Founded in 1947, Dover (DOV) is an international industrial conglomerate. In 2017, the company decided to spin off its energy division (18% of 2017 revenue) into a seperate company called Apergy (APY). The spin-off became official in May 2018 and left Dover with three less volatile business segments.

Engineered Systems (40% of pro-forma revenue): Dover helps drive efficiencies for customers in printing, identification, vehicle service, and waste-handling equipment. Products in this segment include automation components, printing systems, hydraulic components, electronic components, 3D printing tools, and more.

Fluids (35% of pro-forma revenue): products include strategically engineered specialized pumps, tubing, fueling, vehicle wash, and dispensing systems. Dover’s components and equipment are used for fueling and vehicle wash and for transferring and dispensing critical materials in numerous end markets such as chemicals, food, and pharmaceuticals.

Refrigeration & Food Equipment (25% of pro-forma revenue): Dover’s products reduce customers’ total cost of ownership in refrigeration, electrical, heating and cooling systems, and food and beverage packaging. Products include commercial refrigerator and glass doors, lighting systems, food processing and packaging solutions, cooking preparation equipment, and more.

The company essentially delivers a wide range of equipment and components, specialty systems, and support services that are sold to thousands of customers across numerous end markets including convenience stores, gas stations, grocery stores, and vehicle fleets.

Dover's revenues are mostly from developed markets, but the company also operates in fast-growing emerging economies in Latin America and Asia.

US: 57%

Europe: 19%

Asia: 10%

Latin America: 9%

Rest of World: 5%

With 63 consecutive years of annual dividend growth (tied for the longest in America), Dover is a dividend king.

Business Analysis

In order for a company to generate over six decades of continuous dividend growth, it must have both a stable and growing business, as well as some kind of moat to defend market share and margins over time.

The key to Dover's long-term success is its niche focus on technologically advanced products. The industrial sector is very fragmented with even industry leaders (in their respective niches) only obtaining a small piece of the market. For example, Dover is No. 1 or No. 2 in almost all its niches yet commands roughly 11% market share overall. The company's top brand has 30% market share but most business segments average 20% or less of their markets.

Dover tailors its products to meet the specific needs of its customers, creating deeply integrated systems that result in a "one-stop shop" experience. This allows some of its businesses to also enjoy long-term maintenance contracts which create high margin and recurring revenue streams (60% in its digital printing business).

Due to strict safety and environmental regulations (especially in the food prep and medical industries), most of Dover's components and systems are mission critical in nature. Dover's relationships with its customers sometime stretch back decades, and because reliability and durability are so important, Dover's product quality helps create long-lasting relationships and high switching costs.

And since the cost of the company's products is generally a low percentage of a client's total costs (usually about 5%), Dover is able to maintain strong pricing power without having to worry about losing market share.

The company enjoys a large global distribution chain as well, including in fast-growing markets such as China, Mexico, and Brazil. This distribution network has been built up over 60 years, enables Dover to reliably serve multinational customers, and would be both costly and time-consuming for small upstart rivals to recreate.

To help maximize its profitability, the company has a continuous cost cutting program it calls the Dover Excellence program, which utilizes data-driven business optimization for each autonomously operating business unit. This includes proprietary internal score cards to ensure that the company's numerous small bolt-on acquisitions achieve their synergistic cost savings targets.

Management's dedication to integrating small acquisitions has been one of the biggest drivers of Dover's success over the decades. That's because the specialized and long term, relationship-driven nature of the niche industries in which it operates make it hard to win market share. So Dover essentially buys market share with each acquisition, adding additional patented technology and bringing a loyal base of reliable customers.

Between 2015 and 2017, Dover made 13 bolt on acquisitions totalling $2.2 billion. The company also sold off $1.3 billion in business it deemed slower growing and with less favorable economics (lower margins). That includes the 2017 sales of Performance Motorsports International and the consumer and industrial winch business.

Of course, Dover's business mix is never perfect. The company sometimes incurs large restructuring changes in an effort to stabilize its cash flows and enhance its dividend safety and growth potential. Dover's latest spin-off of Apergy is a good example. Apergy operated in the energy sector, which is prone to boom and bust cycles, including frequent 20% swings in sales depending on the prices of oil and gas. In 2014, management also completed the a spin-off of cyclical electronics components manufacturer Knowles (KN).

Going forward, Dover is focused on increasingly digitizing its products to take advantage of the "internet of things" (IoT). That trend involves placing an increasing number of sensors on industrial components and connecting them to the internet. As a result, customers can monitor their equipment in real time and optimize maintenance and repair schedules, helping each piece of equipment run more efficiently and ultimately be more profitable.

IoT is a key focus for the company's R&D budget which was $125 million in 2017 (1.6% of revenue). In addition, management has said that IoT integration is a major focus of the company's future tuck-in acquisitions.

While Dover's amount of R&D spending is relatively small, management is able to generate excellent returns. For example last year the company managed to generate almost $28 in additional gross profit off each $1 in R&D spent in the prior 12 months. That figure has been rising quickly (up 250% in the past decade according to Morningstar) thanks to the company's increasing focus on IOT integration and customer specific integration.

Overall, Dover's large scale, efficient manufacturing, mission-critical components, and solid pricing power from its long-term customer relationships have helped the firm achieve double-digit operating margins and returns on invested capital. In other words, management has proven to be very disciplined and effective with its use of shareholder capital.

Dover's conservatism and quality are also reflected in the company's balance sheet. In a cyclical and acquisition-heavy industry such as this, a company needs to avoid excessive leverage. That's both to safeguard the dividend but also to retain financial flexibility to make opportunistic bolt-on acquisitions.

Dover's healthy debt ratios earn it an investment grade credit rating of BBB+ from Standard & Poor's. As a result, the company can continue borrowing at low interest rates (an average of 4.1% today) and has flexibility to make small acquisitions going forward.

Over the long term, Dover believes it can achieve 3% to 5% annual organic sales. Thanks to five primary factors, Dover could maintain its current 15% annual EPS growth over the next decade.

Bolt-on acquisition revenue growth of 1% to 2%

A greater focus on higher margin business segments (its energy spin-off earned much lower margins)

Continued cost cutting (margin expansion)

Share buybacks (1% to 2% per year)

Lower tax rate (35% falling to 22%)

If the company is able to hit those forecasts, then it would spell great news for dividend investors who might see dividend growth accelerate from its historical 8% average annual growth rate over last 20 years.

That being said, Dover faces several challenges that might make achieving those growth projections rather difficult.

Key Risks

First, while the spin-off of Apergy will lead to less earnings volatility, Dover's business is not going to be a low volatility one. Just 30% of the company's sales are from recurring sources (quickly consumed products that need constant replacement). That's compared to industrial peers such as 3M (MMM) and Roper Technologies (ROP) who both generate closer to 50% of their sales from recurring sources. In other words, Dover's sales, earnings, and cash flow will still be highly correlated to the health of the US and global economy.

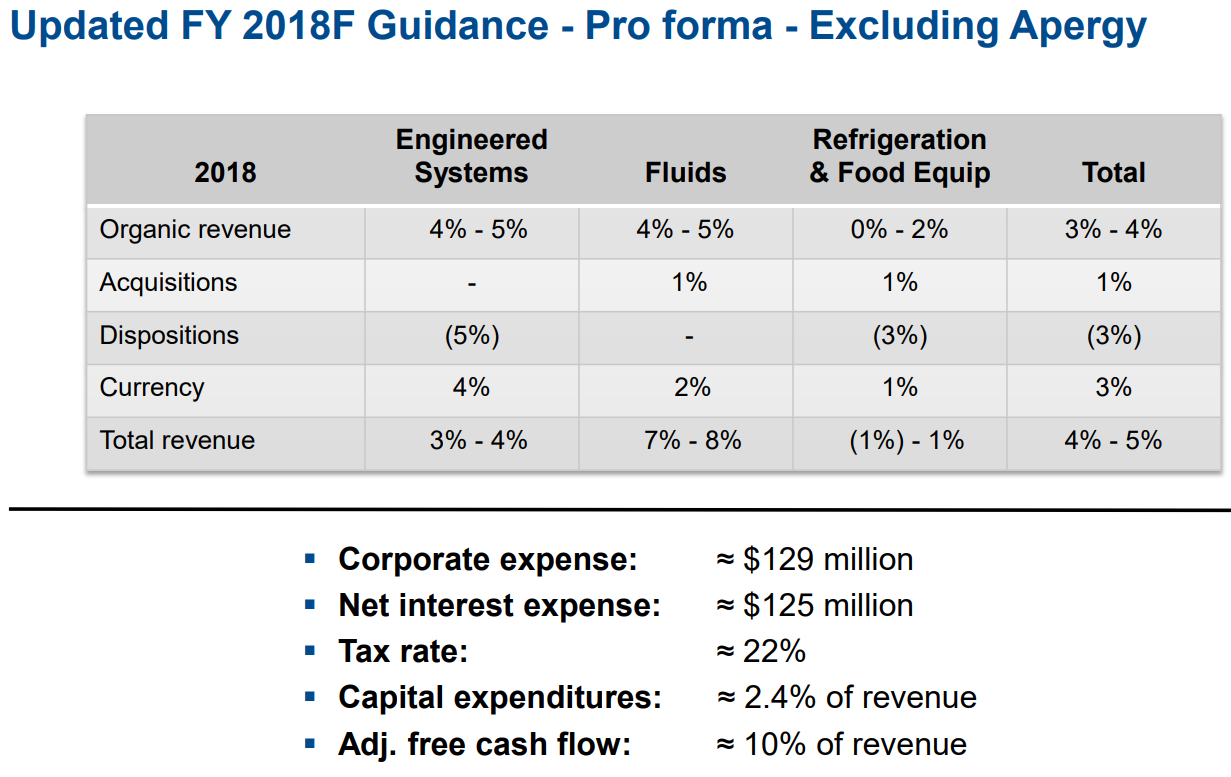

Currency exchange rate fluctuations pose another short-term risk to the business. Over 40% of Dover's are from overseas markets, which can affect the company's reported rates of sales and earnings growth any given year. For example, management's 2018 guidance assumes that currency fluctuations will boost its revenue growth by 300 basis points.

Source: Dover Earnings Presentation

Besides the health of the economy and currency exchange rates, rising raw material input prices can also crimp Dover's performance over the short term. However, none of these factors should impact the company's long-term earnings power.

Finally, it's worth mentioning again that the highly fragmented nature of this industry results in a lot of acquisitions. While Dover has done a good job avoiding large, complex, and complicated purchases, the company still spends roughly $700 million per year acquiring smaller bolt-on companies. Each acquisition comes with execution risk, including the chance of overpaying and missing on synergy targets.

Other than unpredictable macro trends, there doesn’t seem to be much that threatens Dover’s long-term prospects. The company is well diversified by product, end market, and customer. Most of its markets evolve at a very slow pace, and it’s hard to imagine many of the company’s products becoming obsolete.

If anything, Dover’s biggest risk is probably itself. The company likes to acquire other businesses, which adds some risk to its strategy. Furthermore, although Dover has become less decentralized over the years, additional acquisitions could cause the company to reach a point where it needs to reorganize its segments or risk them becoming inefficient.

Overall, Dover has proven to be an extremely well-managed company.

Closing Thoughts on Dover

For more than 60 years, Dover has managed to prove that a little-known company in a boring industry can be a great dividend growth investment. Management's disciplined focus on building an empire of niche market leaders in specialized sub-industries has proven to be a winning strategy.

Combined with a strong balance sheet, good record of increasing profitability over time, and long-term growth catalysts (the internet of things and digital industrial systems), Dover is likely to continue delivering safe and consistent dividend growth for years, if not decades, to come.