Reviewing Kellogg's Dividend Profile and Underperformance

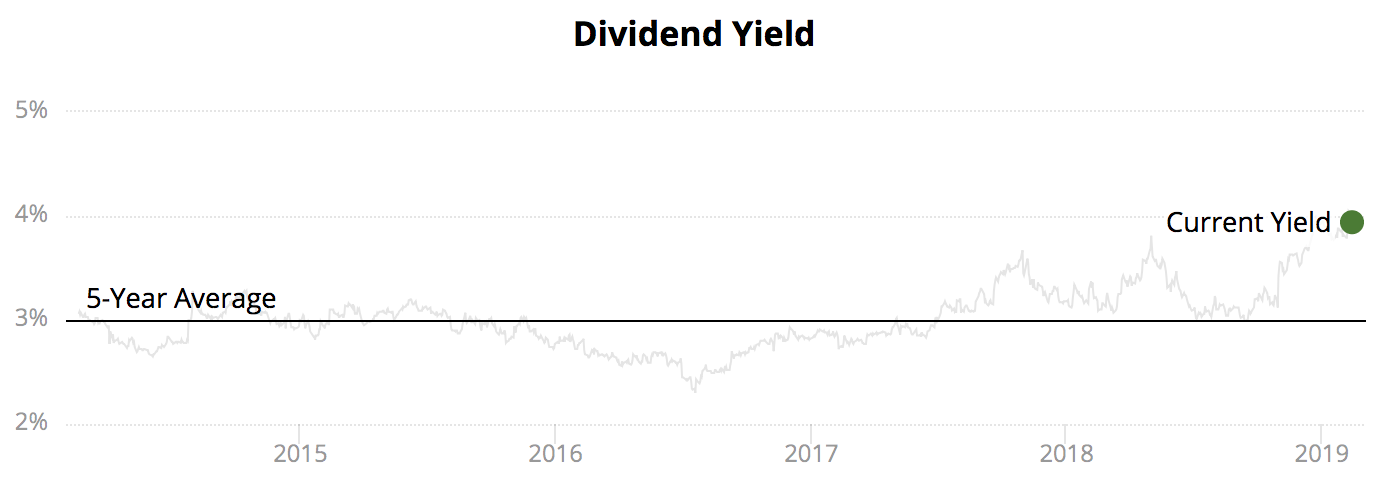

Kellogg (K) shares have slumped over 20% since September, sending the stock's dividend yield up to about 4%, its highest level in 19 years.

Source: Simply Safe Dividends

With Kellogg's earnings expected to decline close to 10% over the next year, plus the company's somewhat elevated debt load, let's take a closer look at Kellogg's dividend safety and long-term outlook.

Why Kellogg's Shares Have Suffered

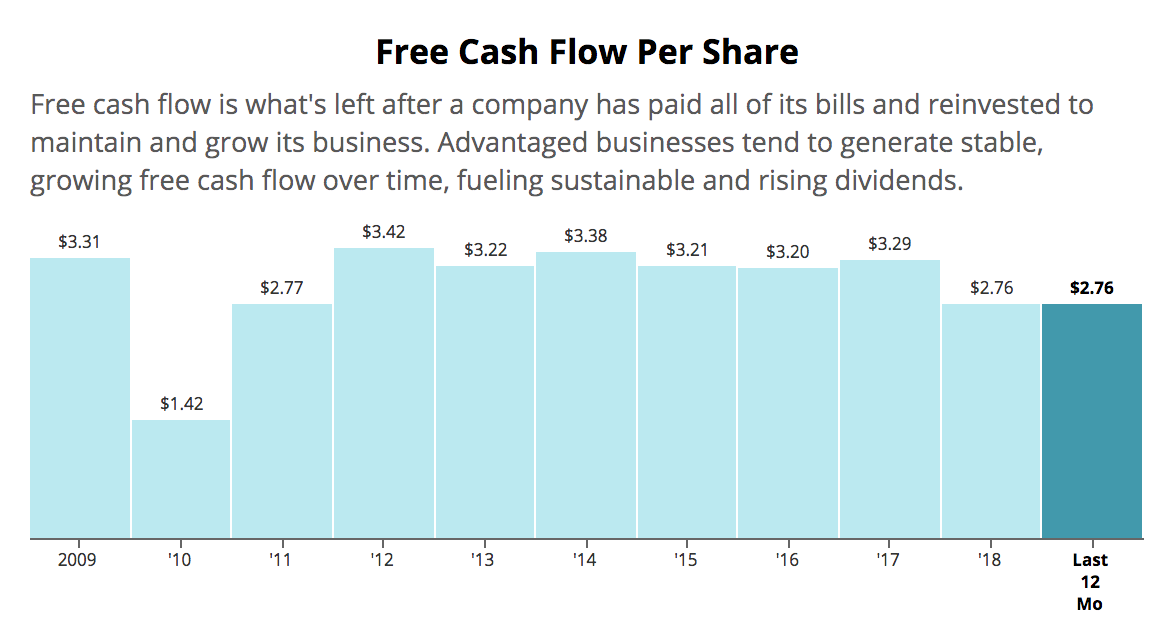

The consumer packaged goods industry isn't known for very fast growth, but in recent years Kellogg's sales and free cash flow have taken a hit. The company's revenue declined by 1.9% annually over the past five years, and in 2018 Kellogg's free cash flow per share fell to its lowest level since 2009 despite a decade's worth of share buybacks, cost-cutting programs, and modest (+7%) sales growth.

Source: Simply Safe Dividends

Like many of its peers, Kellogg has struggled to adapt to shifting consumer preferences, especially as food shoppers become more health conscious. Changing consumer tastes are especially rippling through North America (-2% organic sales growth in 2018), Kellogg's core market which generates about 60% of its sales and an even larger share of profits.

Most recently, Kellogg's stock fell nearly 6% on February 9 when its latest earnings result disappointed investors.

Specifically, the 0.6% organic sales growth rate the company posted was a sign that its core brands across the cereal, chip, cracker, and snack bar categories continue to struggle in the new packaged food environment. And that weak growth was despite a strong push into emerging markets and acquiring fast-growing, health-focused brands in recent years (more on this in a moment).

Worse still, the company's 2019 guidance was far from reassuring to investors who worry that Kellogg's best days are behind it. Here are management's expectations for the year ahead:

Overall currency neutral sales growth 3% to 4%

Organic sales growth 1% to 2%

Adjusted operating profit: 0%

Adjusted EPS: -5% to -7% (due to a higher expected tax rate and a write-down on pension assets)

Achieving stronger organic sales growth is not much of an accomplishment when it comes at the expense of profit growth. Simply put, Kellogg is not yet demonstrating an ability to return to profitable growth, suggesting its once powerful portfolio of brands could be fading in relevance.

With a better understanding of Kellogg's disappointing financial results, let's take a look at management's plans to get the company back on track.

Kellogg's Turnaround Plan

Kellogg's turnaround plan is built on a multi-pronged approach. That includes acquisitions of brands that are "on trend" with today's consumers. One of the company's most notable deals took place in 2017 when Kellogg paid $600 millionfor all-natural protein bar maker RXBAR.

As CEO Steve Cahillane told analysts on Kellogg's fourth-quarter 2018 conference call:

"We acquired RX in late 2017 and in 2018 we expanded its distribution, doubled its small brand awareness and extended its product line. This is a new growth platform for us."

In addition, to offset weak growth in the saturated U.S. market the company boosted its exposure to emerging markets by acquiring larger stakes in its West African operations. According to its CEO:

"Emerging markets will be a growth driver for years to come and in 2018 we accelerated our organic growth in these markets to a high single-digit rate."

The company also ramped up advertising (about $1 billion per year, or 7% of revenue) in an effort to revitalize its brands. Management says this is a multi-year effort that will continue for the foreseeable future.

Meanwhile, in foreign markets, the company is actually enjoying decent organic growth including:

3% in Europe (thanks to the reintroduction of Pringles and expansion into Russia and the Middle East)

7% in Latin America (fueled largely by a thriving Brazilian business)

5% in Asia Pacific

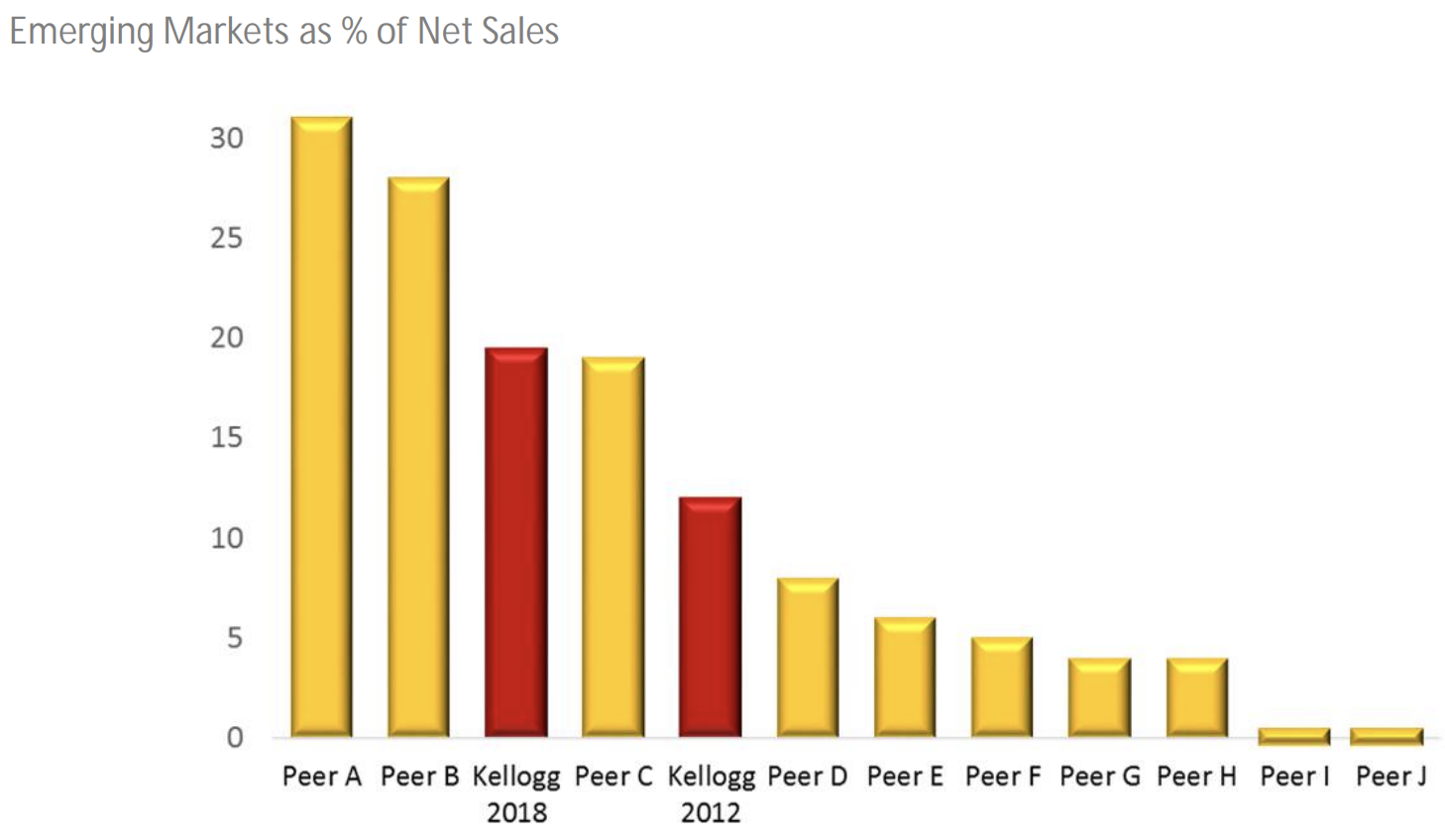

In fact, thanks in part to a $420 million deal in 2018 to expand its African business, a higher proportion of Kellogg's revenue (nearly 20%) is derived from emerging markets than all but two of its peers.

Source: Kellogg Investor Presentation

But targeting stronger overseas growth and expanding its healthier brands are just two parts of a three-pronged strategy to restore the company to profitable growth.

The final element is cost cutting, specifically "Project K" which was launched in 2013 and designed to both streamline Kellogg's supply chain, as well as make it easier to leverage its stronger performing brands into new product launches. Management's goal was to cut $475 million in costs (3.5% of revenue) due to those efforts.

In 2017, Kellogg also shifted from a direct-store distribution model (for about 25% of its products) to one based on warehouses (like most of its rivals use). By the end of 2019 this lowered operating costs by approximately $650 million, representing about a 6% decline in cost of goods sold.

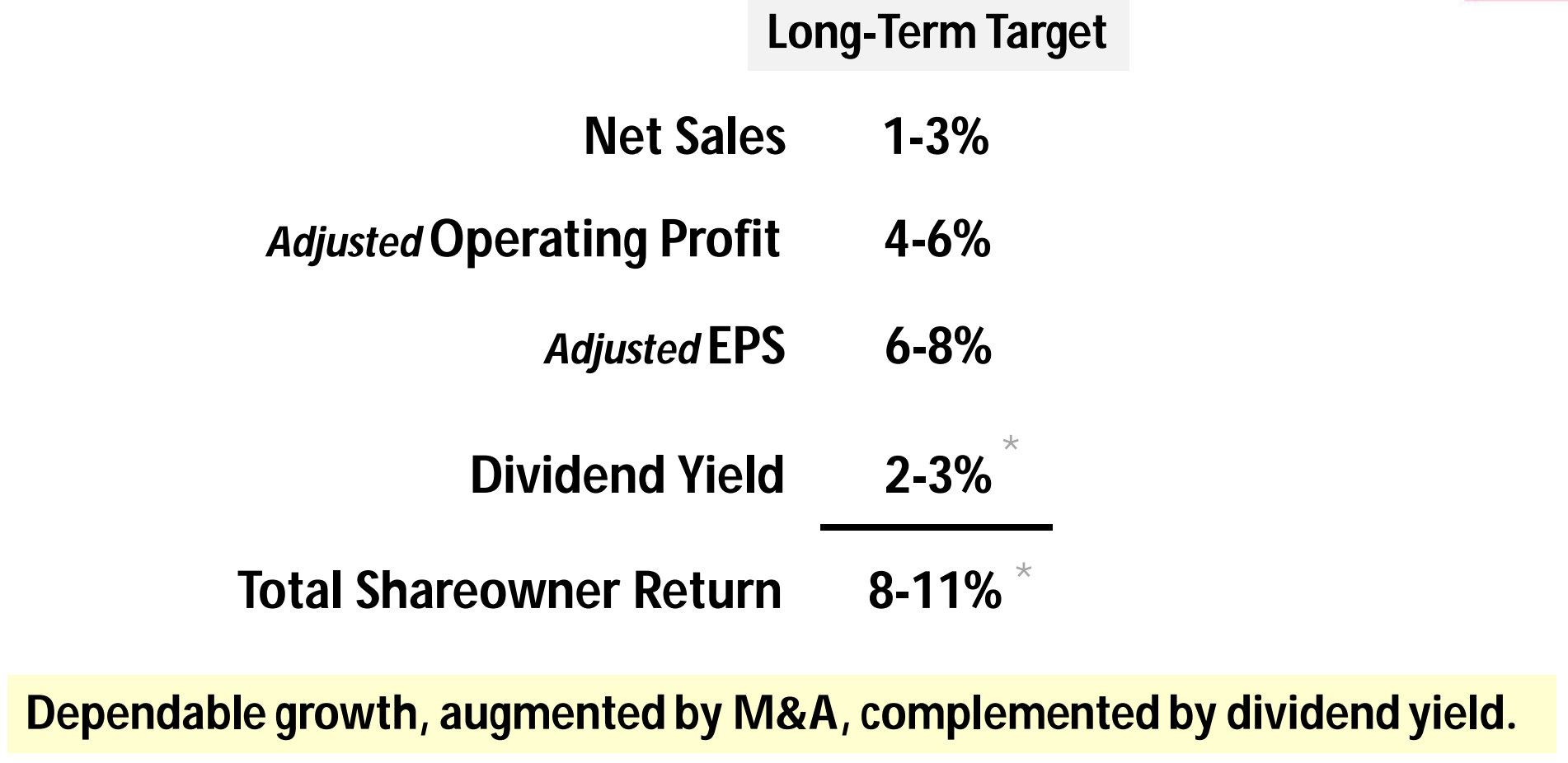

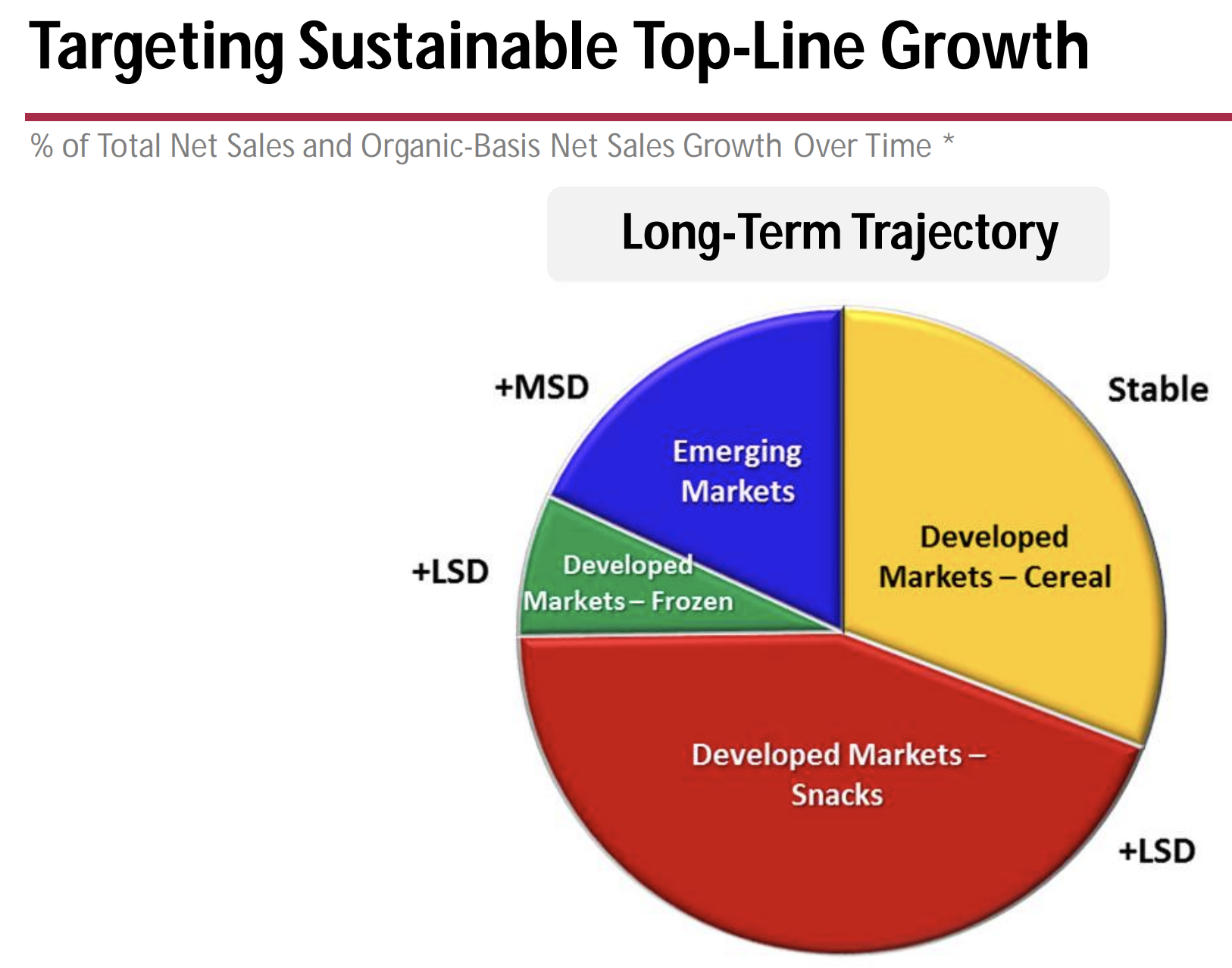

Over the long term, management expects that a reshuffling of its brands, combined with stronger growth overseas and ongoing cost-cutting activities, will help drive long-term adjusted EPS and dividend growth of about 7% per year.

Source: Kellogg Investor Presentation

Profitable growth is expected to be driven by focusing more on snacks, frozen foods, and emerging markets, which are all expected to grow at a low to mid single-digit pace while cereals will hopefully remain stable.

Source: Kellogg Investor Presentation

Kellogg's Dividend Profile So with management presenting such a clear turnaround plan, is Kellogg an attractive long-term dividend growth investment? Not necessarily.

While Kellogg has seen solid growth overseas, its core North American market and heavy reliance on cereals (a stagnant industry) mean that management's long-term growth forecast might prove overly optimistic.

Kellogg appears to have underinvested in many of its brands for years, showing little in the way of new product innovation or meaningful marketing campaigns. Only now is management attempting to play catchup (e.g. higher advertising spending) while also seeking out more acquisitions of trendy products.

It remains to be seen if Kellogg's higher spending will improve its long-term outlook for profitable growth, but these actions will likely result in even smaller dividend increases going forward (Kellogg's dividend has never grown very fast to begin with, about 4% per year for two decades).

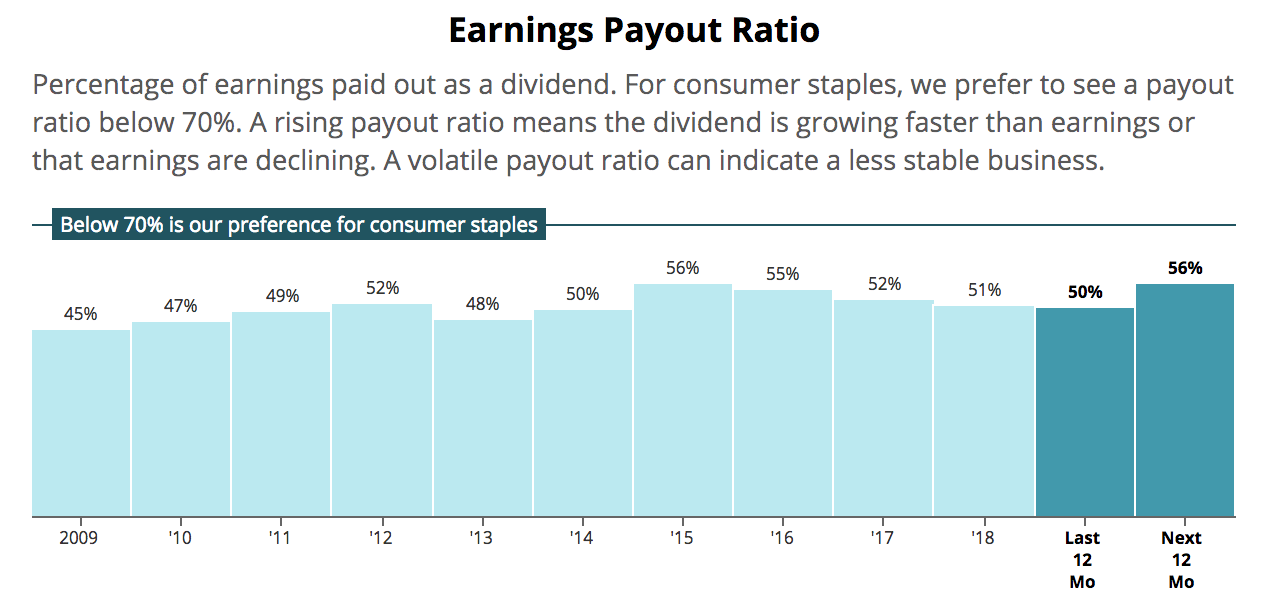

Management targets a long-term payout ratio of 50% of adjusted EPS, which Kellogg achieved in 2018. However, thanks to an expected decline in 2019 earnings and the potential for several divestitures, Kellogg's payout ratio is expected to moderately rise.

Source: Simply Safe Dividends

While the firm's payout ratio seems likely to hover somewhat above management's long-term target for now, Kellogg's dividend continues to look secure. The firm also earns a BBB investment grade credit rating from S&P, providing it with financial flexibility as it continues pursuing acquisitions.

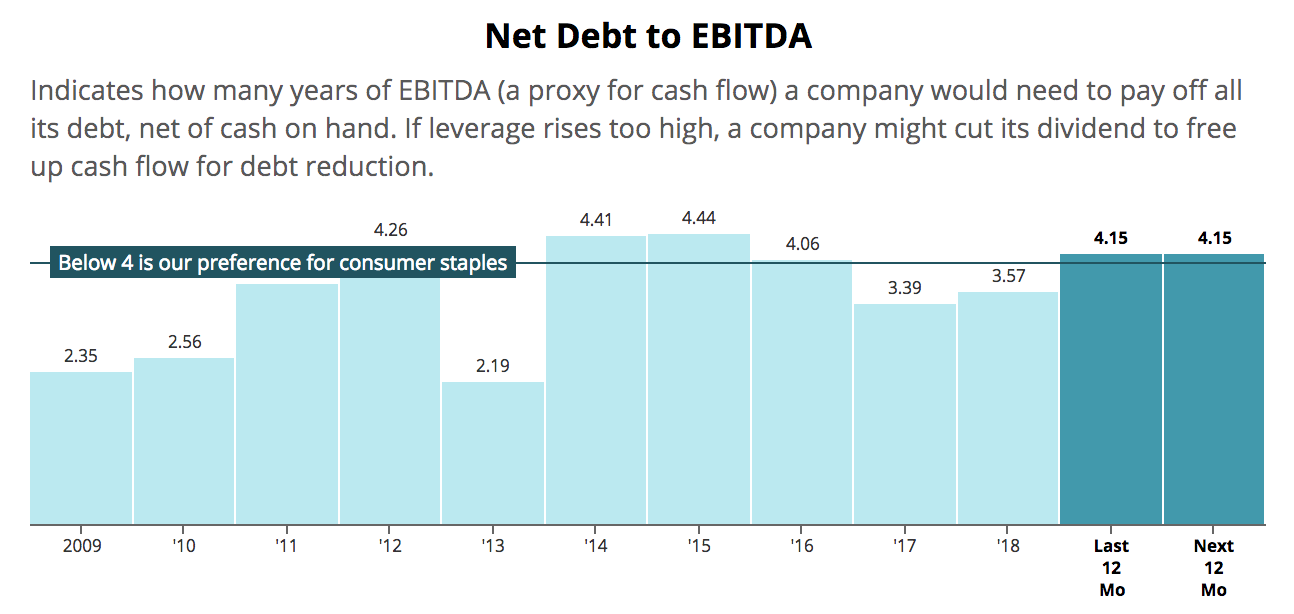

However, those factors don't necessarily mean Kellogg is a solid long-term dividend growth stock. With the payout ratio creeping higher over the last decade and free cash flow remaining suppressed as management increases growth investments, Kellogg could have a harder time maintaining its balance sheet. Management has said that maintaining the firm's investment grade credit rating is a top priority.

Over the past decade, Kellogg has taken on a lot of debt to fund its strategic acquisitions while taking advantage of extremely low interest rates. With most of its free cash flow now going to its safe but slow-growing dividend, profitable growth still a challenge, and acquisitions remaining a key growth strategy, maintaining its current credit rating may be harder in the future.

Source: Simply Safe Dividends

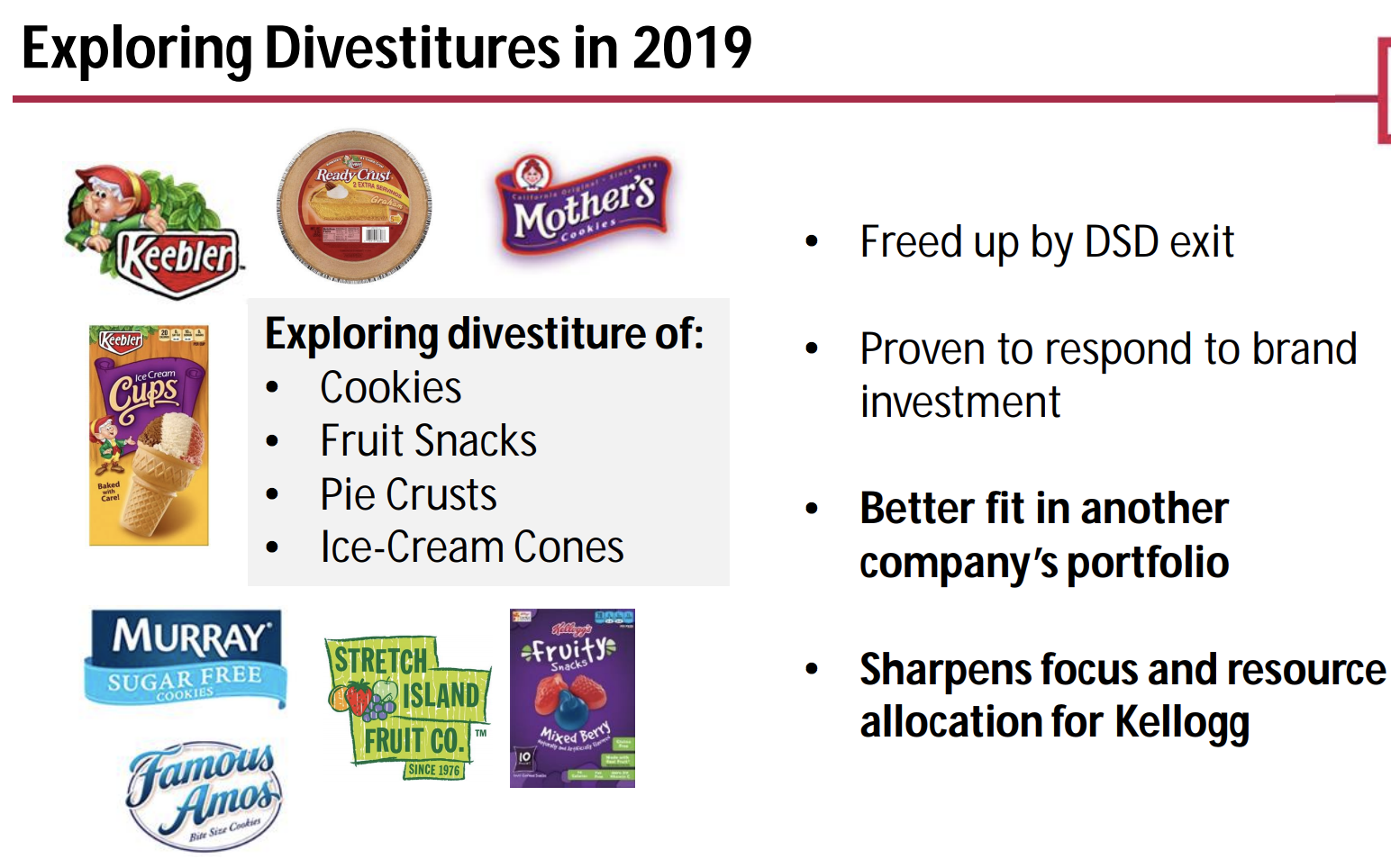

The need to fund its turnaround plans and maintain a healthy balance sheet is a key reason why the company is considering divesting struggling brands that sell slow or negative growth products like cookies and fruit snacks. Management says that those potential divestitures totaled about $900 million in 2018 sales and the proceeds would go to reducing debt ahead of future acquisitions and possibly opportunistic buybacks.

Source: Kellogg Investor Presentation

The good news is that Kellogg's dividend should remain safe despite the firm's divestitures and cost-cutting plans, even if a recession hits and credit markets tighten. Kellogg's business still throws off a lot of cash flow, and most of its products enjoy recession-resistant demand.

However, conservative investors shouldn't expect more than low single-digit annual cash flow and dividend growth for the foreseeable future. Should Kellogg's turnaround continue struggling, perhaps due to prolonged weakness in cereals, a dividend freeze would not be out of the question either, especially if the firm's payout ratio and leverage continue creeping higher.

Basically, while Kellogg's thesis hasn't broken, it has weakened somewhat over the years. Management's long-promised turnaround continues taking more time than most investors expected to return the company to profitable growth.

Combined with signs that Kellogg has mismanaged some of its brands over time and could remain anchored by its large cereal business, potential investors need to ask themselves whether a 4% yield with a very slow payout growth profile and somewhat uncertain long-term outlook is something they want to own in their portfolio.

Concluding Thoughts

Kellogg's wide assortment of large and well-known brands has served investors well for more than a century. However, all companies need to adapt to changing consumer tastes, and Kellogg has really struggled to do that over the past decade.

While management's turnaround plan sounds reasonable, and the firm's long-term growth guidance (about 7% cash flow and dividend growth per year) looks appealing at first glance, investors have reason to be skeptical that it can deliver on that plan.

At the very least, realize that Kellogg, while likely a safe income investment, is probably going to have to grow its dividend slower than in the past, in order to maintain a healthy balance sheet and fund its ongoing turnaround.

As conservative investors, our preference is to invest in companies with stronger long-term outlooks and clearer paths to profitable growth. Many parts of Kellogg's portfolio appear to remain in the crosshairs of changing consumer tastes, and management's long-term track record of adapting the business doesn't inspire much confidence.

.png)