Campbell Soup (CPB) has had a "Borderline Safe" Dividend Safety Score since closing its $6.1 billion acquisition of snack company Snyder's-Lance in March 2018.

While this deal improved Campbell's diversification and overall growth profile, it also resulted in a significant spike in the company's financial leverage.

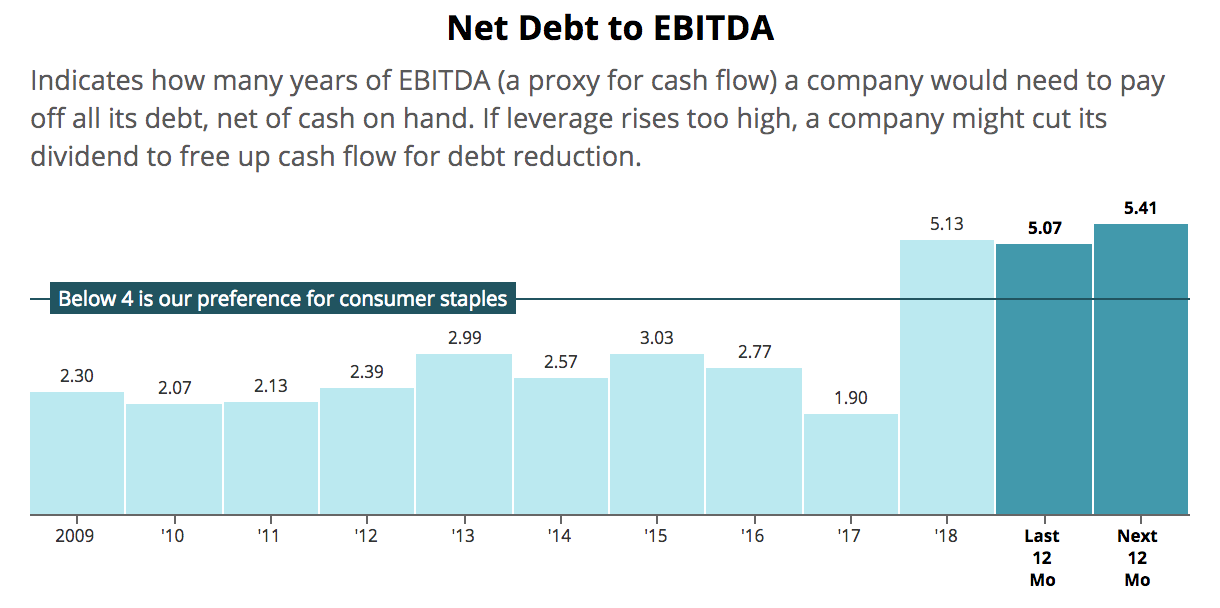

Source: Simply Safe Dividends

These situations will almost always put a company's dividend safety profile in our "Borderline" risk category. High leverage reduces a company's margin for error, and cutting the dividend is an easy lever to pull in order to strengthen the balance sheet.

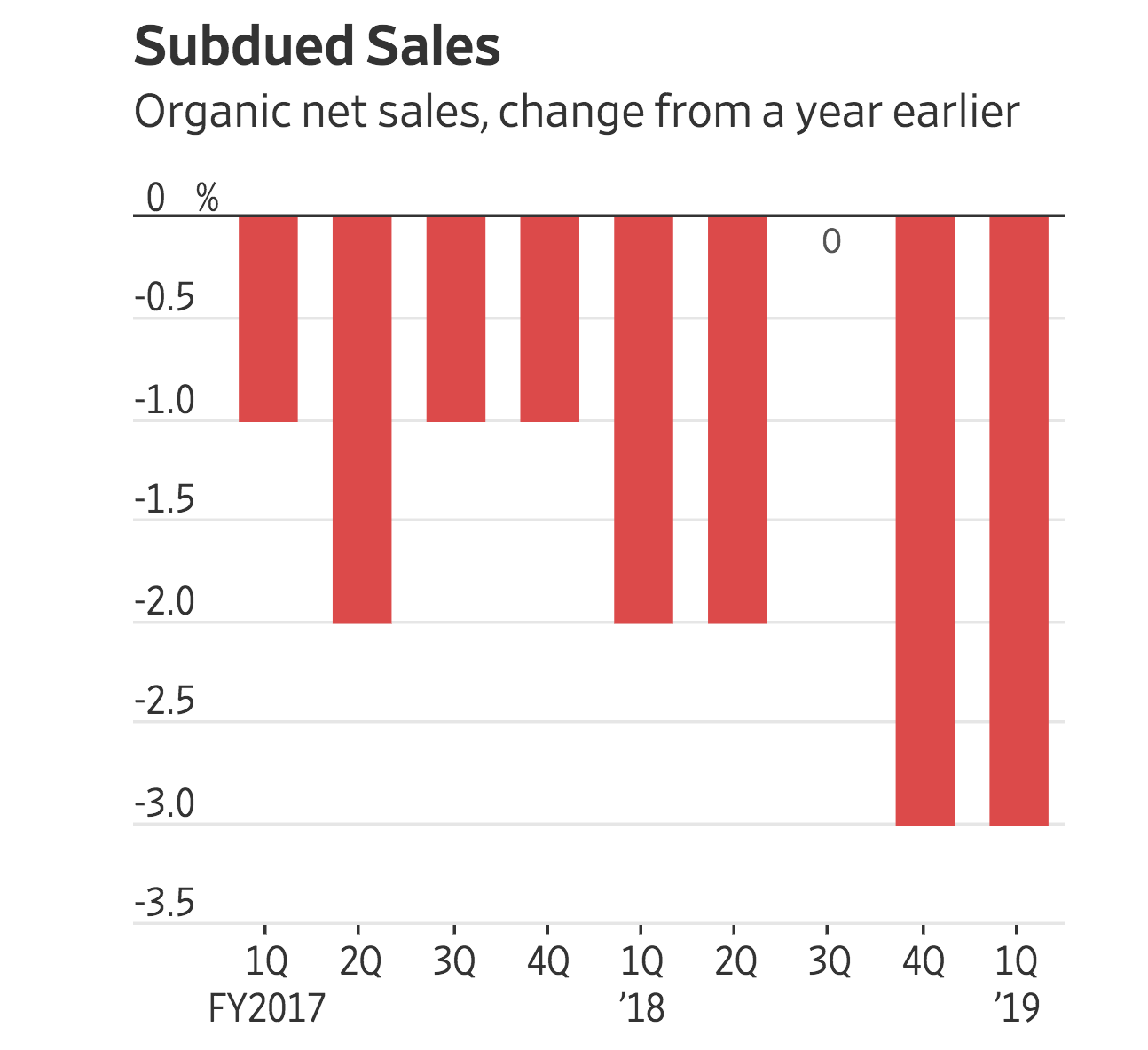

Campbell's use of leverage especially raised the stakes since the company's organic sales growth remains weak. The firm's namesake soup business in the U.S. continues losing market share to cheaper private label offerings, and consumers are opting for healthier foods as well.

Source: The Wall Street Journal

Pressure on Campbell came to a head last year. In May 2018, the company's then-CEO Denise Morrison abruptly resigned following poor earnings results. She had acquired a number of fresh refrigerated food brands in recent years to help offset some of the declines Campbell's canned soups and packaged foods were experiencing.

However, this strategy wasn't working. Not only were these "fresh" businesses much less profitable than Campbell's shelf-stable soup lines, but management was too inexperienced to achieve success in these new categories.

After replacing CEO Morrison, Campbell also announced it would take a strategic review of its business. Smelling blood in the water, activist investor Dan Loeb's Third Point revealed a stake in the company in August 2018. Loeb made a push to sell the company and later demanded to replace Campbell's entire board.

Simply put, a lot of change has taken place at Campbell over the past year. Whenever you have a combination of management turnover, high financial leverage, and slumping growth, a company's dividend safety profile becomes murkier.

One of the biggest factors supporting Campbell's dividend is the Campbell family itself. Campbell's heirs own over 40% of the company, as well as several seats on the board. They benefited immensely from the $426 million in dividends Campbell doled out in fiscal 2018.

Since Campbell's charter also requires two thirds of shareholders to approve a sale of the company, they also stand in the way of any attempts by outsiders to sell the business.

However, income investors may not be able to bank completely on the Campbell's heirs keeping the company committed to its current dividend. After all, in 2001 the iconic soup-maker slashed its payout by 30%, despite the Campbell's heirs owning over half of the company at the time.

"We have stumbled in the marketplace, weakened our connection with consumers and disappointed our investors," [CEO Douglas Conant] told a group of analysts.

Indeed, though Campbell leads the wet-soup category with roughly 70% of the market, it has failed to lift condensed-soup volumes over the past decade. In recent years, aggressive price increases and inconsistent marketing have enabled others to nibble at the company's market share. Campbell's stock has suffered a painful slide, falling from a high of $60 a share in 1998 to a low of $23.75 in September 2000...

As of July 30, the start of the fiscal year, Campbell will increase marketing expenditures 15% to $200 million, said Mr. Conant. It will spend an additional $100 million on capital improvements and invest more heavily in new product development.

In a widely anticipated move, the CEO also lowered earnings targets for 2002 by roughly 20%, to $1.30 a share.

An old article from CNN captured similar insights:

"The urgent need for transformation of our business is clear and compelling," CEO Douglas Conant said. "We have stumbled in the marketplace, weakened our connection with consumers and disappointed investors."

Conant told analysts during a meeting in New York Friday that the company is on track for 5 percent sales growth in the U.S. soup business, but acknowledged that Campbell alienated consumers by slashing advertising and pricing its soups too high relative to rival's brands.

"In our quest for ambitious EPS targets we simply pushed the envelope too far in pricing. We did not do enough to keep ahead in the quality race and let competitors begin to close the gap," Conant told analysts.

In 2001, Campbell's dividend cut came as a surprise due to the company's reasonable payout ratio and solid balance sheet. By our estimates, Campbell's leverage ratio sat near 2 (versus about 5 today), and its payout ratio was 56%. Even after management's downward revision to earnings, Campbell's payout ratio was just below 70%.

With Campbell's appointing a new CEO in December 2018, agreeing to add two of Third Point's nominees to its board, continuing to experience declines in soup (down 6% last quarter), and maintaining significant leverage, could investors be looking at another dividend cut in the near future?

It's possible, since you never know what management shakeups like this can lead to. For now, unless results have significantly deteriorated over the last quarter (similar to Kraft Heinz's situation), management's plans do not include a dividend cut. As discussed on last quarter's earnings call, Campbell has plans in motion to refocus on its core businesses, divest non-core operations to help with deleveraging, and continue taking costs out of the business:

"As you'll recall, we announced on May 18, that the Board was launching its own strategy and portfolio review process, one with outside advisors and which all options were on the table. Together with those advisors, we evaluated a full slate of potential options for Campbell, including optimizing our portfolio and divesting assets, splitting the company in two and selling the entire company.

After considerable analysis and evaluation and as discussed on August 30, the Board concluded that at this time, the best path forward to maximize shareholder value and maintain flexibility going forward is a three-pronged strategy. First, optimize our portfolio and focus on our core businesses with an emphasis on execution; two, divest certain non-core businesses in order to focus the Company, while significantly paying down debt; and three, to increase our successful multi-year cost saving efforts, while driving improved asset efficiency."

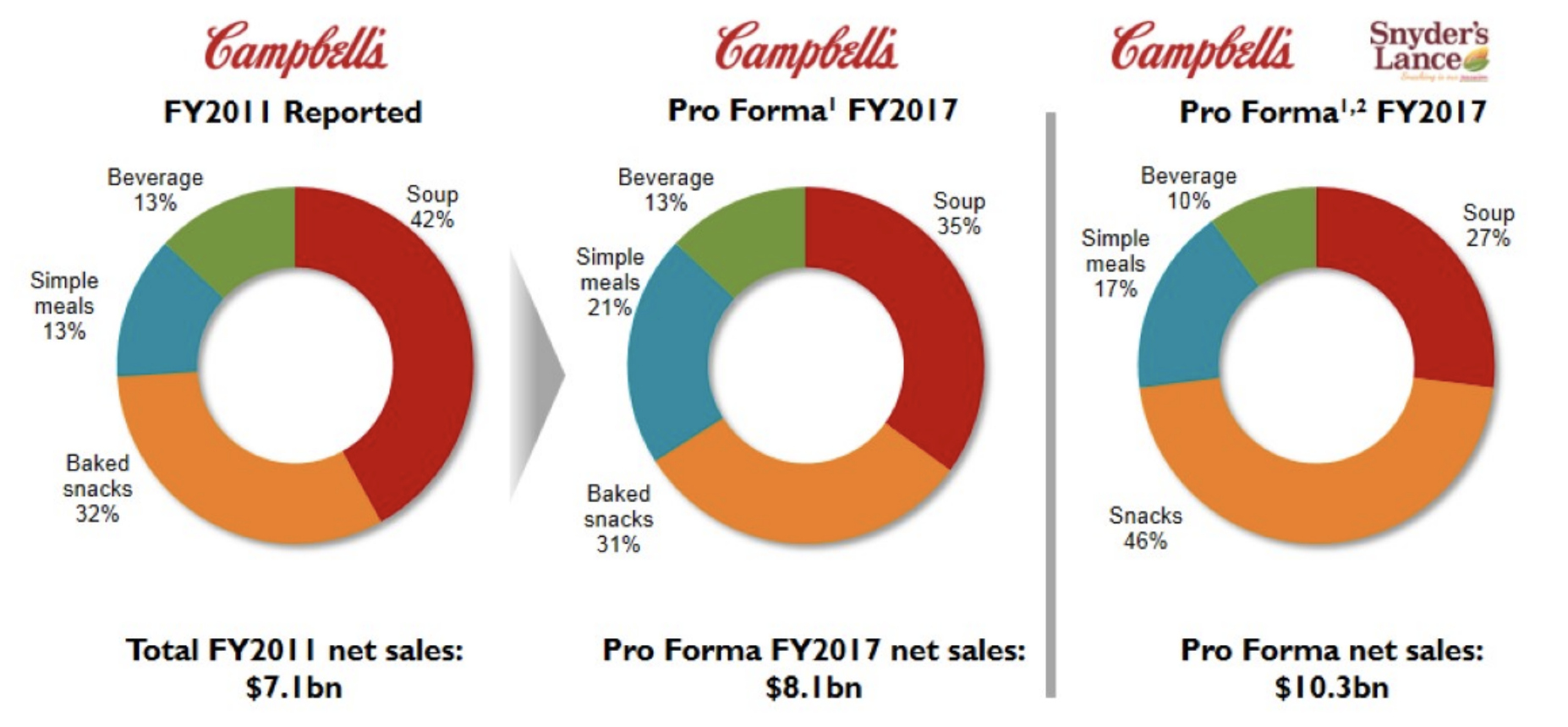

Compared to 2001, when U.S. soup accounted for over 80% of Campbell's total profits, the business is fortunately much more diversified today. Following its acquisition of Synder's-Lance, soup dropped below 30% of Campbell's overall sales.

Source: Campbell's Investor Presentation

Although shelf-stable soup carries higher margins and thus accounts for a larger share of overall profits, Campbell is much less anchored to one product category than it was back in 2001 when it cut its dividend.

In fact, Campbell notes that close to half of its overall sales are "large and exciting brands" that are outpacing category growth. While management still expects organic sales to decline slightly in fiscal 2019, there is potential for longer-term improvement across the firm's food portfolio.

Source: Campbell Annual Report

What about Campbell's debt load? We've seen several dividend cuts over the past year alone related to company's desires to accelerate their pace of deleveraging. Campbell's leverage is certainly a valid concern.

Campbell's net debt totals approximately $9.9 billion. Analysts estimate the company will generate EBITDA of $1.8 billion in the year ahead, resulting in an uncomfortably high net debt / EBITDA ratio north of 5.

Fortunately, management has plans to get the company's leverage ratio back to 3.0 by the end of 2021. Two divestitures are expected to take place this year, shedding $2.1 billion of sales (and largely undoing Campbell's earlier foray into fresh refrigerated foods). Given that Campbell generated $8.7 billion in fiscal 2018 revenue, these are significant transactions.

However, the Campbell Fresh business actually lost money last year, so anticipated earnings dilution from the divestitures is modest. Management believes adjusted EPS will sit between $2.40 and $2.50 this year, compared to its current annual dividend of $1.40 per share (about a 57% payout ratio).

It's hard to say what these struggling businesses will sell for. If they sell for just 1.25 times revenue, proceeds would be $2.1 billion. In that conservative scenario, Campbell could lower its debt by more than 20% and reduce its leverage ratio to about 4.1, according to our estimates.

That's still on the high side, but it provides a much better foundation for management to deliver on its goal of achieving a 3.0 leverage ratio target by the end of 2021. To help get there, Campbell will need to funnel the vast majority of its retained free cash flow to debt reduction while also banking on moderate (low single-digit) EBITDA growth, largely driven by cost cutting and merger synergies.

In fiscal 2018, the company generated $1.3 billion in cash flow from operations, invested $407 million in capital expenditures, and paid $426 million in dividends, leaving $472 million available for debt reduction. If Campbell can hold this level of retained free cash flow while slightly growing its EBITDA beyond 2019, it can hit its deleveraging goals without cutting its dividend.

In May 2018 when Campbell was first discussing its strategic review, CFO Anthony DiSilvestro was supportive of the payout's safety:

"But with respect to the dividend, two things I can say. We have a well-articulated priority for the uses of cash. It starts with reinvesting in our business and capital expenditures. Second is the dividend. And third, in the current environment, is to reduce leverage by paying down the debt. We have a robust and significant cash flow, which we fully expect we will continue to maintain a competitive dividend level and to have that dividend increase over time with earnings. So I think the management team as well as the board certainly supports the continued payment of a competitive dividend, and we see nothing that we're looking at that would change that at all."

Of course, talk is cheap, and a permanent CEO is now in charge since December 2018. There's a chance capital allocation prioritizes could change. Should Campbell encounter any meaningful, unexpected headwind this year that reduces its cash flow outlook, the pressure on the dividend could rise.

After all, on the company's first-quarter fiscal 2019 earnings call management noted they were open to "all" strategic options:

"The Board and management team are committed to look deleveraging the Company, maintaining our investment grade credit rating and rewarding our shareholders through long-term earnings growth and competitive cash dividends.

I also want to reiterate that the Board remains committed to evaluating all strategic options if they can demonstrably enhanced value above and beyond the significant actions that we are currently undertaking."

Income investors considering Campbell need to be aware of these uncertainties as the company embarks on a transition year. The cost inflation environment remains challenging for most packaged food businesses, and the headwinds ailing Campbell's soup business seem likely to linger (though they are already baked into management's 2019 guidance to some degree). The stock could remain more volatile than usual as investors digest each news update on the business.

Our preference would be to invest in other companies that have financially stronger operations, no governance concerns, and more proven track records of creating long-term value for shareholders. Consider that over the last 20 years Campbell has delivered a total shareholder return below 20%, while the S&P 500 has nearly tripled in that period, according to CNBC.

Campbell remains exposed to several product categories which appear to face structural growth headwinds. While a successful turnaround could restore some of the stock's valuation multiple, it's hard to imagine this business achieving its long-term targets (1-2% organic sales growth, 7-9% adjusted EPS growth). Combined with the firm's high debt load and weak managerial track record (another victim of cutting costs too far at the expense of brand equity and product innovation), investors may want to look elsewhere.