles, markers, highlighters, cleaning products, and more.

Like many consumer-facing companies, Newell has struggled with how to grow as e-commerce has disrupted many of the retailers that marketed its brands. The bankruptcy of some of those businesses, such as Toys 'R' Us, as well as increased pricing pressure from retailers struggling to manage their inventory levels, has caused Newell's organic growth to turn negative while operating margins have been cut in half since 2016.

Source: Simply Safe Dividends

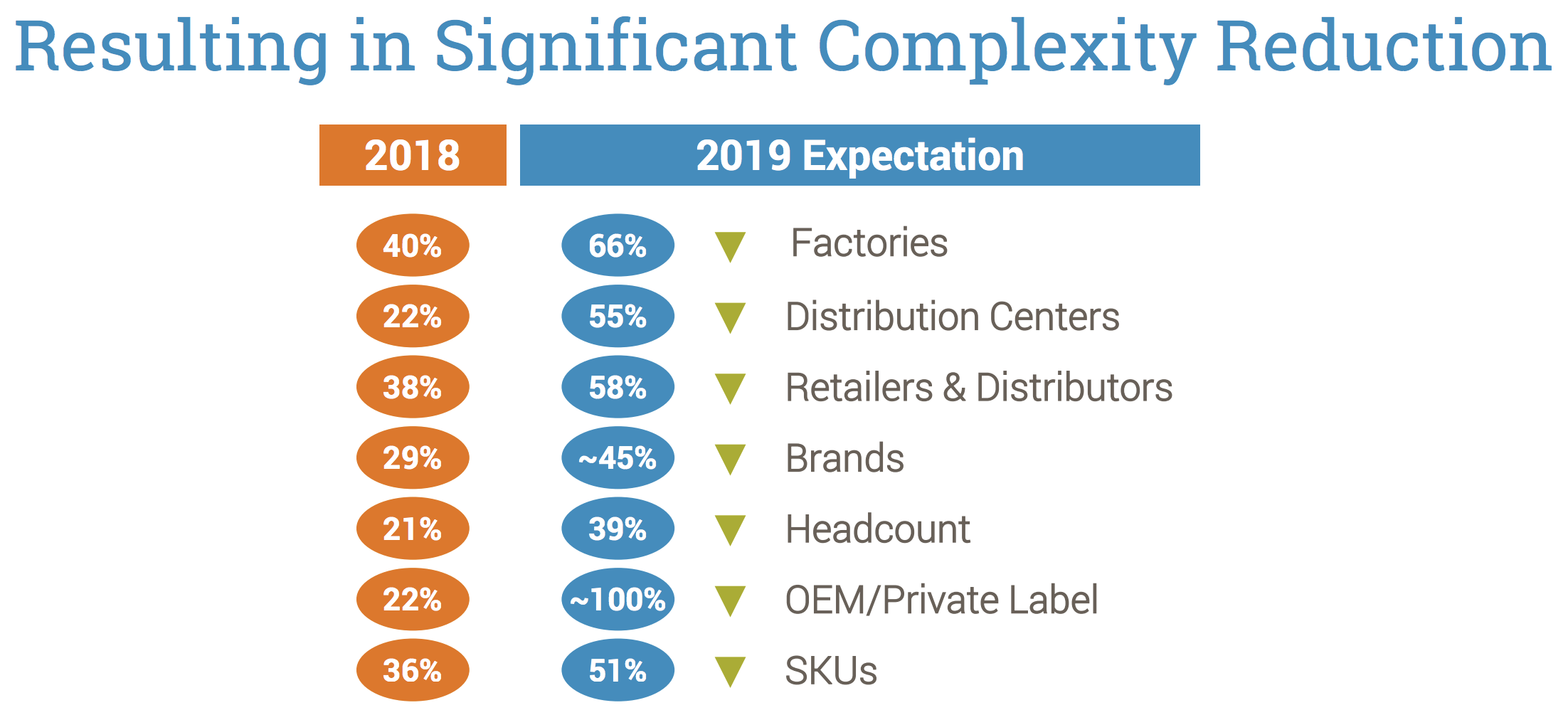

As a result, the company announced it was expanding its restructuring efforts in early 2018, with potentially 10 more asset sales to reduce its operating business count from 32 in 2016 to just nine (in 2017 it announced plans to cut its number of businesses to 15). That news caused the stock to plunge over 20% in a day, with some investors worrying that the company's falling cash flow might make deleveraging harder without a dividend cut.

In February 2018 Martin Franklin, former chairman of Jarden, a $16 billionacquisition Newell made in 2016, announced he was partnering with Starboard Value to launch a proxy fight to regain control of the company.

The proxy fight attracted the attention of another famed activist investor, Carl Icahn, who took a nearly 7% stake in Newell in early 2018. That relatively small stake was enough to get Icahn four board appointees, including a new chairman of the company.

Those board changes were part of a deal Icahn and Starboard Newell made in March 2018. In April Newell made a second deal with Starboard where it got to appoint two directors to the company's board in exchange for ending the proxy war. In late 2018 Icahn bought even more of the stock, boosting his stake to nearly 10%.

Essentially, Newell is now a company dominated by two activist investor groups, who aim to restructure the company in a massive way, including through the sale of $10 billion of assets in an effort to pay off the company's dangerous debt levels, boost profitability, and return it to organic growth.

“We believe that exiting non-strategic assets, reducing complexity and focusing on our key consumer-focused brands will make us more effective at unlocking value and responding to the fast-changing retail environment...A stronger, simpler, faster Newell, together with leading brands, brilliant marketing, outstanding innovation and an advantaged e-commerce capability, better positions us to win in these dynamic times.”

Newell has already made steady progress on that goal including the sale of five of its businesses for after-tax proceeds of $5.2 billion. In February 2019 the company announced the sale of Rexair, which generated $123 million in 2018 sales.

Source: Newell Investor Presentation

The asset sales executed so far allowed Newell to repay $2.6 billion in debt in 2018 as well as repurchase $1 billion in stock. In total, Newell says it will be done with asset sales by the end of 2019, resulting in a far smaller and simplified company.

Source: Newell Investor Presentation

However, while management's strategic plan might sound good in theory, the stock proceeded to fall nearly 20% when it released fourth-quarter earnings on February 15, 2019. Newell's report showed sales from continuing operations down 6%, and management guided for a further 3% to 5% decline in the first quarter of 2019 and low single-digit declines for the full year ahead.

The firm's CEO made clear that 2019 is going to be another tough year for the company, due to numerous challenges its been struggling with for years:

"We've planned 2019 to be another year of significant portfolio and organization transformation. We intend to drive the Accelerated Transformation Plan to completion in 2019, and despite the ongoing negative impact of retailer bankruptcies, foreign exchange, inflation and tariffs, we expect to stabilize and then reignite core sales growth, increase margins, and strengthen the operational and financial performance of the company."

According to its CFO, Newell expects total after-tax proceeds of $9 billion once all asset sales are complete by the end of the year, and management believes that the turnaround effort will eventually:

Improve gross margins by about 250 basis points (better product mix)

Reduce overhead expenses by about 4.5% of revenue

So what does all this boardroom drama and heavy restructuring mean for the safety of Newell's dividend? Unfortunately, the news doesn't look good.

Newell's Dividend Could be on Shaky Ground

During the last conference call, Newell's CEO said the company has "no plans to change the dividend." At first glance, that reassuring statement sounds good, especially given that Newell only has $7 billion in total debt remaining and will likely receive about $3.8 billion in remaining post-tax asset sale proceeds by the end of the year.

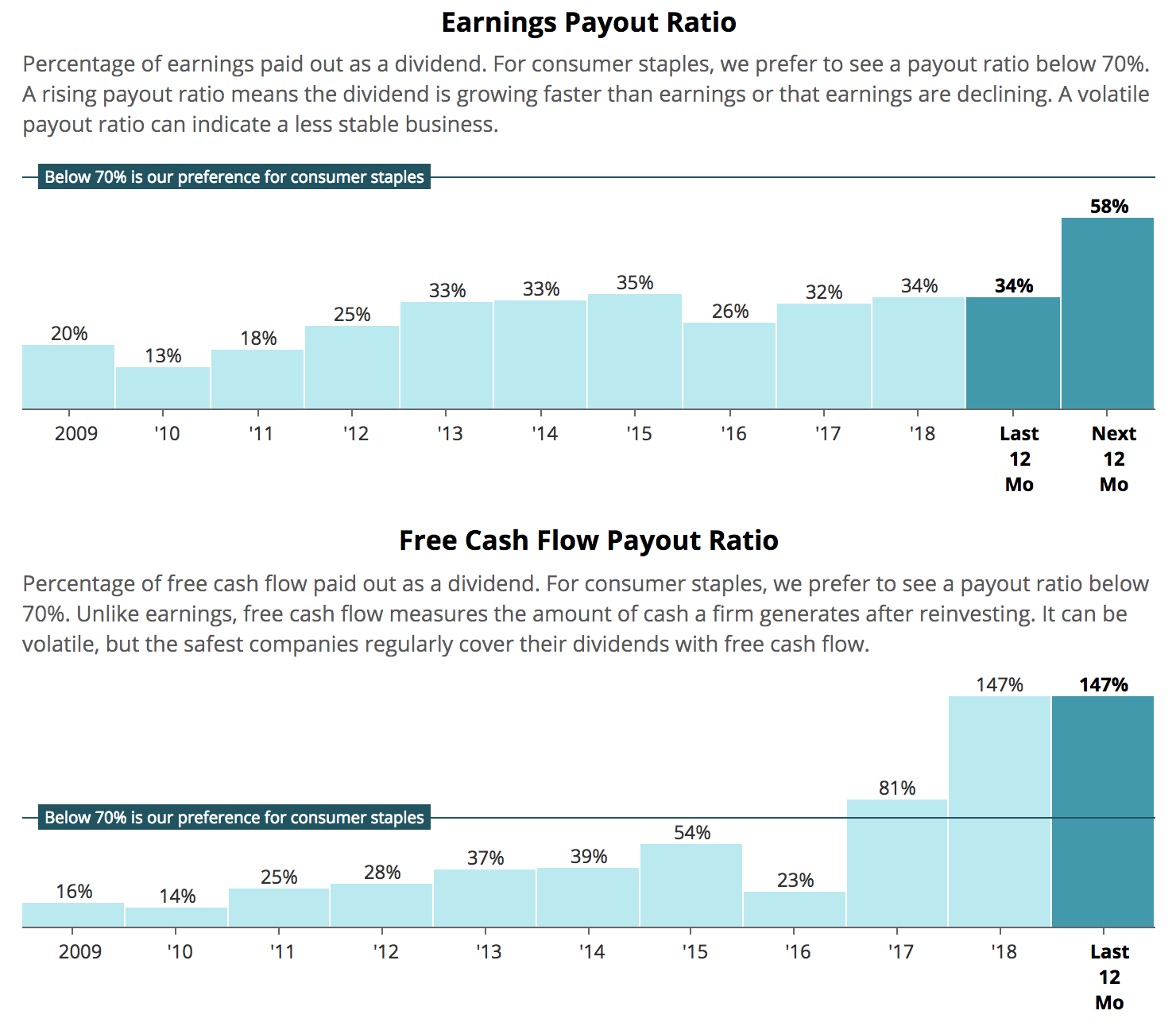

However, Newell's previous management had said it would like to keep the firm's adjusted earnings payout ratio at 30% to 35%, which is the company's historical norm.

Thanks to its substantial asset sales, plus difficult operating conditions persisting, Newell's EPS payout ratio is expected to soar way above that target in 2019, and its free cash flow payout ratio climb to dangerously unsustainable levels.

Source: Simply Safe Dividends

While most of the proceeds from asset sales are going towards paying down debt, Newell's net debt / EBITDA (leverage) ratio will remain at dangerously high levels. That's because the operating cash flow Newell is losing via asset sales is going to largely offset the lower debt levels. Even if Newell reduced its debt load by $4 billion this year, its net debt / EBITDA ratio would remain around 5.0.

Source: Simply Safe Dividends

Management is guiding for about $400 million in operating cash flow in 2019, and last year's dividend cost was $436 million. Sustainable dividends are paid out of free cash flow which equals operating cash flow less capital expenditures. Basically, management's guidance for 2019 calls for another year with a free cash flow payout ratio well above 100%.

The trouble is that debt is repaid with retained free cash flow (free cash flow minus dividends), and Newell isn't likely to have any in 2019. And as Moody's explained in August 2018, Newell's big turnaround plan is fraught with elevated risks:

"Moody's remains concerned about the strategic path Newell has followed over the past few years, and with regards to its future direction. In only the past few years the company has been through periods of high M&A, management and Board change, shareholder activism, and now material divestitures. The company is also entering into a period of heavy internal reorganization in both its manufacturing and employee base, as well as consolidating very fragmented management information systems. Such a high level of internal change creates a higher-than-normal risk of operational disruption."

Speaking of disruption, on March 4 Newell disclosed it would be unable to file its 2018 annual report on time since it needs more time to finalize its financial statements. This is clearly a complicated turnaround.

Newell currently has a BBB- credit rating from Standard & Poor's, which is a single downgrade away from junk bond status and needs to be protected in order to shield the company's already fragile cash flow from higher borrowing costs.

In order for Newell's dividend to be sustained management can't just sell its way to deleveraging and safety. The idea behind Newell's Accelerated Transformation Plan is to only sell the company's weaker, non-core brands while retaining the ones in which it has No. 1 or No. 2 market share position.

Source: Newell Investor Presentation

And once the weaker brands are gone the company will be able to focus its efforts on strong brands sold through thriving retailers using some of that "brilliant marketing and outstanding innovation" the CEO talked about in early 2018, to drive a return to positive revenue and cash flow growth.

While the asset sales so far put the company on track to complete the first part of its plan, management's 2019 guidance for negative core organic revenue growth doesn't bode well for Newell being able to achieve the kind of free cash flow growth that's required to both sustain the dividend and allow it to bring down its leverage ratio enough to potentially avoid a downgrade to junk.

Moody's has the company on a negative outlook already, and the operational risk it mentioned above is something that income investors need to keep in mind when considering buying or owning this stock.

After all, management's core organic growth guidance pertains to the brands it plans to keep. Leading market share positions don't mean much if a brand's pricing power is so impaired that sales and cash flow continue to decline in the future. Thus, until Newell can return to positive organic sales growth and a sustainable payout ratio, we consider the stock to be speculative and best avoided by conservative investors.

Concluding Thoughts

At first glance, Newell's Accelerated Transformation Plan sounds like it has potential to preserve the current dividend if management is able to execute well in 2019 and beyond.

However, as Moody's points out, the company's been dealing with a lot of drama in recent years, because thus far Newell has been unable to successfully adapt to the fast-changing retail environment created by the rise of e-commerce.

The firm's continued guidance for negative organic sales growth in 2019 indicates that Newell's turnaround efforts might extend far beyond this year. Meanwhile, the company's high debt levels might necessitate a dividend cut in order to divert free cash flow towards preserving an investment grade credit rating while also providing more breathing room for management to invest in Newell's remaining brands.

The past few years have shown that the wide moats Newell's brands once enjoyed are now eroding. The company's pricing power has fallen to the point where its ability to deliver safe and growing income over time has become questionable, so conservative dividend investors are likely better off looking at safer high-yield alternatives that don't face such a wide range of potential outcomes.